Question: Attached are the excel sheets for the case! could you please with using a DCF approach, sign a new striker! with details please. the questionn

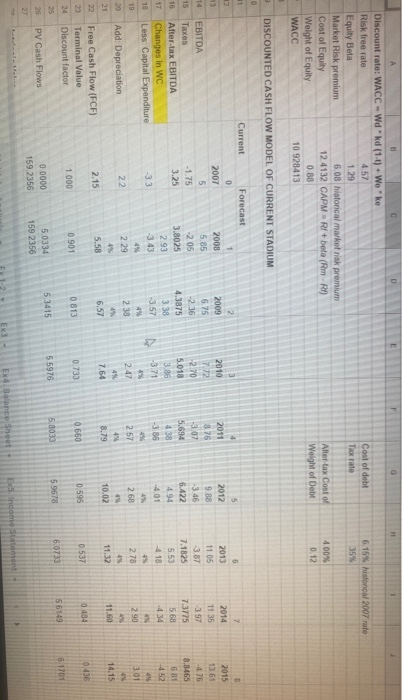

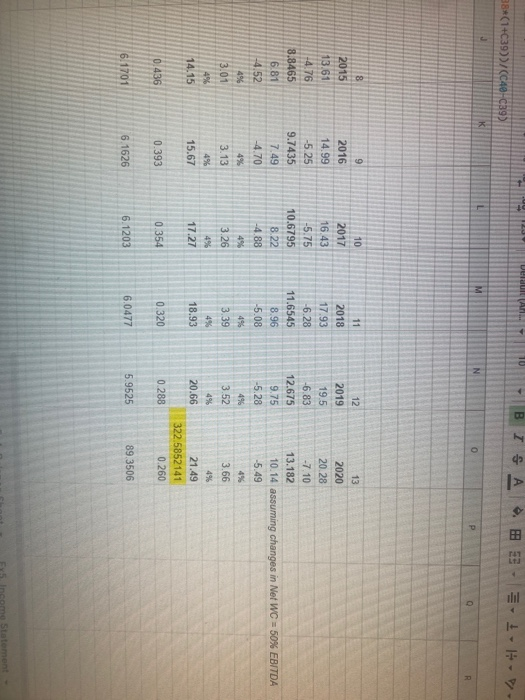

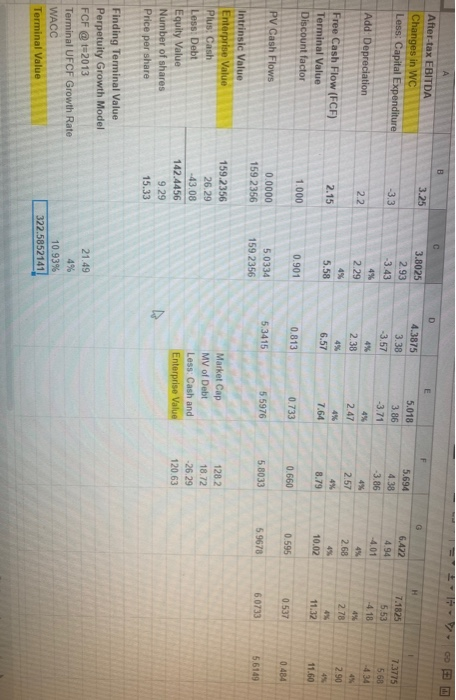

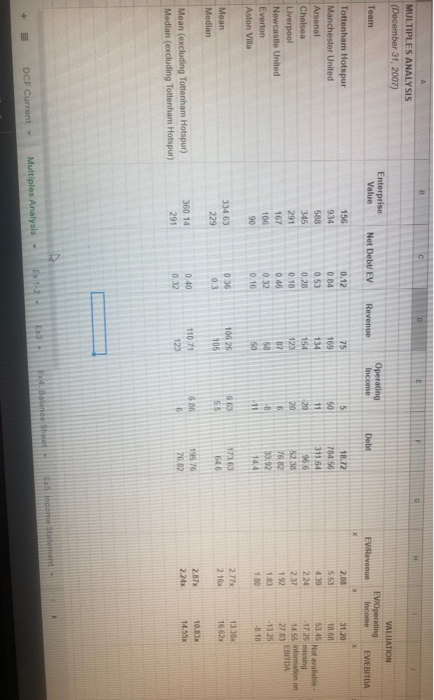

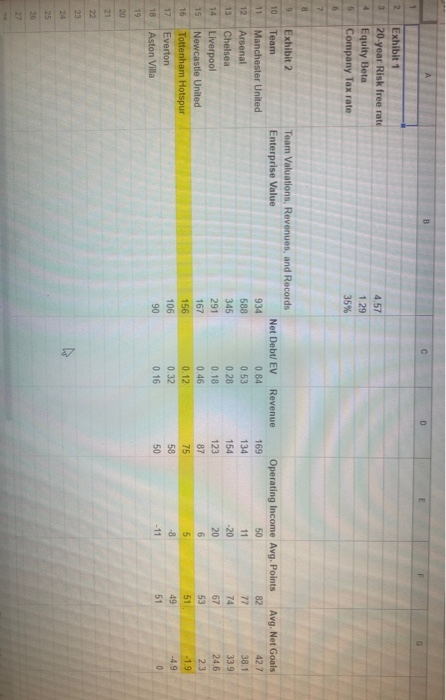

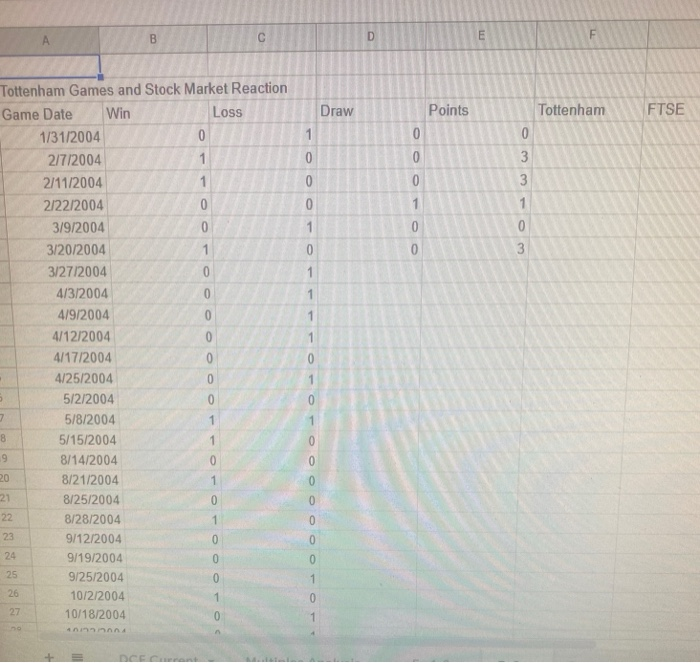

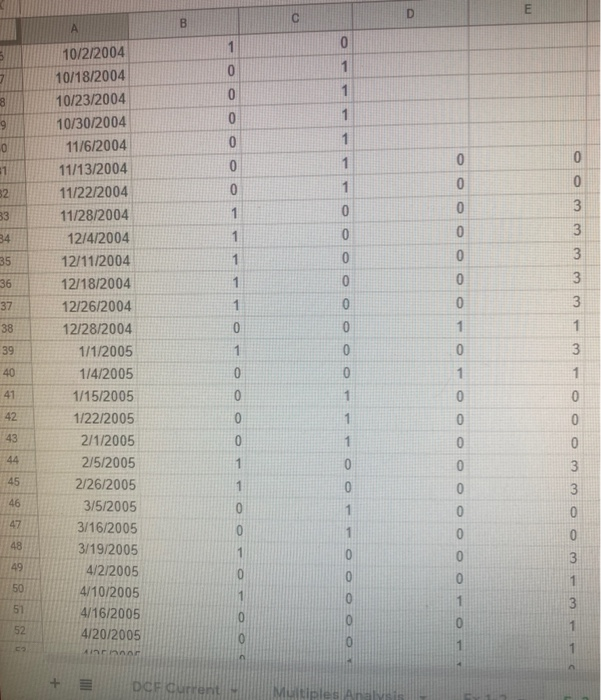

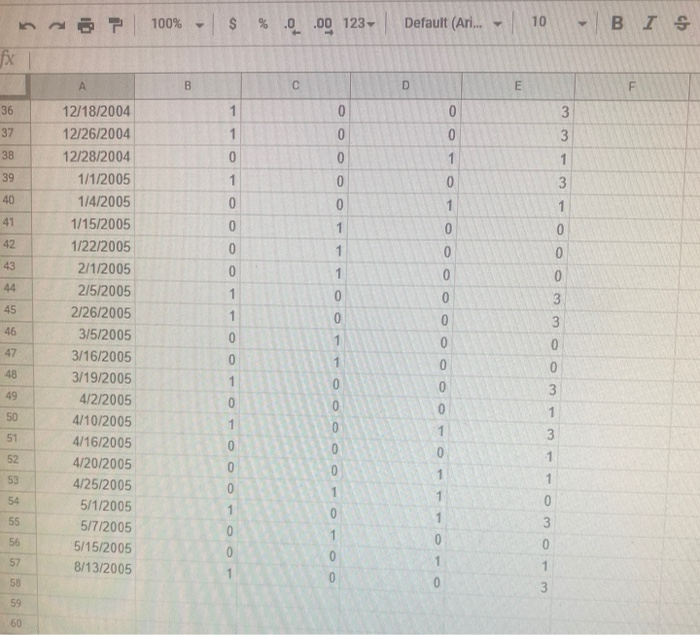

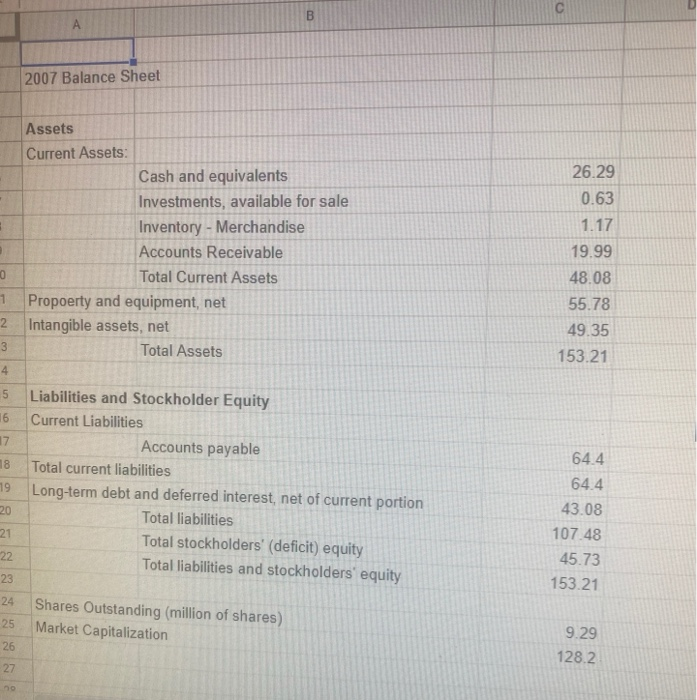

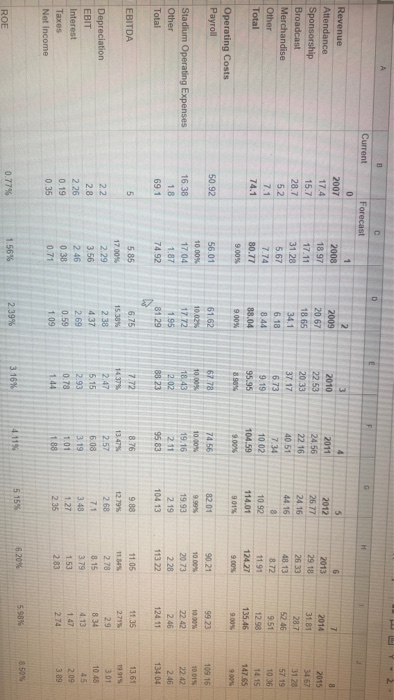

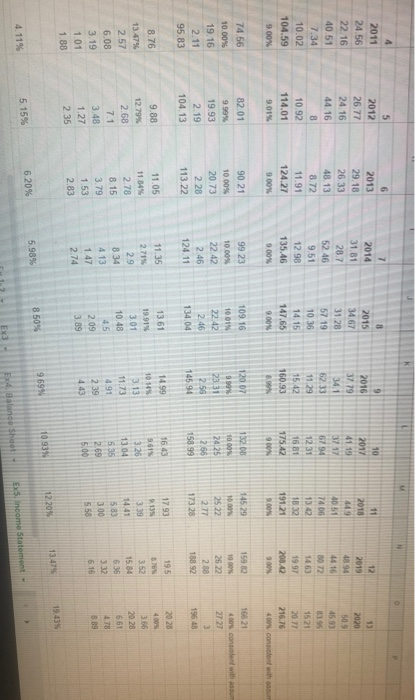

Cost of debt 6.15% histoncal 2007 rate 35% Tax rate Discount rate: WACC - Wdkd (1-1) + Weke Risk free rate 4.57 Equity Beta 1.29 Market Risk premium 6.08 historical market risk premium Cost of Equity 12.4132 CAPM = R + beta (Rm - RY) Weight of Equity 0.88 WACC 10.928413 After-tax Cost of Weight of Debt 400% 0.12 DISCOUNTED CASH FLOW MODEL OF CURRENT STADIUM 11 Current Forecast 5 6 7 1 0 12 13 14 2007 5 -1.75 3.25 EBITDA Taxes After-tax EBITDA Changes in WC Less: Capital Expenditure 2008 5.85 -205 3.8025 2.93 -3.43 4% 2.29 49 5.58 2 2009 6.75 -2.36 4.3875 3.38 -3.57 4% 2.38 15 16 17 2010 7172 2.70 5.018 3.86 -3.71 4 2.47 4% 7.64 2011 8.76 -3.07 5,694 438 -3.86 4 257 49 8.79 2013 11 05 -3.87 7.1825 5.53 -4.18 2012 9.88 -3.46 6.422 4.94 -4.01 2014 1135 3.97 7,3775 568 -4.34 8 2015 13 61 -4.76 8,8465 681 452 -33 18 19 49 2.78 3.01 2.90 268 2.2 Add: Depreciation 4 4 49 10.02 14.15 21 11.60 11.32 2.15 6.57 Free Cash Flow (FCF) Terminal Value Discount factor 0,436 0.484 0.537 0.595 0 660 0.733 0813 0901 1.000 24 6 1701 56149 25 6.0733 5.9678 5,8033 55976 53415 26 PV Cash Flows 0.0000 159.2356 5,0334 159 2356 2 Ethdoo Stato Ex Balance Sheet DE DUAL 10 BISA BE 38*(1+C39))/(C40-C39) - - HD M N 8 11 13 2020 2015 13.61 -4.76 8.8465 6.81 -4.52 496 3.01 4% 14.15 9 2016 14.99 -5.25 9.7435 7.49 -4.70 10 2017 16.43 -5.75 10.6795 8.22 -4.88 2018 17.93 -6.28 11.6545 8.96 -5.08 12 2019 19.5 -6.83 12.675 9.75 -5.28 20.28 -7.10 13.182 10.14 assuming changes in Net WC -50% EBITDA -5.49 49 3.13 4% 3.26 49% 3.39 496 3.52 4% 3.66 4% 4% 4% 4% 15.67 17.27 18.93 20.66 496 21.49 322.5852141 0.260 0.436 0.393 0.354 0.320 0.288 6.1701 89.3506 