Question: a-What would be the $SDR bid if the SDR appreciates 15% against the dollar? What would be the SDR/$ offer rate if the SDR appreciates

a-What would be the $SDR bid if the SDR appreciates 15% against the dollar? What would be the SDR/$ offer rate if the SDR appreciates 15%? SDR is Special Drawing Rights, a basket currency precursor to the Euro. This requires you to use Exhibit 2, which does not have any SDR. It only has FF, DM, and JPY. You must try all combinations. A "dollar discount" is a situation where the U.S. dollar trades at a forward discount against another currency.

b- Which currencies are at a dollar discount and which are at a dollar premium? What are the outright forward rates for the pound? For the French franc? Using the midpoints of bid-ask spreads, what are the forward premia or discounts on an annualized percentage basis for both these currencies?

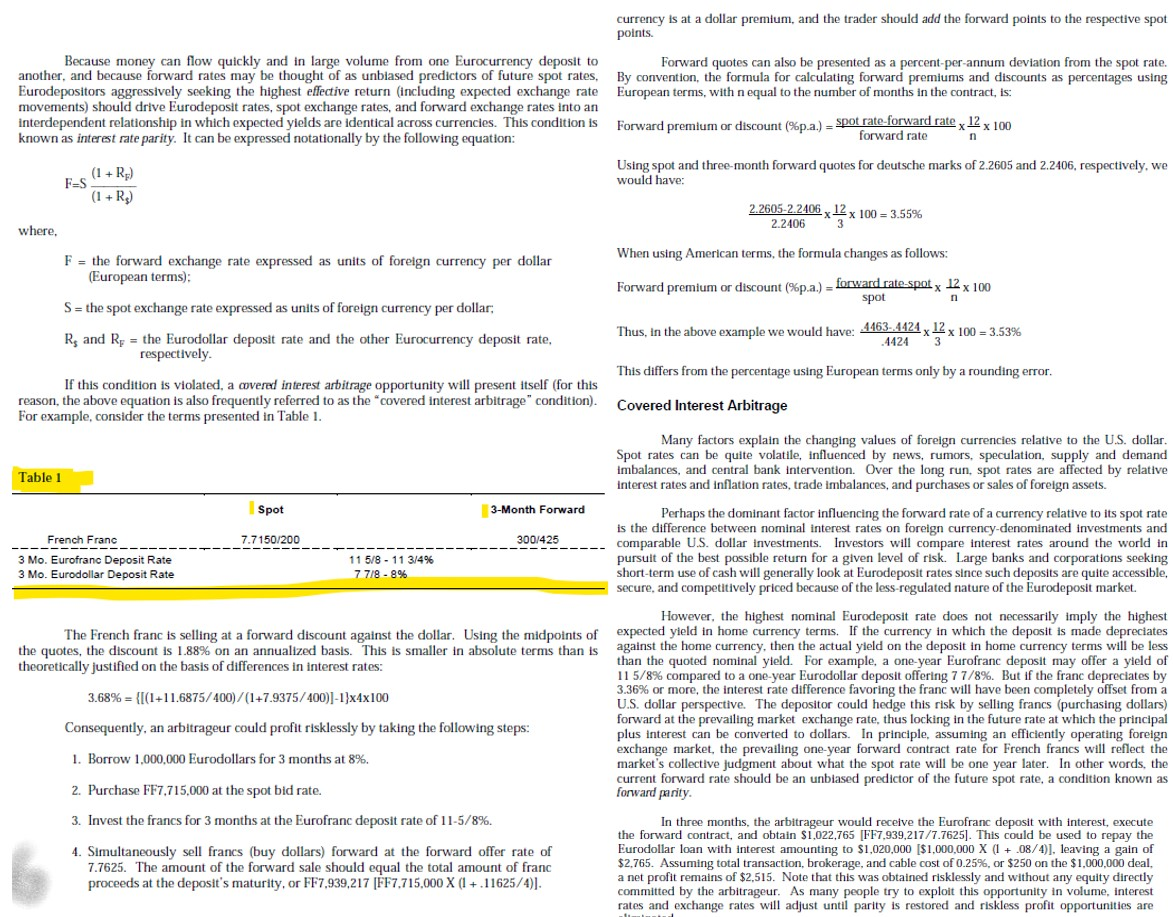

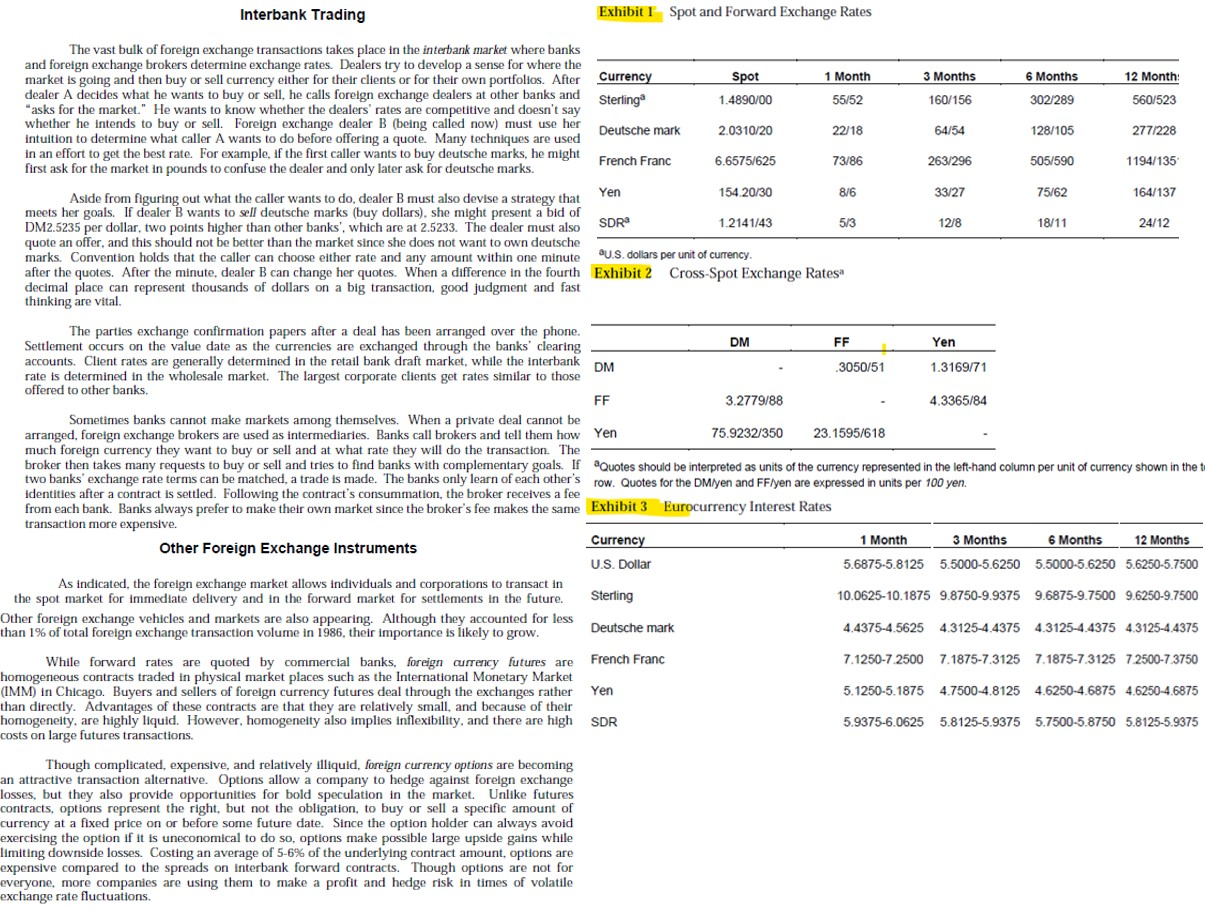

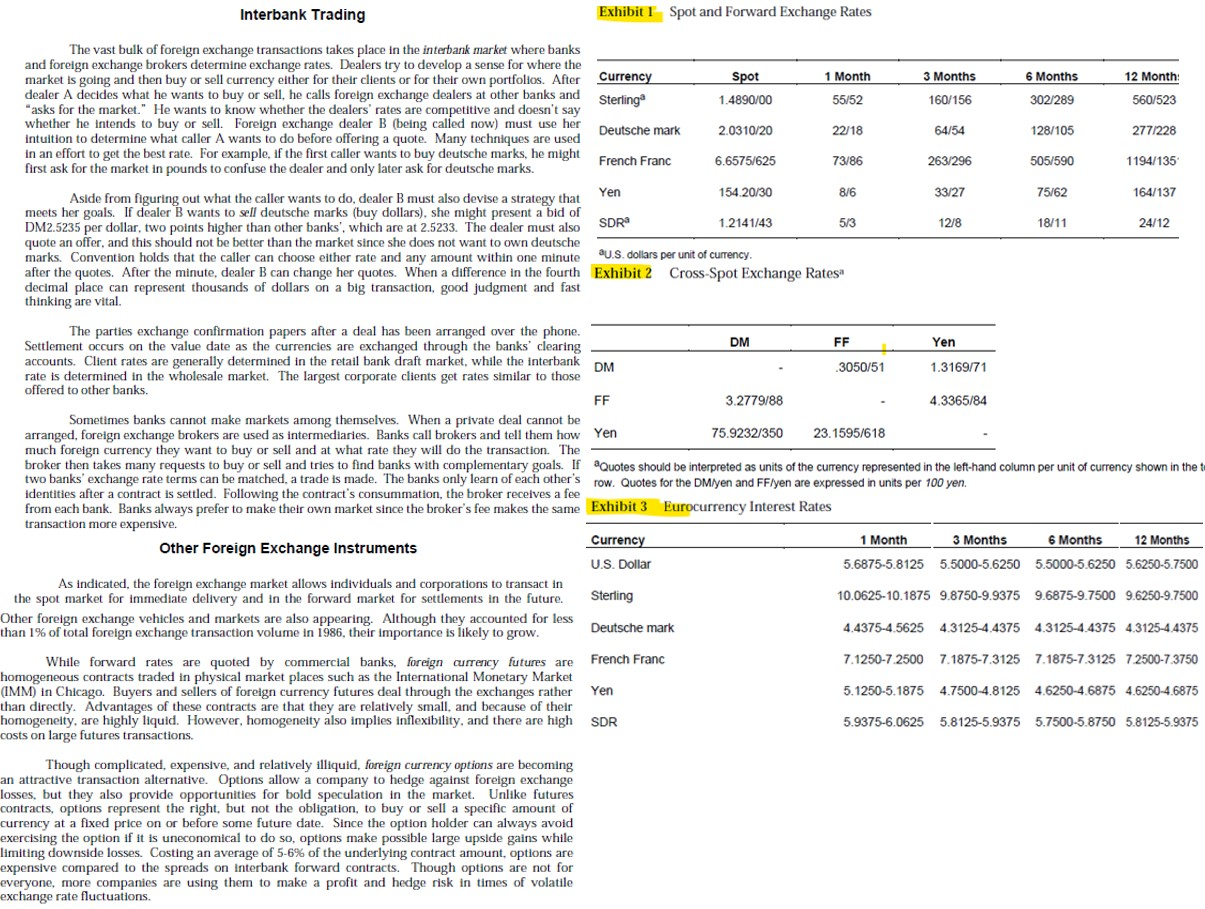

currency is at a dollar premium, and the trader should add the forward points to the respective spot points. Because money can flow quickly and in large volume from one Eurocurrency deposit to another, and because forward rates may be thought of as unbiased predictors of future spot rates, Eurodepositors aggressively seeking the highest effective return (including expected exchange rate movements) should drive Eurodeposit rates, spot exchange rates, and forward exchange rates into an interdependent relationship in which expected yields are identical across currencies. This condition is known as interest rate parity. It can be expressed notationally by the following equation: Forward quotes can also be presented as a percent-per-annum deviation from the spot rate. By convention, the formula for calculating forward premiums and discounts as percentages using European terms, with n equal to the number of months in the contract, is: Forward premium or discount (%p.a.) spot rate-forward rate x 12 x 100 forward rate (1 + Rp) (1 + R) Using spot and three-month forward quotes for deutsche marks of 2.2605 and 2.2406, respectively, we would have: F-S 2.2605-2.2406 x 12 x 100 = 3.55% 2.2406 3 where, When using American terms, the formula changes as follows: F = the forward exchange rate expressed as units of foreign currency per dollar (European terms); n S = the spot exchange rate expressed as units of foreign currency per dollar; Rs and Rp = the Eurodollar deposit rate and the other Eurocurrency deposit rate, respectively. Forward premium or discount (%p.a.) forward rate-spotx 12 x 100 spot Thus, in the above example we would have: 4463..4424 x 12 x 100 - 3.53% .4424 3 This differs from the percentage using European terms only by a rounding error. If this condition is violated, a covered interest arbitrage opportunity will present itself (for this reason, the above equation is also frequently referred to as the covered interest arbitrage" condition) For example, consider the terms presented in Table 1. Covered Interest Arbitrage Table 1 Spot 3-Month Forward 7.7150/200 300/425 --- French Franc 3 Mo. Eurofranc Deposit Rate 