Question

At the most basic level, you could just add up each account for all the companies and call that Consolidated. That's the starting point. But

At the most basic level, you could just add up each account for all the companies and call that "Consolidated." That's the starting point. But we've gone through all of the changes that must be made to reflect the combination of the four companies as if they were a single economic entity. Moving a chair from one office to another doesn't affect the value of a business, does it? Moving a machine (or other asset) from one company in a consolidated group to another company in the same consolidated group doesn't affect the value of the consolidated group. Go through those items and start making adjustments to the sum of the four companies. Cash is easy, the total of the four companies is the same as if it were a single entity, right? But then it gets more complex:

- Eliminate the investment account

- Eliminate equity income

- Eliminate intercompany sales

- Eliminate the effects of intercompany transactions (like asset sales)

- etc.

Just think through all of the topics we've covered and how they affect consolidated financial statements, then figure out what sort of adjustment is necessary to make the statements meet the "single economic entity" objective. On an asset sale, for example, you might compare what the statements currently reflect and what they would reflect if the transaction had been within a single company. Asset transfers within a single economic entity can't affect financial statements.

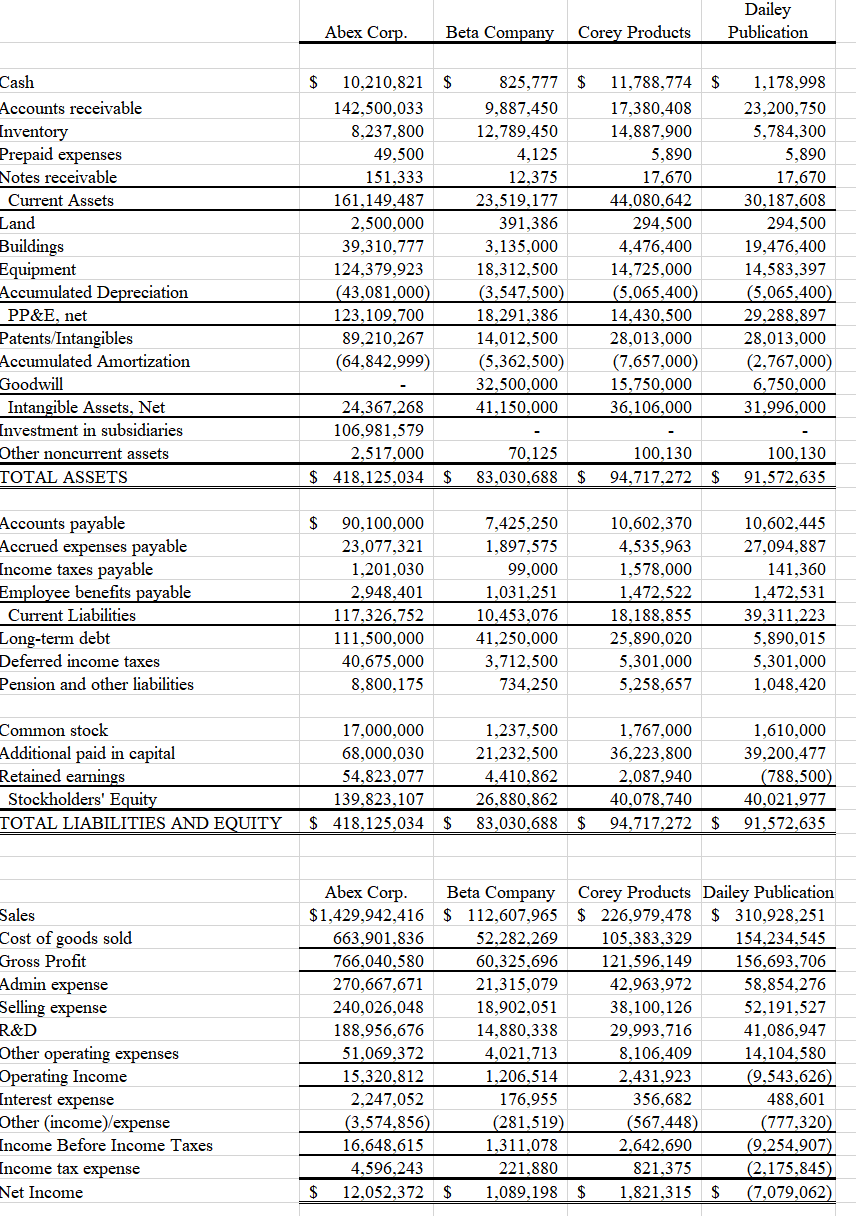

You are the Consolidation Accountant for Abex Corporation. Assume that 2021 is the first year that Abex is preparing consolidated financial statements with its three subsidiaries. (That's a very silly assumption, don't think about it too deeply. It allows us to not be concerned with prior consolidation adjustments.) Do read the instructions completely and carefully before starting. This must be your own work product. You may refer to notes, the textbook, etc. But you may not consult with anyone else. The spreadsheet you submit must be your own work. Critical assumptions about the financial statements:

presented with a statement of financial position and a statement of income for each company, separately. These are not trial balances, though you could prepare one if you wish (I don't recommend that).

