Answered step by step

Verified Expert Solution

Question

1 Approved Answer

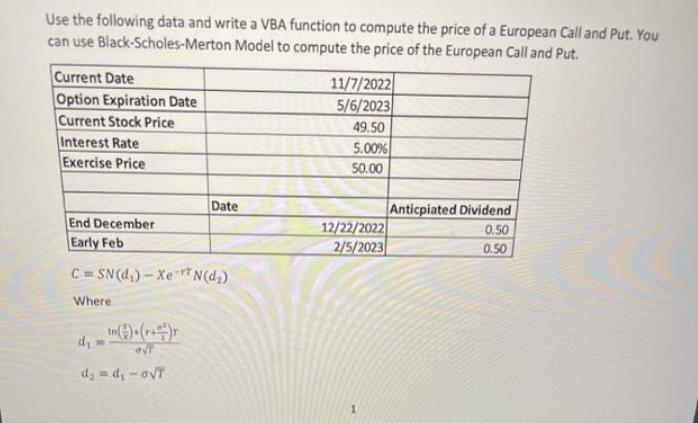

Use the following data and write a VBA function to compute the price of a European Call and Put. You can use Black-Scholes-Merton Model

Use the following data and write a VBA function to compute the price of a European Call and Put. You can use Black-Scholes-Merton Model to compute the price of the European Call and Put. Current Date Option Expiration Date Current Stock Price Interest Rate Exercise Price End December Early Feb C=SN(d,)- Xe N(d) Where Date d d=d - oT 11/7/2022 5/6/2023 49.50 5.00% 50.00 12/22/2022 2/5/2023 Anticpiated Dividend 0.50 0,50

Step by Step Solution

★★★★★

3.43 Rating (162 Votes )

There are 3 Steps involved in it

Step: 1

Certainly Heres an example of a VBA function that uses the BlackScholesMerton model to compute the price of a European Call and Put option vba Functio...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Concepts In Federal Taxation

Authors: Kevin E. Murphy, Mark Higgins, Tonya K. Flesher

19th Edition

978-0324379556, 324379552, 978-1111579876