3 Mo. Eurodollar Deposit Rate 11 5/8 - 11 3/4% 7 7/8-8% The French franc is selling at a forward discount against the dollar. Using the midpoints of the quotes, the discount is 1.88% on an annualized basis. This is smaller in absolute terms than is theoretically justified on the basis of differences in interest rates: 3.68% = {[(1+11.6875/400)/(1+7.9375/400))-1}x4x100 Consequently, an arbitrageur could profit risklessly by taking the following steps: Many factors explain the changing values of foreign currencies relative to the U.S. dollar. Spot rates can be quite volatile, influenced by news, rumors, speculation, supply and demand imbalances, and central bank intervention. Over the long run, spot rates are affected by relative interest rates and inflation rates, trade imbalances, and purchases or sales of foreign assets. Perhaps the dominant factor influencing the forward rate of a currency relative to its spot rate is the difference between nominal interest rates on foreign currency-denominated investments and comparable U.S. dollar investments. Investors will compare interest rates around the world in pursuit of the best possible return for a given level of risk. Large banks and corporations seeking short-term use of cash will generally look at Eurodeposit rates since such deposits are quite accessible, secure, and competitively priced because of the less-regulated nature of the Eurodeposit market. However, the highest nominal Eurodeposit rate does not necessarily imply the highest expected yield in home currency terms. If the currency in which the deposit is made depreciates against the home currency, then the actual yield on the deposit in home currency terms will be less than the quoted nominal yield. For example, a one-year Eurofranc deposit may offer a yield of 11 5/8% compared to a one-year Eurodollar deposit offering 7 7/8%. But if the franc depreciates by 3.36% or more, the interest rate difference favoring the franc will have been completely offset from a U.S. dollar perspective. The depositor could hedge this risk by selling francs (purchasing dollars) forward at the prevailing market exchange rate, thus locking in the future rate at which the principal plus interest can be converted to dollars. In principle, assuming an efficiently operating foreign exchange market, the prevailing one-year forward contract rate for French francs will reflect the market's collective judgment about what the spot rate will be one year later. In other words, the current forward rate should be an unbiased predictor of the future spot rate, a condition known as forward parity. In three months, the arbitrageur would receive the Eurofranc deposit with interest, execute the forward contract, and obtain $1,022,765 [FF7,939,217/7.7625]. This could be used to repay the Eurodollar loan with interest amounting to $1,020,000 [$1,000,000 X (1 + 08/4)], leaving a gain of $2,765. Assuming total transaction, brokerage, and cable cost of 0.25%, or $250 on the $1,000,000 deal, a net profit remains of $2,515. Note that this was obtained risklessly and without any equity directly committed by the arbitrageur. As many people try to exploit this opportunity in volume, interest rates and exchange rates will adjust until parity is restored and riskless profit opportunities are 1. Borrow 1,000,000 Eurodollars for 3 months at 8%. 