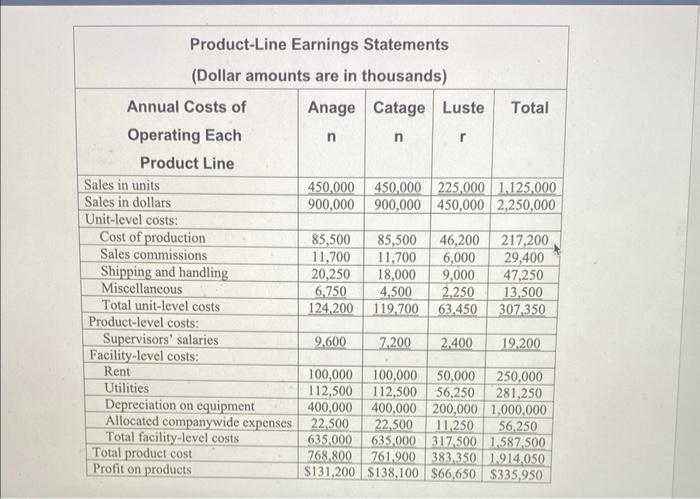

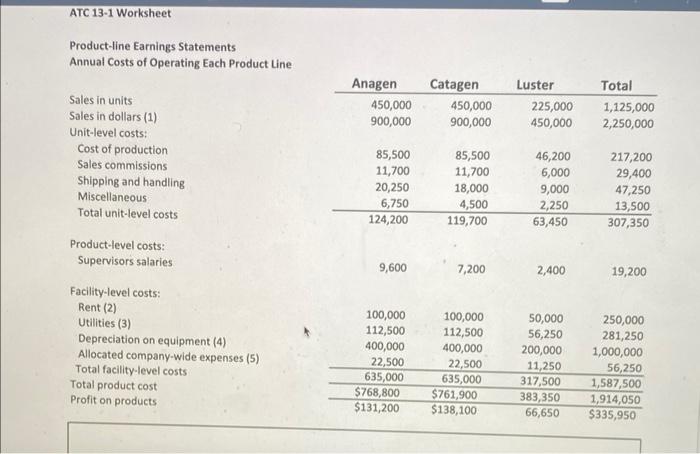

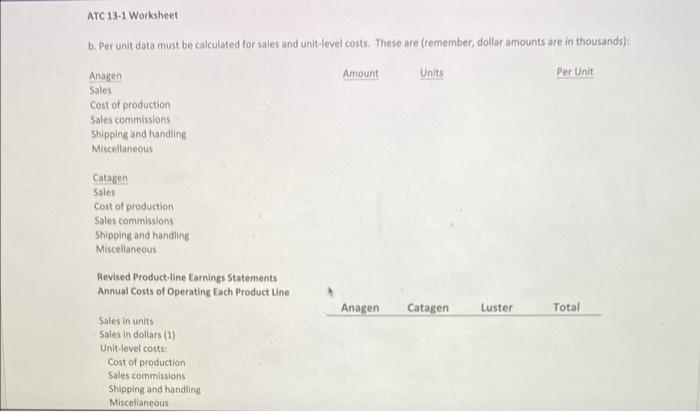

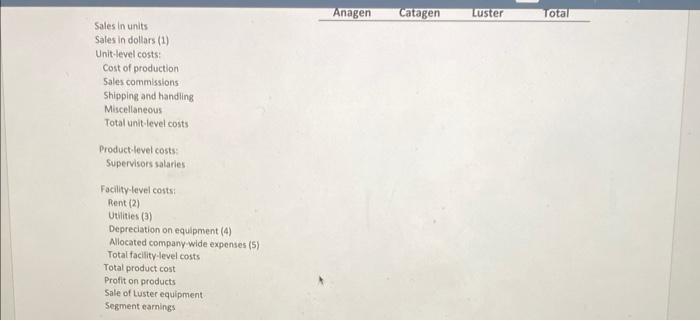

ATC 13-1 Business Application Case Analyzing inventory reductions at Proctor & Gamble Real-wordd companies offen seek to reduce the complexity of their operations in an attempt to increase profits. In 2012, Procter \& Gamble (PAG) telient it could increase the company's profits by eliminating some product-tines. In 2017, PEG announced that it had "divessed, discontinued, or consolidateded 105 brands". As a result, eeten thougel its sales had decresed by 22 percent from 2012102017 , its proff as a percentage of soles had luceresed by 55 percent, Other companies have also tried to improve their financial performance by downsizige. In Norember 2017, Geteral Electric announced it nould beginin a downsizing operation that would result in their exiting businesses using over \$20 billion in assets in the next one to two jears. In January 2018, Newell Bradds, the company whose products include Tupperware, Sharpie pens, Elmer's Glue, and Remtings spoots products, announced it would be reducing its product offerings to the extent that it would close half of its facilities and reduce it rereatus by 20 percent. Required a. Identify some cost savings these companies might realize by reducing the number of items they sell or use in production. Be as specific as possible, and use your imagination. b. Consider the additional information presented as follows, which is hypothetical. All dollar amounts are in thousands; unit amounts are not. Assume that P\&G decides to eliminate one the following are expected to occur. (1) The number of units sold for the segment is expected to drop by only 125.000 becanse of (1) The number of units sold for the segment is expected to drop by only 125,000 because of the elimination of Luster, since most customers are expected to purchase an Anagen or Catagen product instead. The shift of sales from Luster to Anagen and Catagen is expected to be evenly split. In other words, the sales of Anagen and Catagen will each increase by 50,000 units. (2) Rent is paid for the entire production facility, and the space used by Luster cannot be sublet. (3) Utilities costs are expected to be reduced by $40,000. (4) All of the supervisors for Luster were terminated. No new supervisors will be hired for Anagen or Catagen. (5) Half of the equipment being used to produce Luster is also used to produce the other two products and its depreciation cost must be absorbed by them. The remaining equipment has a book-value of $340,000 and can be sold for only $60,000. (6) Facility-level costs will continue to be allocated between the product lines based on the number of units produced. pare revised product-line earnings statements based on the elimination of Luster. (Hint: It will be essary to calculate some per-unit data to accomplish this). Product-Line Earnings Statements (Dollar amounts are in thousands) \begin{tabular}{|l|c|c|c|c|} \hline \multicolumn{1}{|c|}{\begin{tabular}{|c|c|c|} \hline Annual Costs of \\ Operating Each \\ Product Line \end{tabular}} & Anage & Catage & Luste & Total \\ \multicolumn{1}{|c|}{n} & r & \\ \hline Sales in units & 450,000 & 