6.1626 6.0477 6.1203 5.9525 Income Statoment B D E 3.25 g After-tax EBITDA Changes in WC Less: Capital Expenditure 5.018 4.3875 3.38 -3.57 -3.3 3.86 -3.71 3.8025 2.93 -3.43 4% 2.29 4% 5.58 5.694 4.38 -3.86 6.422 4.94 4.01 4% 2.68 7.1825 5,53 -4.18 Add Depreciation 7.3775 5.68 -4.34 2.2 4% 2.38 4% 2.47 4% 278 49 2.90 2.15 Free Cash Flow (FCF) Terminal Value Discount factor 2.57 4% 8.79 4% 7.64 6.57 44 10.02 11.32 11.60 1.000 0.901 0.813 0.733 0.660 0.595 0.537 0.484 PV Cash Flows 0.0000 159 2356 5.0334 159.2356 5.3415 5.5976 5.8033 5.9678 6.0733 5.6149 Intrinsic Value Enterprise Value Plus Cash Less: Debt Equity Value Number of shares Price per share 159.2356 26.29 -43.08 142.4456 9.29 15.33 Market Cap MV of Debt Less: Cash and Enterprise Value 1282 18.72 -26.29 120.63 Finding Terminal Value Perpetuity Growth Model FCF @t=2013 Terminal UFCF Growth Rate WACC Terminal Value 21.49 4% 10.93% 322.5852141 C. H MULTIPLES ANALYSIS (December 31, 2007) Enterprise Value Team VALUATION EV/Operating Income EVEBITDA Net Debu EV Operating Income Revenue Debt EVRevenue y 75 169 5 50 11 31.20 18 60 53.45 Not available 20 1725 mising Tottenham Hotspur Manchester United Arsenal Chelsea Liverpool Newcastle United Everton Aston Villa 156 934 588 345 291 167 106 90 0.12 0.84 0.53 0.28 0.18 0.46 0.32 0.16 18.72 784 56 311 64 966 5238 7602 33.92 144 134 154 123 87 58 50 2.00 5.53 439 2.24 237 192 183 130 20 145 Information on 2703 EBITDA -13.25 18 11 334.63 229 0.36 0.3 Mean Median 10825 105 603 55 2778 2.16 1710 646 1662 5 36 360.14 291 0.40 0.32 195 76 76.82 110 71 123 2.87 2.24 Mean (excluding Tottenham Hotspur) Median (excluding Tottenham Hotspur) 1083 14.55 6 Endome Stiitement EX 1-2 Ex3 4. Banco Shit Multiples Analysis DCF Current B c D 1 2 3 4 Exhibit 1 20-year Risk free rate Equity Beta Company Tax rate 4.57 1.29 35% 5 7 9 10 Revenue 11 12 13 Exhibit 2 Team Manchester United Arsenal Chelsea Liverpool Newcastle United Tottenham Hotspur Everton Aston Villa Team Valuations, Revenues, and Records Enterprise Value Net Debt EV 934 0.84 588 0.53 345 0.28 291 0.18 0.46 156 0.12 106 0.32 90 0.16 Operating Income Avg. Points Avg. Net Goals 169 50 82 42.7 134 11 77 38.1 154 -20 74 33.9 123 20 67 24.6 87 6 53 23 75 5 51 58 -8 49 -4.9 50 - 11 51 0 14 15 16 17 167 18 19 20 21 23 24 25 26 B D E F Draw Points Tottenham FTSE 1 0 0 0 0 0 0 0 1 3 3 1 0 3 1 1 0 0 0 Tottenham Games and Stock Market Reaction Game Date Win Loss 1/31/2004 0 2/7/2004 1 2/11/2004 1 2/22/2004 0 3/9/2004 0 3/20/2004 1 3/27/2004 0 4/3/2004 0 4/9/2004 0 4/12/2004 0 4/17/2004 0 4/25/2004 0 5/2/2004 0 7 5/8/2004 1 5/15/2004 9 8/14/2004 0 20 8/21/2004 1 21 8/25/2004 0 22 8/28/2004 1 23 9/12/2004 0 24 9/19/2004 0 25 9/25/2004 0 26 10/2/2004 1 27 10/18/2004 0 1 1 0 1 0 1 8 0 0 0 0 0 0 0 1 0 1 Ann D m B 0 0 1 0 1 0 1 9 0 1 0 1 0 81 0 1 32 0 1 0 0 3 3 3 33 34 1 3 3 35 1 1 0 0 0 0 0 0 0 0 0 1 0 1 0 3 36 37 1 0 38 10/2/2004 10/18/2004 10/23/2004 10/30/2004 11/6/2004 11/13/2004 11/22/2004 11/28/2004 12/4/2004 12/11/2004 12/18/2004 12/26/2004 12/28/2004 1/1/2005 1/4/2005 1/15/2005 1/22/2005 2/1/2005 2/5/2005 2/26/2005 3/5/2005 3/16/2005 3/19/2005 4/2/2005 4/10/2005 4/16/2005 4/20/2005 0 39 40 3 1 3 1 0 1 0 0 0 0 41 0 0 0 1 1 1 0 42 0 43 44 0 0 1 0 0 3 3 0 45 1 0 46 0 1 0 47 0 1 0 0 48 1 0 3 49 0 0 0 50 1 0 1 3 1 5 0 3 1 0 0 52 0 0 2 Anar DCF current Multiple 100% - $ ae 0.00123 Default (Ari.. 10 - BIS fx A B C D E F 36 1 0 3 0 0 3 3 37 0 1 0 38 0 1 1 39 0 0 0 40 1 41 1 0 0 0 0 3 1 0 0 1 0 42 1 43 1 0 0 0 0 44 1 0 3 45 1 0 3 46 12/18/2004 12/26/2004 12/28/2004 1/1/2005 1/4/2005 1/15/2005 1/22/2005 2/1/2005 2/5/2005 2/26/2005 3/5/2005 3/16/2005 3/19/2005 4/2/2005 4/10/2005 4/16/2005 4/20/2005 4/25/2005 5/1/2005 5/7/2005 5/15/2005 8/13/2005 0 1 0 47 0 1 0 0 48 1 0 0 49 0 0 0 50 1 0 1 3 1 3 1 51 0 52 0 0 0 1 53 1 0 1 54 1 0 0 3 55 1 0 1 56 0 0 0 57 0 1 1 1 0 58 0 3 59 60 B 2007 Balance Sheet 26.29 Assets Current Assets: Cash and equivalents Investments, available for sale Inventory - Merchandise Accounts Receivable 0 Total Current Assets Propoerty and equipment, net 2 Intangible assets, net 3 Total Assets 4 0.63 1.17 19.99 48.08 55.78 49.35 153.21 1 5 16 Liabilities and Stockholder Equity Current Liabilities 17 Accounts payable 18 Total current liabilities 19 Long-term debt and deferred interest, net of current portion Total liabilities Total stockholders' (deficit) equity 22 Total liabilities and stockholders' equity 23 20 64.4 64.4 43.08 107.48 45.73 153.21 21 24 Shares Outstanding (million