Answered step by step

Verified Expert Solution

Question

1 Approved Answer

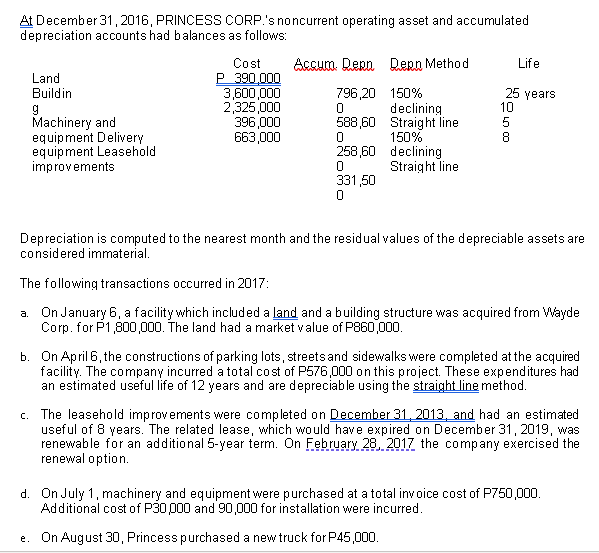

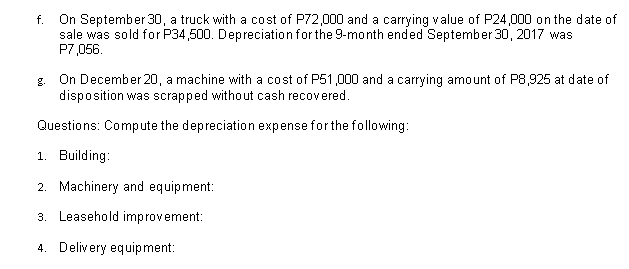

At December 31, 2016, PRINCESS CORP.'s noncurrent operating asset and accumulated depreciation accounts had balances as follows: Cost Accum. Depn Depn Method Life Land P

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Integrated Accounting For Windows

Authors: Dale A. Klooster, Warren Allen

5th Edition

0324312490, 9780324312492