Answered step by step

Verified Expert Solution

Question

1 Approved Answer

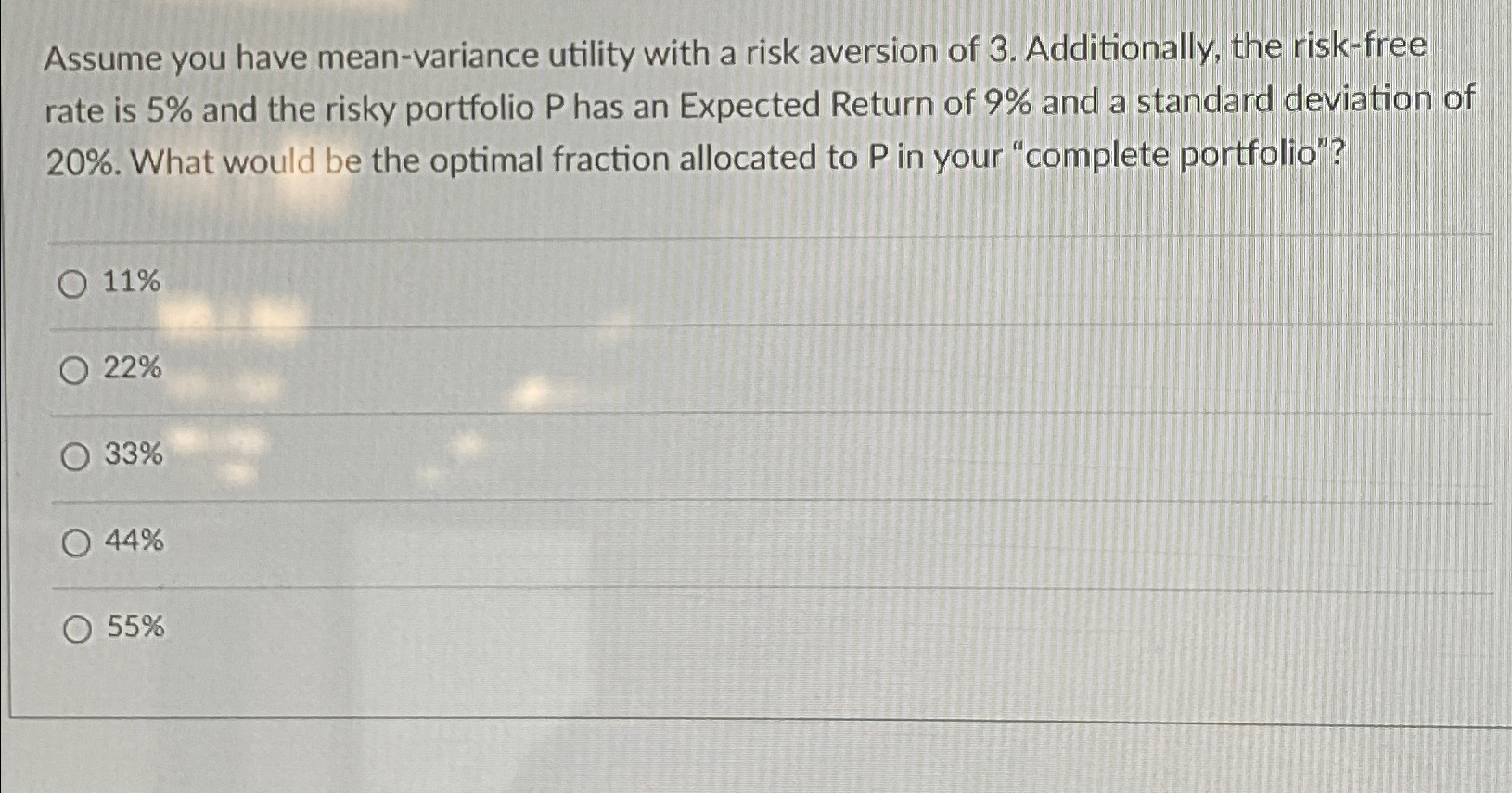

Assume you have mean - variance utility with a risk aversion of 3 . Additionally, the risk - free rate is 5 % and the

Assume you have meanvariance utility with a risk aversion of Additionally, the riskfree rate is and the risky portfolio has an Expected Return of and a standard deviation of What would be the optimal fraction allocated to in your "complete portfolio"?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of Alternative Assets

Authors: Peter Temple

1st Edition

161477076X, 978-1906659219