of shares) Market Capitalization 25 26 9.29 128.2 27 2 D E Current Forecast o H 1 7 4 2011 24.56 Revenue Attendance Sponsorship Broadcast Merchandise Other Total 22.16 2007 17.4 15.7 28.7 52 7.1 74.1 2008 18.97 17.11 31.28 5.67 7.74 80.77 9.00% 2 2009 20.67 18.65 34.1 6.18 844 88.04 9.00% 3 2010 22.53 20.33 37.17 6.73 9.19 95.95 8.90% 40.51 7.34 10.02 104.59 9.00% 5 2012 26.77 24.16 44.16 8 10.92 114.01 6 2013 29.18 26 33 48 13 8.72 11.91 124.27 9.00 2014 31.81 28.7 5246 9.51 12.90 135.46 8 2015 34 67 31.28 57 19 10.36 14.15 147.65 9.01% 9005 9.00% Operating Costs Payroll 50.92 67.78 90.21 10.00% Stadium Operating Expenses Other Total 16 38 1.8 69.1 56 01 10.00% 17.04 1.87 74.92 51.62 10.02% 17.72 1.95 81 29 18.43 2.02 88 23 74 56 10.00% 19.16 2.11 9583 82 01 9.99% 19.93 2.19 104.13 10.00% 20.73 2.28 113 22 9923 10.00% 22.42 2.46 124.11 109.15 10.01% 2242 2.46 134.04 EBITDA 5 6.75 8.76 13 61 585 17.00% 2.29 3.56 2.46 0.38 0.71 13.47% 2.57 6.08 9.88 12.79% 268 71 772 14 375 2.47 5.15 2.93 0.73 1.44 2.2 28 2 26 0.19 0.35 Depreciation EBIT Interest Taxes Net Income 15.38% 2.38 4.37 2.69 0.59 1.09 1135 2.71% 29 8.34 4.13 11.05 11.55 2.78 8.15 3.79 1.53 2.83 1991 3.01 10.48 45 2.09 3.89 3.19 1.01 1.88 3.43 1.27 2.35 2.74 5.98 6.209 4 11% 5 15% 2.39% 3.16% 1.56% 0.77% ROE 4 10 2017 2011 24.56 22 16 40.51 7.34 10.02 104.59 5 2012 26.77 24 16 44.16 8 10.92 114.01 9.01% 6 2013 29.18 2633 48.13 8.72 11.91 124.27 7 2014 31.81 28.7 52.46 9.51 12.98 135.46 2015 34 67 31.28 57 19 10.36 14.15 147.65 9 2016 37 79 34.1 62 33 11.29 15.42 160.93 8.95 41 19 37 17 6794 1231 16 81 17542 11 2018 449 40.51 7406 13 42 1832 191.21 9.00 12 2019 4894 4416 3072 1463 19.97 208.42 900 13 2020 509 45.90 8355 15 21 20 77 216.76 40 content with som 9.00% 9.00 9.00% 9.00% 90% 74.56 10.00% 19.16 2.11 95 83 82.01 9.99% 19.93 2.19 104.13 90.21 1000% 20.73 2.28 113.22 99.23 100% 22.42 2.46 124.11 109.16 10 DIN 22.42 2.46 134.04 120 07 9.99% 23 31 2.56 145.94 132.00 10. 