Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Assuming the risk-free rate is 7 percent, calculate Sharpe ratios for ABC, XYZ and KLCI. Compare the performance of ABC and XYZ relative to the

Assuming the risk-free rate is 7 percent, calculate Sharpe ratios for ABC, XYZ and KLCI.

Compare the performance of ABC and XYZ relative to the market index based on the answer in (a).

Assuming the risk-free rate is 7 percent, calculate Treynor's ratio for ABC, XYZ, and KLCI.

State the differences between the two measurements.

If the actual returns realized from ABC and XYZ funds are 12 and 19 percent respectively, given that the market return is 15 percent and beta is 0.7 and 1.3, calculate the expected return for both funds.

Calculate the differential return or alpha value for ABC and XYZ funds.

Compare the performance of ABC and XYZ relative to the market index based on the answer in (a).

Assuming the risk-free rate is 7 percent, calculate Treynor's ratio for ABC, XYZ, and KLCI.

State the differences between the two measurements.

If the actual returns realized from ABC and XYZ funds are 12 and 19 percent respectively, given that the market return is 15 percent and beta is 0.7 and 1.3, calculate the expected return for both funds.

Calculate the differential return or alpha value for ABC and XYZ funds.

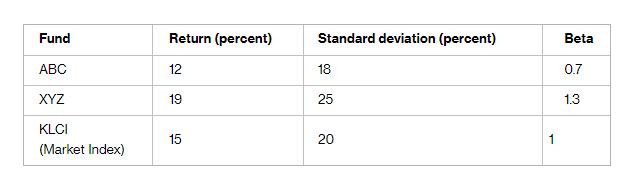

Fund ABC XYZ KLCI (Market Index) Return (percent) 12 19 15 Standard deviation (percent) 18 25 20 1 Beta 0.7 1.3

Step by Step Solution

★★★★★

3.49 Rating (172 Votes )

There are 3 Steps involved in it

Step: 1

Sharpe Ratio Return of the fund Riskfree rate Standard deviation of the fund Calculation of the Shar...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Financial Management

Authors: Eugene F. Brigham, Joel F. Houston

15th edition

1337671002, 978-1337395250