450,000 & 225,000 & 1,125,000 \\ \hline Sales in dollars & 900,000 & 900,000 & 450,000 & 2,250,000 \\ \hline Unit-level costs: & & & & \\ \hline Cost of production & 85,500 & 85,500 & 46,200 & 217,200 \\ \hline Sales commissions & 11,700 & 11,700 & 6,000 & 29,400 \\ \hline Shipping and handling & 20,250 & 18,000 & 9,000 & 47,250 \\ \hline Miscellaneous & 6,750 & 4,500 & 2,250 & 13,500 \\ \hline Total unit-level costs & 124,200 & 119,700 & 63,450 & 307,350 \\ \hline Product-level costs: & & & & \\ \hline Supervisors' salaries & 9,600 & 7,200 & 2,400 & 19,200 \\ \hline Facility-level costs: & & & & \\ \hline Rent & 100,000 & 100,000 & 50,000 & 250,000 \\ \hline Utilities & 112,500 & 112,500 & 56,250 & 281,250 \\ \hline Depreciation on equipment & 400,000 & 400,000 & 200,000 & 1,000,000 \\ \hline Allocated companywide expenses & 22,500 & 22,500 & 11,250 & 56,250 \\ \hline Total facility-level costs & 635,000 & 635,000 & 317,500 & 1,587,500 \\ \hline Total product cost & 768,800 & 761,900 & 383,350 & 1,914,050 \\ \hline Profit on products & $131,200 & $138,100 & $66,650 & $335,950 \\ \hline \end{tabular} Product-line Earnings Statements A b. Per unit data must be calculated for sales and unit-level costs. These are (remember, dollar amounts are in thousands): Sales in units Sales in dollars (1) Unit-level costs: Cost of production Sales commissions Shipping and handling Miscellaneous Total unit-level costs Product-level costs: Supervisors salaries Facility-level costs: Rent (2) Utilities (3) Depreciation on equipment (4) Allocated company wide expenses (5) Total facility level costs Total product cost Profit on products Sale of Luster equipment Segment earnings Calculation Detasis: (1) (2) (3) (4) (5) ATC 13-1 Business Application Case Analyzing inventory reductions at Proctor & Gamble Real-wordd companies offen seek to reduce the complexity of their operations in an attempt to increase profits. In 2012, Procter \& Gamble (PAG) telient it could increase the company's profits by eliminating some product-tines. In 2017, PEG announced that it had "divessed, discontinued, or consolidateded 105 brands". As a result, eeten thougel its sales had decresed by 22 percent from 2012102017 , its proff as a percentage of soles had luceresed by 55 percent, Other companies have also tried to improve their financial performance by downsizige. In Norember 2017, Geteral Electric announced it nould beginin a downsizing operation that would result in their exiting businesses using over \$20 billion in assets in the next one to two jears. In January 2018, Newell Bradds, the company whose products include Tupperware, Sharpie pens, Elmer's Glue, and Remtings spoots products, announced it would be reducing its product offerings to the extent that it would close half of its facilities and reduce it rereatus by 20 percent. Required a. Identify some cost savings these companies might realize by reducing the number of items they sell or use in production. Be as specific as possible, and use your imagination. b. Consider the additional information presented as follows, which is hypothetical. All dollar amounts are in thousands; unit amounts are not. Assume that P\&G decides to eliminate one the following are expected to occur. (1) The number of units