Answered step by step

Verified Expert Solution

Question

1 Approved Answer

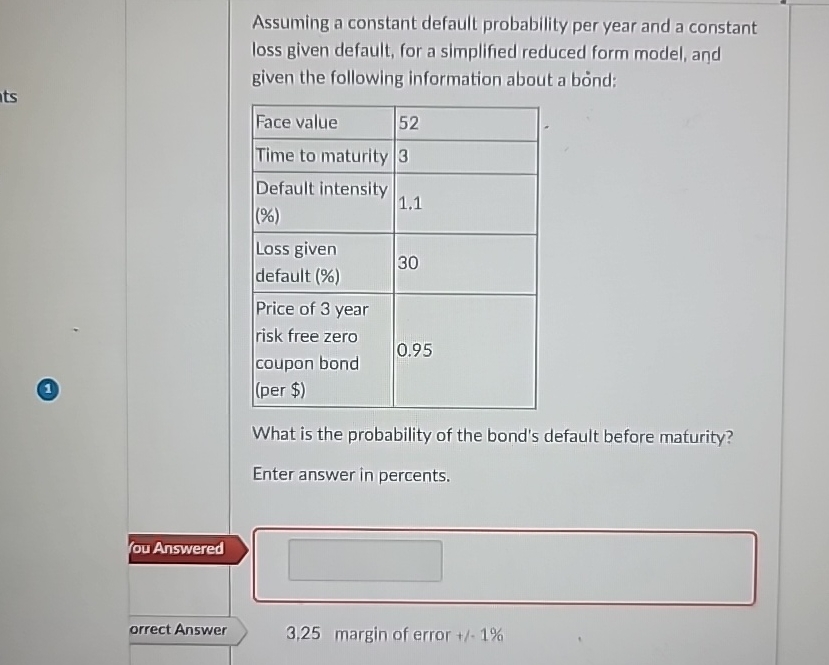

Assuming a constant default probability per year and a constant loss given default, for a simplified reduced form model, and given the following information about

Assuming a constant default probability per year and a constant loss given default, for a simplified reduced form model, and given the following information about a bond:

tableFace value,Time to maturity,tableDefault intensitytableLoss givendefault tablePrice of yearrisk free zerocoupon bondper $

What is the probability of the bond's default before maturity?

Enter answer in percents.

ou Answered

orrect Answer

margin of error

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Course In Derivative Securities

Authors: Kerry Back

2005th Edition

3540253734, 978-3540253730