24 25 2.66 158 99 145.29 10.00 25.22 2.77 173 28 1592 1000 26.22 2.88 18892 16621 400s condit with a 2727 3 1968 1793 1643 13.61 11.05 9615 13 20 28 4.00% 3.66 20.28 11.34% 2.78 195 8 3.52 15.84 635 8.76 13.47% 2.57 6.08 3.19 1.01 1.88 9.88 12.79% 2.66 7.1 3.48 1.27 2.35 11.35 2.71% 29 8 34 4.13 1.47 2.74 14.99 100% 3.13 11.73 4.91 2.39 4.43 19.91% 3.01 10.48 4.5 2.09 3.89 8.15 3.79 1.53 2.83 3.39 14.41 583 300 550 3.26 13 04 5.35 269 5.00 332 4.78 8.89 6.16 13.47% 12.20% 1093 9 69% 8 50% 8 50% 5.98% 6 20% 5.15% 4 11% Exs, income Statement Ex3 EX4 Balance Sheet Cost of debt 6.15% histoncal 2007 rate 35% Tax rate Discount rate: WACC - Wdkd (1-1) + Weke Risk free rate 4.57 Equity Beta 1.29 Market Risk premium 6.08 historical market risk premium Cost of Equity 12.4132 CAPM = R + beta (Rm - RY) Weight of Equity 0.88 WACC 10.928413 After-tax Cost of Weight of Debt 400% 0.12 DISCOUNTED CASH FLOW MODEL OF CURRENT STADIUM 11 Current Forecast 5 6 7 1 0 12 13 14 2007 5 -1.75 3.25 EBITDA Taxes After-tax EBITDA Changes in WC Less: Capital Expenditure 2008 5.85 -205 3.8025 2.93 -3.43 4% 2.29 49 5.58 2 2009 6.75 -2.36 4.3875 3.38 -3.57 4% 2.38 15 16 17 2010 7172 2.70 5.018 3.86 -3.71 4 2.47 4% 7.64 2011 8.76 -3.07 5,694 438 -3.86 4 257 49 8.79 2013 11 05 -3.87 7.1825 5.53 -4.18 2012 9.88 -3.46 6.422 4.94 -4.01 2014 1135 3.97 7,3775 568 -4.34 8 2015 13 61 -4.76 8,8465 681 452 -33 18 19 49 2.78 3.01 2.90 268 2.2 Add: Depreciation 4 4 49 10.02 14.15 21 11.60 11.32 2.15 6.57 Free Cash Flow (FCF) Terminal Value Discount factor 0,436 0.484 0.537 0.595 0 660 0.733 0813 0901 1.000 24 6 1701 56149 25 6.0733 5.9678 5,8033 55976 53415 26 PV Cash Flows 0.0000 159.2356 5,0334 159 2356 2 Ethdoo Stato Ex Balance Sheet DE DUAL 10 BISA BE 38*(1+C39))/(C40-C39) - - HD M N 8 11 13 2020 2015 13.61 -4.76 8.8465 6.81 -4.52 496 3.01 4% 14.15 9 2016 14.99 -5.25 9.7435 7.49 -4.70 10 2017 16.43 -5.75 10.6795 8.22 -4.88 2018 17.93 -6.28 11.6545 8.96 -5.08 12 2019 19.5 -6.83 12.675 9.75 -5.28 20.28 -7.10 13.182 10.14 assuming changes in Net WC -50% EBITDA -5.49 49 3.13 4% 3.26 49% 3.39 496 3.52 4% 3.66 4% 4% 4% 4% 15.67 17.27 18.93 20.66 496 21.49 322.5852141 0.260 0.436 0.393 0.354 0.320 0.288 6.1701 89.3506 6.1626 6.0477 6.1203 5.9525 Income Statoment B D E 3.25 g After-tax EBITDA Changes in WC Less: Capital Expenditure 5.018 4.3875 3.38 -3.57 -3.3 3.86 -3.71 3.8025 2.93 -3.43 4% 2.29 4% 5.58 5.694 4.38 -3.86 6.422 4.94 4.01 4% 2.68 7.1825 5,53 -4.18 Add Depreciation 7.3775 5.68 -4.34 2.2 4% 2.38 4% 2.47 4% 278 49 2.90 2.15 Free Cash