Recall that consolidating financial statements means that you will be recording adjustments to the statements, not offsetting journal entries. If you wish to reformat the statements to consolidate, you may. But the end result must be a consolidated statement of financial position and a consolidated statement of income, presented as they would be shown in a company's annual report.

Related to the item above, I likely mislead you (I should probably just say "I did mislead you") on the adjustments comment in consolidating financial statements. Make sure you understand this. Any "adjustments" made to the statement of financial position necessarily are in the form of offsetting debits and credits. Otherwise, the statement of financial position wouldn't balance, right? However, adjustments to the statement of income may be different. There may be some that affect only one account in the statement of income. Profit in inventory is an example of this. You'll debit or credit one account in the statement of income, but there won't be an offsetting entry to another account. When recording profit in inventory in the statement of financial position, however, there will be a debit and credit that offset. The offsetting debit or credit is in retained earnings.

Each company has completed the closing process and is presenting financial statements in accordance with GAAP.

Abex uses the equity method of accounting. Abex owns 100% of the three subsidiaries and has recorded the income of the subsidiaries in its equity accounts. Abex's statement of income includes equity income in the caption "Other (income) expense." The other item in the caption for Abex is Royalty Income on a patent it developed and licensed to an unrelated company.

o You must use formulas wherever possible (subtotals, for example).

o Your adjustments must be supported and explained, either on the consolidation spreadsheet or on a separate worksheet (in the same Excel workbook).

o The end result must be a consolidated (not consolidating) statement of financial condition and a consolidated statement of income. (Consolidated statements show only the consolidated amounts and do not show the individual companies in the consolidation.) The statements must be in a format that could be printed and given to senior executives, a bank, investors, etc.

Intercompany Sales: The four companies have intercompany transactions involving inventory. During the year, the following intercompany sales were made:

1. Abex sold to Corey: $252,500.

2. Dailey sold to Corey: $23,400.

3. Corey sold to Beta: $89,554.

4. Corey sold to Dailey: $121,000.

By company policy, all intercompany sales are priced so that the selling company has a gross profit of 30%. (For example, Abex will have a gross profit of 30% on its sales to Corey.)

Unsold Inventory: At the end of the year, only 25% of the inventory sold by Corey to Dailey has been sold to outside parties. At the end of the year, $25,000 of the inventory sold by Corey to Beta remained in inventory. Other than that, all intercompany inventory was sold to outside parties.

Intercompany Accounts: The following intercompany balances remain at year-end. Intercompany receivables are included in "Accounts receivable" and the related payable is included in "Accounts payable."

1. Corey receivable from Dailey: $112,500.

2. Abex receivable from Corey: $51,750

Intercompany Asset Transfer: During the year, 5 acres of undeveloped land was sold by Corey to Abex. Corey's book value of the land at the time of the transfer was $75,000. The land was sold to Abex for $500,000, with the gain on the sale recorded in "Other (income)/expense." The payment of $500,000 from Abex to Corey was settled before the end of the year.

In addition, Dailey sold a machine (at time of sale, cost = $85,000; accumulated depreciation = $65,000) to Abex for $105,000. The sale took place at the end of the year, so Abex has not recorded any depreciation expense (and won't until January). Dailey depreciated the machine through the end of the year.

Management Fee: Abex charges its subsidiaries a fee equal to 1% of sales (to pay for services provided by the parent company, Abex). The fee revenue has been recorded by all companies and paid (there is no receivable or payable related to this) Abex records the fee as a reduction of Administrative Expense. The subsidiaries include the expense in "Other (income)/expense."

By practice, the fee is calculated and paid at the end of the year and is rounded down to the nearest even thousand dollar amount. (So, if the fee calculated to $5,349, the fee would be rounded to $5,000.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Government and Not-for-Profit Accounting Concepts and Practices

Authors: Michael H. Granof, Saleha B. Khumawala, Thad D. Calabrese, Daniel L. Smith

8th edition

1119495814, 1119495857, 1119495819, 9781119495819 , 978-1119495857