2. Purchase FF7.715.000 at the spot bidrate. 3. Invest the francs for 3 months at the Eurofranc deposit rate of 11-5/8%. 4. Simultaneously sell francs (buy dollars) forward at the forward offer rate of 7.7625. The amount of the forward sale should equal the total amount of franc proceeds at the deposit's maturity, or FF7,939,217 |FF7.715,000 X (1 +.11625/4)). Interbank Trading Exhibit 1 Spot and Forward Exchange Rates The vast bulk of foreign exchange transactions takes place in the interbank market where banks and foreign exchange brokers determine exchange rates. Dealers try to develop a sense for where the market is going and then buy or sell currency either for their clients or for their own portfolios. After Currency Spot 1 Month 3 Months 6 Months 12 Month: dealer A decides what he wants to buy or sell, he calls foreign exchange dealers at other banks and Sterling 1.4890/00 55/52 160/156 302/289 560/523 asks for the market." He wants to know whether the dealers' rates are competitive and doesn't say whether he intends to buy or sell. Foreign exchange dealer B (being called now) must use her Deutsche mark 2.0310/20 22/18 64/54 128/105 2771228 intuition to determine what caller A wants to do before offering a quote. Many techniques are used in an effort to get the best rate. For example, if the first caller wants to buy deutsche marks, he might first ask for the market in pounds to confuse the dealer and only later ask for deutsche marks. French Franc 6.6575/625 73/86 263/296 505/590 1194/135 Aside from figuring out what the caller wants to do, dealer B must also devise a strategy that Yen 154 20/30 8/6 33/27 75/62 164/137 meets her goals. If dealer B wants to sell deutsche marks (buy dollars), she might present a bid of DM2.5235 per dollar, two points higher than other banks', which are at 2.5233. The dealer must also SDR 1.2141/43 5/3 12/8 18/11 24/12 quote an offer, and this should not be better than the market since she does not want to own deutsche marks. Convention holds that the caller can choose either rate and any amount within one minute U.S. dollars per unit of currency after the quotes. After the minute, dealer B can change her quotes. When a difference in the fourth Exhibit 2 Cross-Spot Exchange Rates decimal place can represent thousands of dollars on a big transaction, good judgment and fast thinking are vital. The parties exchange confirmation papers after a deal has been arranged over the phone. Settlement occurs on the value date as the currencies are exchanged through the banks' clearing DM FF Yen accounts. Client rates are generally determined in the retail bank draft market, while the interbank DM .3050/51 1.3169/71 rate determined in the wholesale market. The largest corporate clients get rates similar to those offered to other banks. FF 3.2779/88 4.3365/84 Sometimes banks cannot make markets among themselves. When a private deal cannot be arranged, foreign exchange brokers are used as