Flow (FCF) Terminal Value Discount factor 2.57 4% 8.79 4% 7.64 6.57 44 10.02 11.32 11.60 1.000 0.901 0.813 0.733 0.660 0.595 0.537 0.484 PV Cash Flows 0.0000 159 2356 5.0334 159.2356 5.3415 5.5976 5.8033 5.9678 6.0733 5.6149 Intrinsic Value Enterprise Value Plus Cash Less: Debt Equity Value Number of shares Price per share 159.2356 26.29 -43.08 142.4456 9.29 15.33 Market Cap MV of Debt Less: Cash and Enterprise Value 1282 18.72 -26.29 120.63 Finding Terminal Value Perpetuity Growth Model FCF @t=2013 Terminal UFCF Growth Rate WACC Terminal Value 21.49 4% 10.93% 322.5852141 C. H MULTIPLES ANALYSIS (December 31, 2007) Enterprise Value Team VALUATION EV/Operating Income EVEBITDA Net Debu EV Operating Income Revenue Debt EVRevenue y 75 169 5 50 11 31.20 18 60 53.45 Not available 20 1725 mising Tottenham Hotspur Manchester United Arsenal Chelsea Liverpool Newcastle United Everton Aston Villa 156 934 588 345 291 167 106 90 0.12 0.84 0.53 0.28 0.18 0.46 0.32 0.16 18.72 784 56 311 64 966 5238 7602 33.92 144 134 154 123 87 58 50 2.00 5.53 439 2.24 237 192 183 130 20 145 Information on 2703 EBITDA -13.25 18 11 334.63 229 0.36 0.3 Mean Median 10825 105 603 55 2778 2.16 1710 646 1662 5 36 360.14 291 0.40 0.32 195 76 76.82 110 71 123 2.87 2.24 Mean (excluding Tottenham Hotspur) Median (excluding Tottenham Hotspur) 1083 14.55 6 Endome Stiitement EX 1-2 Ex3 4. Banco Shit Multiples Analysis DCF Current B c D 1 2 3 4 Exhibit 1 20-year Risk free rate Equity Beta Company Tax rate 4.57 1.29 35% 5 7 9 10 Revenue 11 12 13 Exhibit 2 Team Manchester United Arsenal Chelsea Liverpool Newcastle United Tottenham Hotspur Everton Aston Villa Team Valuations, Revenues, and Records Enterprise Value Net Debt EV 934 0.84 588 0.53 345 0.28 291 0.18 0.46 156 0.12 106 0.32 90 0.16 Operating Income Avg. Points Avg. Net Goals 169 50 82 42.7 134 11 77 38.1 154 -20 74 33.9 123 20 67 24.6 87 6 53 23 75 5 51 58 -8 49 -4.9 50 - 11 51 0 14 15 16 17 167 18 19 20 21 23 24 25 26 B D E F Draw Points Tottenham FTSE 1 0 0 0 0 0 0 0 1 3 3 1 0 3 1 1 0 0 0 Tottenham Games and Stock Market Reaction Game Date Win Loss 1/31/2004 0 2/7/2004 1 2/11/2004 1 2/22/2004 0 3/9/2004 0 3/20/2004 1 3/27/2004 0 4/3/2004 0 4/9/2004 0 4/12/2004 0 4/17/2004 0 4/25/2004 0 5/2/2004 0 7 