Answered step by step

Verified Expert Solution

Question

1 Approved Answer

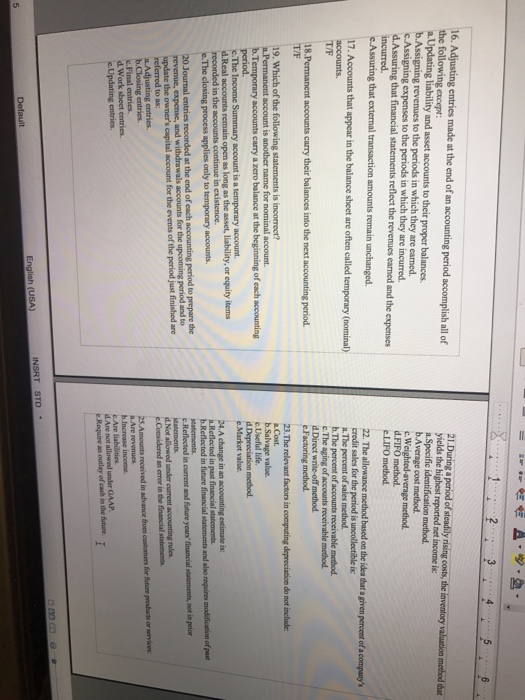

Assuring that external transaction amounts remain unchanged False True Real accounts remain open as long as the asset, liability or equity items recorded in the

- Assuring that external transaction amounts remain unchanged

- False

- True

- Real accounts remain open as long as the asset, liability or equity items recorded in the accounts continue in existence

- Closing entries

- FIFO

- The percent of sales method

- Market Value

- Reflected in current and future years financial statement, not in prior statements

- Are revenues

These are the answers I got on my accounting homework, but when I received the score it said I got some wrong (but I cannot see what I did) can you tell me what I missed ?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Mastering SAP FICO A Comprehensive Guide To Financial Accounting And Controlling

Authors: Daniel Moussima

1st Edition

979-8859658541