intermediaries. Banks call brokers and tell them how Yen 75.9232/350 23.1595/618 much foreign currency they want to buy or sell and at what rate they will do the transaction. The broker then takes many requests to buy or sell and tries to find banks with complementary goals. If Quotes should be interpreted as units of the currency represented in the left-hand column per unit of currency shown in the t two banks' exchange rate terms can be matched, a trade is made. The banks only learn of each other's row. Quotes for the DMlyen and FF/yen are expressed in units per 100 yen. identities after a contract is settled. Following the contract's consummation, the broker receives a fee from each bank. Banks always prefer to make their own market since the broker's fee makes the same Exhibit 3 Eurocurrency Interest Rates transaction more expensive. Currency 1 Month 3 Months 6 Months Other Foreign Exchange Instruments 12 Months U.S. Dollar 5.6875-5.8125 5.5000-5.6250 5.5000-5.6250 5.6250-5.7500 As indicated, the foreign exchange market allows individuals and corporations to transact in the spot market for immediate delivery and in the forward market for settlements in the future. Sterling 10.0625-10.1875 9.8750-9.9375 9.6875-9.7500 9.6250-9.7500 Other foreign exchange vehicles and markets are also appearing. Although they accounted for less than 1% of total foreign exchange transaction volume in 1986, their importance is likely to grow. Deutsche mark 4.4375-4.5625 4.3125-4.4375 4.3125-4.4375 4.3125-4.4375 While forward rates are quoted by commercial banks, foreign currency futures are French Franc 7.1250-7 2500 7.1875-7.3125 7.1875-7.3125 72500-7.3750 homogeneous contracts traded in physical market places such as the International Monetary Market (IMM) in Chicago. Buyers and sellers of foreign currency futures deal through the exchanges rather Yen 5.1250-5.1875 4.7500-4.8125 4.6250-4.6875 4.6250-4.6875 than directly. Advantages of these contracts are that they are relatively small, and because of their homogeneity, are highly liquid. However, homogeneity also implies inflexibility, and there are high SDR 5.9375-6.0625 5.8125-5.9375 5.7500-5.8750 5.8125-5.9375 costs on large futures transactions. Though complicated, expensive, and relatively illiquid, foreign currency options are becoming an attractive transaction alternative. Options allow a company to hedge against foreign exchange losses, but they also provide opportunities for bold speculation in the market. Unlike futures contracts, options represent the right, but not the obligation, to buy or sell a specific amount of currency at a fixed price on or before some future date. Since the option holder can always avoid exercising the option if it is uneconomical to do so, options make possible large upside gains while limiting downside losses. Costing an average of 5-6% of the underlying contract amount options are expensive compared to the spreads on interbank forward contracts. Though options are not for everyone, more companies are using them to make a profit and hedge risk in times of volatile exchange rate fluctuations. Interbank Trading Exhibit 1 Spot and Forward Exchange