Answered step by step

Verified Expert Solution

Question

1 Approved Answer

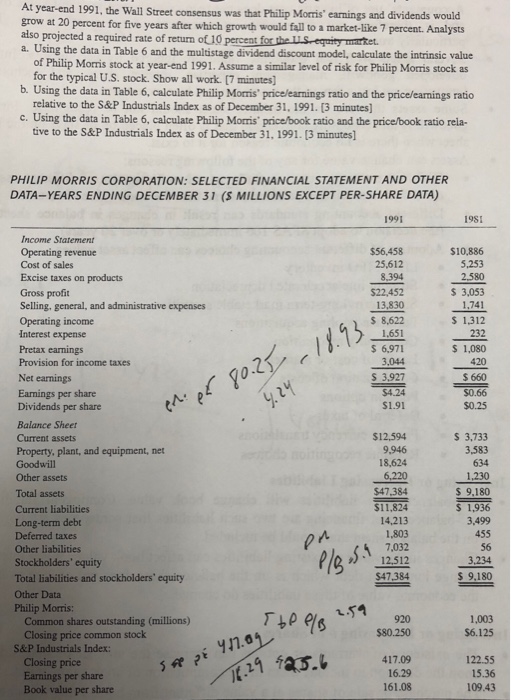

At year-end 1991, the Wall Street consensus was that Philip Morris' earnings and dividends would grow at 20 percent for five years after which growth

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Full IFRS And IFRS For SMEs Adoption By Private Firms Empirical Evidence On Country Level

Authors: Maximilian Saucke

1st Edition

363166298X,3653055318