Answered step by step

Verified Expert Solution

Question

1 Approved Answer

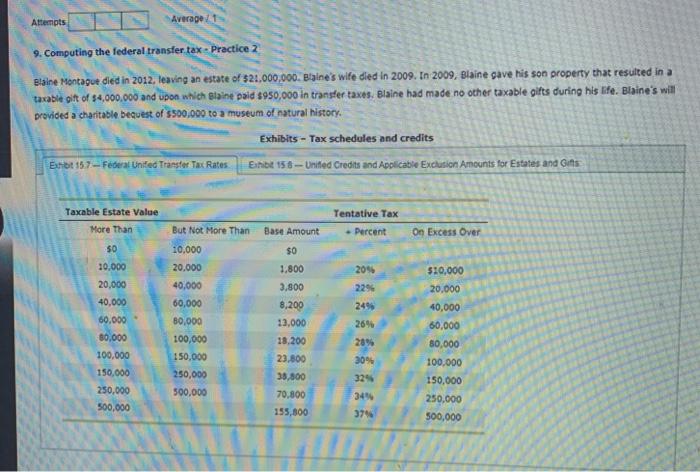

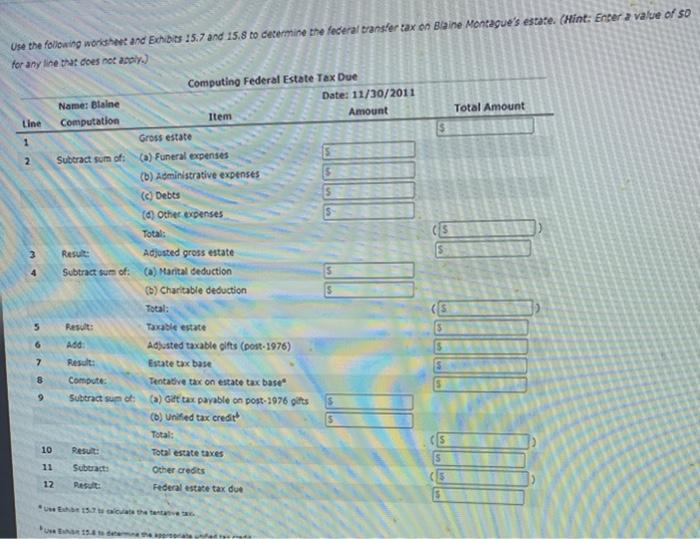

Attempts Average 1 9. Computing the federal transfer tax - Practice Blaine Montague died in 2012, leaving an estate of $21,000,000. Bhaine's wife died in

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Currency Internationalization Global Experiences And Implications For The Renminbi

Authors: Wensheng Peng, Chang Shu

2nd Edition

0230580491, 9780230580497