Rates The vast bulk of foreign exchange transactions takes place in the interbank market where banks and foreign exchange brokers determine exchange rates. Dealers try to develop a sense for where the market is going and then buy or sell currency either for their clients or for their own portfolios. After Currency Spot 1 Month 3 Months 6 Months 12 Month: dealer A decides what he wants to buy or sell, he calls foreign exchange dealers at other banks and Sterling 1.4890/00 55/52 160/156 302/289 560/523 asks for the market." He wants to know whether the dealers' rates are competitive and doesn't say whether he intends to buy or sell. Foreign exchange dealer B (being called now) must use her Deutsche mark 2.0310/20 22/18 64/54 128/105 2771228 intuition to determine what caller A wants to do before offering a quote. Many techniques are used in an effort to get the best rate. For example, if the first caller wants to buy deutsche marks, he might first ask for the market in pounds to confuse the dealer and only later ask for deutsche marks. French Franc 6.6575/625 73/86 263/296 505/590 1194/135 Aside from figuring out what the caller wants to do, dealer B must also devise a strategy that Yen 154 20/30 8/6 33/27 75/62 164/137 meets her goals. If dealer B wants to sell deutsche marks (buy dollars), she might present a bid of DM2.5235 per dollar, two points higher than other banks', which are at 2.5233. The dealer must also SDR 1.2141/43 5/3 12/8 18/11 24/12 quote an offer, and this should not be better than the market since she does not want to own deutsche marks. Convention holds that the caller can choose either rate and any amount within one minute U.S. dollars per unit of currency after the quotes. After the minute, dealer B can change her quotes. When a difference in the fourth Exhibit 2 Cross-Spot Exchange Rates decimal place can represent thousands of dollars on a big transaction, good judgment and fast thinking are vital. The parties exchange confirmation papers after a deal has been arranged over the phone. Settlement occurs on the value date as the currencies are exchanged through the banks' clearing DM FF Yen accounts. Client rates are generally determined in the retail bank draft market, while the interbank DM .3050/51 1.3169/71 rate determined in the wholesale market. The largest corporate clients get rates similar to those offered to other banks. FF 3.2779/88 4.3365/84 Sometimes banks cannot make markets among themselves. When a private deal cannot be arranged, foreign exchange brokers are used as intermediaries. Banks call brokers and tell them how Yen 75.9232/350 23.1595/618 much foreign currency they want to buy or sell and at what rate they will do the transaction. The broker then takes many requests to buy or sell and tries to find banks with complementary goals. If Quotes should be interpreted as units of the currency represented in the left-hand column per unit of currency shown in the t two banks' exchange rate terms can be matched, a trade is made. The banks only learn of each other's row. Quotes for the DMlyen and FF/yen are expressed in units per 100 yen. identities after a contract is