Answered step by step

Verified Expert Solution

Question

1 Approved Answer

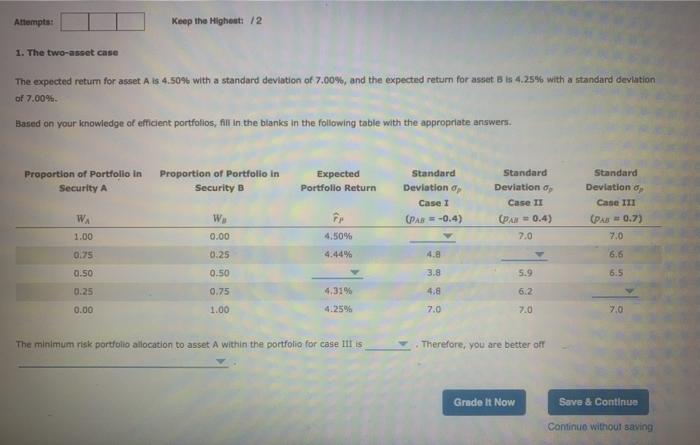

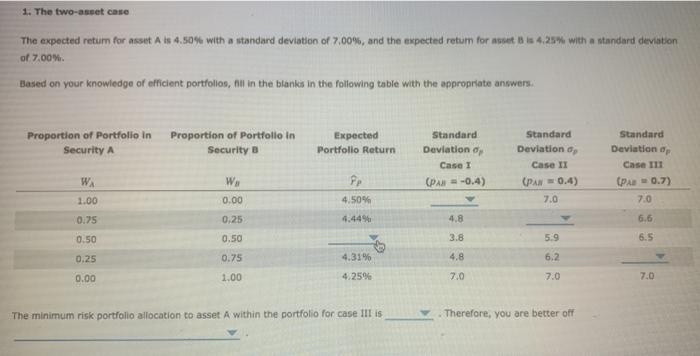

Attempts: Keep the Highest / 2 1. The two-asset case The expected return for asset A is 4.5094 with a standard deviation of 7.00%, and

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Valuation Measuring And Managing The Value Of Companies

Authors: McKinsey & Company Inc., Tom Copeland, Tim Koller, Jack Murrin

3rd Edition