sold for the segment is expected to drop by only 125.000 becanse of (1) The number of units sold for the segment is expected to drop by only 125,000 because of the elimination of Luster, since most customers are expected to purchase an Anagen or Catagen product instead. The shift of sales from Luster to Anagen and Catagen is expected to be evenly split. In other words, the sales of Anagen and Catagen will each increase by 50,000 units. (2) Rent is paid for the entire production facility, and the space used by Luster cannot be sublet. (3) Utilities costs are expected to be reduced by $40,000. (4) All of the supervisors for Luster were terminated. No new supervisors will be hired for Anagen or Catagen. (5) Half of the equipment being used to produce Luster is also used to produce the other two products and its depreciation cost must be absorbed by them. The remaining equipment has a book-value of $340,000 and can be sold for only $60,000. (6) Facility-level costs will continue to be allocated between the product lines based on the number of units produced. pare revised product-line earnings statements based on the elimination of Luster. (Hint: It will be essary to calculate some per-unit data to accomplish this). Product-Line Earnings Statements (Dollar amounts are in thousands) \begin{tabular}{|l|c|c|c|c|} \hline \multicolumn{1}{|c|}{\begin{tabular}{|c|c|c|} \hline Annual Costs of \\ Operating Each \\ Product Line \end{tabular}} & Anage & Catage & Luste & Total \\ \multicolumn{1}{|c|}{n} & r & \\ \hline Sales in units & 450,000 & 450,000 & 225,000 & 1,125,000 \\ \hline Sales in dollars & 900,000 & 900,000 & 450,000 & 2,250,000 \\ \hline Unit-level costs: & & & & \\ \hline Cost of production & 85,500 & 85,500 & 46,200 & 217,200 \\ \hline Sales commissions & 11,700 & 11,700 & 6,000 & 29,400 \\ \hline Shipping and handling & 20,250 & 18,000 & 9,000 & 47,250 \\ \hline Miscellaneous & 6,750 & 4,500 & 2,250 & 13,500 \\ \hline Total unit-level costs & 124,200 & 119,700 & 63,450 & 307,350 \\ \hline Product-level costs: & & & & \\ \hline Supervisors' salaries & 9,600 & 7,200 & 2,400 & 19,200 \\ \hline Facility-level costs: & & & & \\ \hline Rent & 100,000 & 100,000 & 50,000 & 250,000 \\ \hline Utilities & 112,500 & 112,500 & 56,250 & 281,250 \\ \hline Depreciation on equipment & 400,000 & 400,000 & 200,000 & 1,000,000 \\ \hline Allocated companywide expenses & 22,500 & 22,500 & 11,250 & 56,250 \\ \hline Total facility-level costs & 635,000 & 635,000 & 317,500 & 1,587,500 \\ \hline Total product cost & 768,800 & 761,900 & 383,350 & 1,914,050 \\ \hline Profit on products & $131,200 & $138,100 & $66,650 & $335,950 \\ \hline \end{tabular} Product-line Earnings Statements A b. Per unit data must be calculated for sales and unit-level costs. These are (remember, dollar amounts are in thousands): Sales in units Sales in dollars (1) Unit-level costs: Cost of production Sales commissions Shipping and handling Miscellaneous Total unit-level costs Product-level costs: Supervisors salaries Facility-level costs: Rent (2) Utilities (3) Depreciation on equipment (4) Allocated company wide expenses (5) Total facility level costs Total product cost Profit on products Sale of Luster equipment Segment earnings Calculation Detasis: (1) (2) (3) (4)