settled. Following the contract's consummation, the broker receives a fee from each bank. Banks always prefer to make their own market since the broker's fee makes the same Exhibit 3 Eurocurrency Interest Rates transaction more expensive. Currency 1 Month 3 Months 6 Months Other Foreign Exchange Instruments 12 Months U.S. Dollar 5.6875-5.8125 5.5000-5.6250 5.5000-5.6250 5.6250-5.7500 As indicated, the foreign exchange market allows individuals and corporations to transact in the spot market for immediate delivery and in the forward market for settlements in the future. Sterling 10.0625-10.1875 9.8750-9.9375 9.6875-9.7500 9.6250-9.7500 Other foreign exchange vehicles and markets are also appearing. Although they accounted for less than 1% of total foreign exchange transaction volume in 1986, their importance is likely to grow. Deutsche mark 4.4375-4.5625 4.3125-4.4375 4.3125-4.4375 4.3125-4.4375 While forward rates are quoted by commercial banks, foreign currency futures are French Franc 7.1250-7 2500 7.1875-7.3125 7.1875-7.3125 72500-7.3750 homogeneous contracts traded in physical market places such as the International Monetary Market (IMM) in Chicago. Buyers and sellers of foreign currency futures deal through the exchanges rather Yen 5.1250-5.1875 4.7500-4.8125 4.6250-4.6875 4.6250-4.6875 than directly. Advantages of these contracts are that they are relatively small, and because of their homogeneity, are highly liquid. However, homogeneity also implies inflexibility, and there are high SDR 5.9375-6.0625 5.8125-5.9375 5.7500-5.8750 5.8125-5.9375 costs on large futures transactions. Though complicated, expensive, and relatively illiquid, foreign currency options are becoming an attractive transaction alternative. Options allow a company to hedge against foreign exchange losses, but they also provide opportunities for bold speculation in the market. Unlike futures contracts, options represent the right, but not the obligation, to buy or sell a specific amount of currency at a fixed price on or before some future date. Since the option holder can always avoid exercising the option if it is uneconomical to do so, options make possible large upside gains while limiting downside losses. Costing an average of 5-6% of the underlying contract amount options are expensive compared to the spreads on interbank forward contracts. Though options are not for everyone, more companies are using them to make a profit and hedge risk in times of volatile exchange rate fluctuations. currency is at a dollar premium, and the trader should add the forward points to the respective spot points. Because money can flow quickly and in large volume from one Eurocurrency deposit to another, and because forward rates may be thought of as unbiased predictors of future spot rates, Eurodepositors aggressively seeking the highest effective return (including expected exchange rate movements) should drive Eurodeposit rates, spot exchange rates, and forward exchange rates into an interdependent relationship in which expected yields are identical across currencies. This condition is known as interest rate parity. It can be expressed notationally by