5/8/2004 1 5/15/2004 9 8/14/2004 0 20 8/21/2004 1 21 8/25/2004 0 22 8/28/2004 1 23 9/12/2004 0 24 9/19/2004 0 25 9/25/2004 0 26 10/2/2004 1 27 10/18/2004 0 1 1 0 1 0 1 8 0 0 0 0 0 0 0 1 0 1 Ann D m B 0 0 1 0 1 0 1 9 0 1 0 1 0 81 0 1 32 0 1 0 0 3 3 3 33 34 1 3 3 35 1 1 0 0 0 0 0 0 0 0 0 1 0 1 0 3 36 37 1 0 38 10/2/2004 10/18/2004 10/23/2004 10/30/2004 11/6/2004 11/13/2004 11/22/2004 11/28/2004 12/4/2004 12/11/2004 12/18/2004 12/26/2004 12/28/2004 1/1/2005 1/4/2005 1/15/2005 1/22/2005 2/1/2005 2/5/2005 2/26/2005 3/5/2005 3/16/2005 3/19/2005 4/2/2005 4/10/2005 4/16/2005 4/20/2005 0 39 40 3 1 3 1 0 1 0 0 0 0 41 0 0 0 1 1 1 0 42 0 43 44 0 0 1 0 0 3 3 0 45 1 0 46 0 1 0 47 0 1 0 0 48 1 0 3 49 0 0 0 50 1 0 1 3 1 5 0 3 1 0 0 52 0 0 2 Anar DCF current Multiple 100% - $ ae 0.00123 Default (Ari.. 10 - BIS fx A B C D E F 36 1 0 3 0 0 3 3 37 0 1 0 38 0 1 1 39 0 0 0 40 1 41 1 0 0 0 0 3 1 0 0 1 0 42 1 43 1 0 0 0 0 44 1 0 3 45 1 0 3 46 12/18/2004 12/26/2004 12/28/2004 1/1/2005 1/4/2005 1/15/2005 1/22/2005 2/1/2005 2/5/2005 2/26/2005 3/5/2005 3/16/2005 3/19/2005 4/2/2005 4/10/2005 4/16/2005 4/20/2005 4/25/2005 5/1/2005 5/7/2005 5/15/2005 8/13/2005 0 1 0 47 0 1 0 0 48 1 0 0 49 0 0 0 50 1 0 1 3 1 3 1 51 0 52 0 0 0 1 53 1 0 1 54 1 0 0 3 55 1 0 1 56 0 0 0 57 0 1 1 1 0 58 0 3 59 60 B 2007 Balance Sheet 26.29 Assets Current Assets: Cash and equivalents Investments, available for sale Inventory - Merchandise Accounts Receivable 0 Total Current Assets Propoerty and equipment, net 2 Intangible assets, net 3 Total Assets 4 0.63 1.17 19.99 48.08 55.78 49.35 153.21 1 5 16 Liabilities and Stockholder Equity Current Liabilities 17 Accounts payable 18 Total current liabilities 19 Long-term debt and deferred interest, net of current portion Total liabilities Total stockholders' (deficit) equity 22 Total liabilities and stockholders' equity 23 20 64.4 64.4 43.08 107.48 45.73 153.21 21 24 Shares Outstanding (million of shares) Market Capitalization 25 26 9.29 128.2 27 2 D E Current Forecast o H 1 7 4 2011 24.56 Revenue Attendance Sponsorship Broadcast Merchandise Other Total 22.16 2007 17.4 15.7 28.7 52 7.1 74.1 2008 18.97 17.11 31.28 5.67 7.74 80.77 9.00% 2 2009 20.67 18.65 34.1 6.18 844 88.04 9.00% 3 2010 22.53 20.33 37.17 6.73 9.19 95.95 8.90% 