Answered step by step

Verified Expert Solution

Question

1 Approved Answer

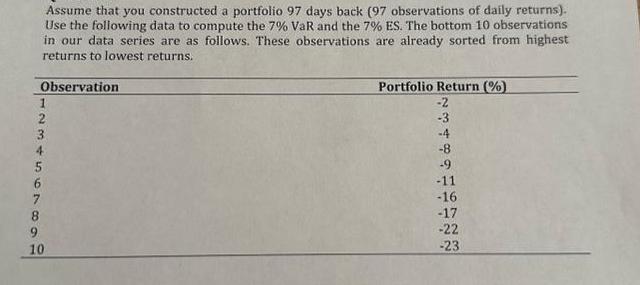

Assume that you constructed a portfolio 97 days back (97 observations of daily returns). Use the following data to compute the 7% VaR and

Assume that you constructed a portfolio 97 days back (97 observations of daily returns). Use the following data to compute the 7% VaR and the 7% ES. The bottom 10 observations in our data series are as follows. These observations are already sorted from highest returns to lowest returns. Observation 123456TBOR 7 9 10 Portfolio Return (%) -2 -3 -4 -8 -9 -11 -16 -17 -22 -23

Step by Step Solution

★★★★★

3.33 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

7 VaR The 7 VaR is the 7th percentil...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Macroeconomics Principles And Policy

Authors: William J. Baumol, Alan S. Blinder

11th Edition

0324586213, 978-0324586213