Answered step by step

Verified Expert Solution

Question

1 Approved Answer

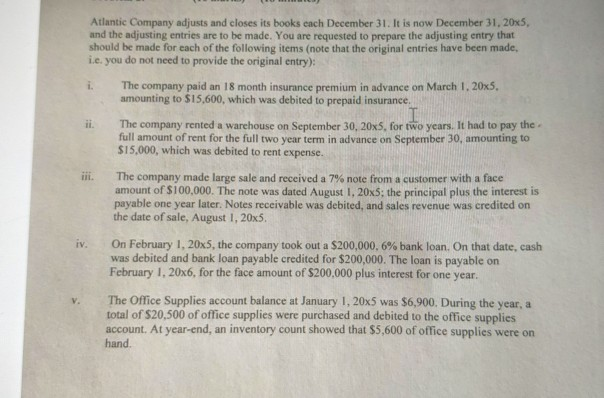

Atlantic Company adjusts and closes its books each December 31. It is now December 31, 20x3 and the adjusting entries are to be made. You

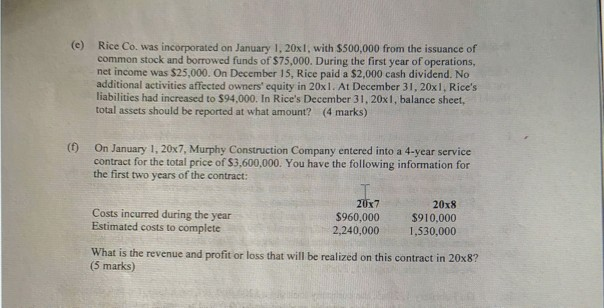

Atlantic Company adjusts and closes its books each December 31. It is now December 31, 20x3 and the adjusting entries are to be made. You are requested to prepare the adjusting entry that should be made for each of the following items (note that the original entries have been made ie, you do not need to provide the original entry): The company paid an 18 month insurance premium in advance on March 1, 20x5. amounting to $15,600, which was debited to prepaid insurance The company rented a warehouse on September 30, 20x5, for two years. It had to pay the full amount of rent for the full two year term in advance on September 30, amounting to $15.000, which was debited to rent expense. TIL The company made large sale and received a 7% note from a customer with a face amount of $100,000. The note was dated August 1, 20x5: the principal plus the interest is payable one year later. Notes receivable was debited, and sales revenue was credited on the date of sale, August 1, 20x5. On February 1, 20x5, the company took out a $200,000.6% bank loan. On that date, cash was debited and bank loan payable credited for $200,000. The loan is payable on February 1, 20x6, for the face amount of $200,000 plus interest for one year. The Office Supplies account balance at January 1, 20x5 was $6,900. During the year, a total of $20,500 of office supplies were purchased and debited to the office supplies account. At year-end, an inventory count showed that $5,600 of office supplies were on hand (c) Rice Co. was incorporated on January 1, 20x1, with $500.000 from the issuance of common stock and borrowed funds of $75,000. During the first year of operations, net income was $25,000. On December 15. Rice paid a $2,000 cash dividend. No additional activities affected owners' equity in 20x1. At December 31, 20x1. Rice's liabilities had increased to $94.000. In Rice's December 31, 20x1, balance sheet, total assets should be reported at what amount? (4 marks) (t) On January 1, 20x 7, Murphy Construction Company entered into a 4-year service contract for the total price of 53,600,000. You have the following information for the first two years of the contract: Costs incurred during the year Estimated costs to complete 2017 $960,000 2.240,000 20x8 $910,000 1,530,000 What is the revenue and profit or loss that will be realized on this contract in 20x8

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Business And Finance An Active Learning Approach Promoting Act

Authors: Jill Hussey

1st Edition

9781858050799