40.51 7.34 10.02 104.59 9.00% 5 2012 26.77 24.16 44.16 8 10.92 114.01 6 2013 29.18 26 33 48 13 8.72 11.91 124.27 9.00 2014 31.81 28.7 5246 9.51 12.90 135.46 8 2015 34 67 31.28 57 19 10.36 14.15 147.65 9.01% 9005 9.00% Operating Costs Payroll 50.92 67.78 90.21 10.00% Stadium Operating Expenses Other Total 16 38 1.8 69.1 56 01 10.00% 17.04 1.87 74.92 51.62 10.02% 17.72 1.95 81 29 18.43 2.02 88 23 74 56 10.00% 19.16 2.11 9583 82 01 9.99% 19.93 2.19 104.13 10.00% 20.73 2.28 113 22 9923 10.00% 22.42 2.46 124.11 109.15 10.01% 2242 2.46 134.04 EBITDA 5 6.75 8.76 13 61 585 17.00% 2.29 3.56 2.46 0.38 0.71 13.47% 2.57 6.08 9.88 12.79% 268 71 772 14 375 2.47 5.15 2.93 0.73 1.44 2.2 28 2 26 0.19 0.35 Depreciation EBIT Interest Taxes Net Income 15.38% 2.38 4.37 2.69 0.59 1.09 1135 2.71% 29 8.34 4.13 11.05 11.55 2.78 8.15 3.79 1.53 2.83 1991 3.01 10.48 45 2.09 3.89 3.19 1.01 1.88 3.43 1.27 2.35 2.74 5.98 6.209 4 11% 5 15% 2.39% 3.16% 1.56% 0.77% ROE 4 10 2017 2011 24.56 22 16 40.51 7.34 10.02 104.59 5 2012 26.77 24 16 44.16 8 10.92 114.01 9.01% 6 2013 29.18 2633 48.13 8.72 11.91 124.27 7 2014 31.81 28.7 52.46 9.51 12.98 135.46 2015 34 67 31.28 57 19 10.36 14.15 147.65 9 2016 37 79 34.1 62 33 11.29 15.42 160.93 8.95 41 19 37 17 6794 1231 16 81 17542 11 2018 449 40.51 7406 13 42 1832 191.21 9.00 12 2019 4894 4416 3072 1463 19.97 208.42 900 13 2020 509 45.90 8355 15 21 20 77 216.76 40 content with som 9.00% 9.00 9.00% 9.00% 90% 74.56 10.00% 19.16 2.11 95 83 82.01 9.99% 19.93 2.19 104.13 90.21 1000% 20.73 2.28 113.22 99.23 100% 22.42 2.46 124.11 109.16 10 DIN 22.42 2.46 134.04 120 07 9.99% 23 31 2.56 145.94 132.00 10. 24 25 2.66 158 99 145.29 10.00 25.22 2.77 173 28 1592 1000 26.22 2.88 18892 16621 400s condit with a 2727 3 1968 1793 1643 13.61 11.05 9615 13 20 28 4.00% 3.66 20.28 11.34% 2.78 195 8 3.52 15.84 635 8.76 13.47% 2.57 6.08 3.19 1.01 1.88 9.88 12.79% 2.66 7.1 3.48 1.27 2.35 11.35 2.71% 29 8 34 4.13 1.47 2.74 14.99 100% 3.13 11.73 4.91 2.39 4.43 19.91% 3.01 10.48 4.5 2.09 3.89 8.15 3.79 1.53 2.83 3.39 14.41 583 300 550 3.26 13 04 5.35 269 5.00 332 4.78 8.89 6.16 13.47% 12.20% 1093 9 69% 8 50% 8 50% 5.98% 6 20% 5.15% 4 11% Exs, income Statement Ex3 EX4 Balance Sheet

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts