Answered step by step

Verified Expert Solution

Question

1 Approved Answer

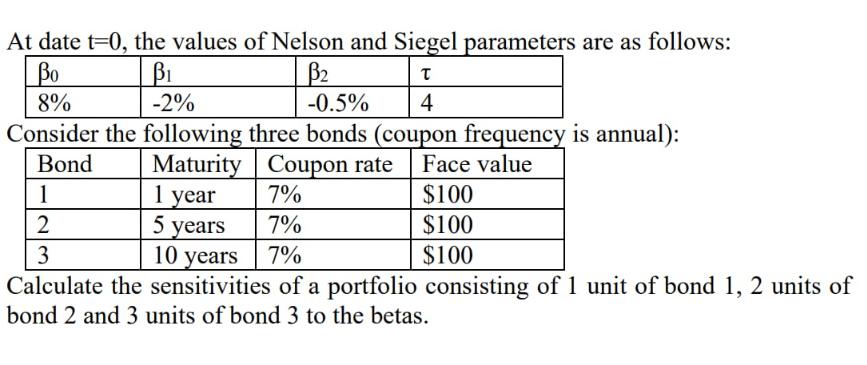

At date t=0, the values of Nelson and Siegel parameters are as follows: Bo B B T 8% -2% -0.5% 4 Consider the following

At date t=0, the values of Nelson and Siegel parameters are as follows: Bo B B T 8% -2% -0.5% 4 Consider the following three bonds (coupon frequency is annual): Bond Maturity Coupon rate Face value $100 1 1 year 7% 2 5 years 7% 3 10 years 7% Calculate the sensitivities of a portfolio consisting of 1 unit of bond 1, 2 units of bond 2 and 3 units of bond 3 to the betas. $100 $100

Step by Step Solution

★★★★★

3.51 Rating (161 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the sensitivities of the portfolio to the NelsonSiegel parameters we need to first calc...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance for Executives Managing for Value Creation

Authors: Gabriel Hawawini, Claude Viallet

4th edition

9781133169949, 538751347, 978-0538751346