the following equation: Forward quotes can also be presented as a percent-per-annum deviation from the spot rate. By convention, the formula for calculating forward premiums and discounts as percentages using European terms, with n equal to the number of months in the contract, is: Forward premium or discount (%p.a.) spot rate-forward rate x 12 x 100 forward rate (1 + Rp) (1 + R) Using spot and three-month forward quotes for deutsche marks of 2.2605 and 2.2406, respectively, we would have: F-S 2.2605-2.2406 x 12 x 100 = 3.55% 2.2406 3 where, When using American terms, the formula changes as follows: F = the forward exchange rate expressed as units of foreign currency per dollar (European terms); n S = the spot exchange rate expressed as units of foreign currency per dollar; Rs and Rp = the Eurodollar deposit rate and the other Eurocurrency deposit rate, respectively. Forward premium or discount (%p.a.) forward rate-spotx 12 x 100 spot Thus, in the above example we would have: 4463..4424 x 12 x 100 - 3.53% .4424 3 This differs from the percentage using European terms only by a rounding error. If this condition is violated, a covered interest arbitrage opportunity will present itself (for this reason, the above equation is also frequently referred to as the covered interest arbitrage" condition) For example, consider the terms presented in Table 1. Covered Interest Arbitrage Table 1 Spot 3-Month Forward 7.7150/200 300/425 --- French Franc 3 Mo. Eurofranc Deposit Rate 3 Mo. Eurodollar Deposit Rate 11 5/8 - 11 3/4% 7 7/8-8% The French franc is selling at a forward discount against the dollar. Using the midpoints of the quotes, the discount is 1.88% on an annualized basis. This is smaller in absolute terms than is theoretically justified on the basis of differences in interest rates: 3.68% = {[(1+11.6875/400)/(1+7.9375/400))-1}x4x100 Consequently, an arbitrageur could profit risklessly by taking the following steps: Many factors explain the changing values of foreign currencies relative to the U.S. dollar. Spot rates can be quite volatile, influenced by news, rumors, speculation, supply and demand imbalances, and central bank intervention. Over the long run, spot rates are affected by relative interest rates and inflation rates, trade imbalances, and purchases or sales of foreign assets. Perhaps the dominant factor influencing the forward rate of a currency relative to its spot rate is the difference between nominal interest rates on foreign currency-denominated investments and comparable U.S. dollar investments. Investors will compare interest rates around the world in pursuit of the best possible return for a given level of risk. Large banks and corporations seeking short-term use of cash will generally look at Eurodeposit rates since such deposits are quite accessible, secure, and competitively priced because of the less-regulated nature of the Eurodeposit market. However, the highest nominal Eurodeposit rate does not necessarily imply the highest expected yield in home currency terms. If the currency in which the deposit is made depreciates against the home currency, then the actual yield on the deposit in home currency terms will be less than the quoted nominal yield. For example, a one-year Eurofranc deposit may offer a yield of 11 5/8% compared to a one-year Eurodollar deposit offering 7 7/8%. But if the franc depreciates by 3.36% or more, the interest rate difference favoring the franc will have been completely offset from a U.S. dollar perspective. The depositor could hedge this risk by selling francs (purchasing dollars) forward at the prevailing market exchange rate, thus locking in the future rate at which the principal plus interest can be converted to dollars. In principle, assuming an efficiently operating foreign exchange market, the prevailing one-year forward contract rate for French francs will reflect the market's collective judgment about what the spot rate will be one year later. In other words, the current forward rate should be an unbiased predictor of the future spot rate, a condition known as forward parity. In three months, the arbitrageur would receive the Eurofranc deposit with interest, execute the forward contract, and obtain $1,022,765 [FF7,939,217/7.7625]. This could be used to repay the Eurodollar loan with interest amounting to $1,020,000 [$1,000,000 X (1 + 08/4)], leaving a gain of $2,765. Assuming total transaction, brokerage, and cable cost of 0.25%, or $250 on the $1,000,000 deal, a net profit remains of $2,515. Note that this was obtained risklessly and without any equity directly committed by the arbitrageur. As many people try to exploit this opportunity in volume, interest rates and exchange rates will adjust until parity is restored and riskless profit opportunities are 1. Borrow 1,000,000 Eurodollars for 3 months at 8%. 2. Purchase FF7.715.000 at the spot bidrate. 3. Invest the francs for 3 months at the Eurofranc deposit rate of 11-5/8%. 4. Simultaneously sell francs (buy dollars) forward at the forward offer rate of 7.7625. The amount of the forward sale should equal the total amount of franc proceeds at the deposit's maturity, or FF7,939,217 |FF7.715,000 X (1 +.11625/4)). Interbank Trading Exhibit 1 Spot and Forward Exchange Rates The vast bulk of foreign exchange transactions takes place in the interbank market where banks and foreign exchange brokers determine exchange rates. Dealers try to develop a sense for where the market is going and then buy or sell currency either for their clients or for their own portfolios. After Currency Spot 1 Month 3 Months 6 Months 12 Month: dealer A decides what he wants to buy or sell, he calls foreign exchange dealers at other banks and Sterling 1.4890/00 55/52 160/156 302/289 560/523 asks for the market." He wants to know whether the dealers' rates are competitive and doesn't say whether he intends to buy or sell. Foreign exchange dealer B (being called now) must use her Deutsche mark 2.0310/20 22/18 64/54 128/105 2771228 intuition to determine what caller A wants to do before offering a quote. Many techniques are used in an effort to get the best rate. For example, if the first caller wants to buy deutsche marks, he might first ask for the market in pounds to confuse the dealer and only later ask for deutsche marks. French Franc 6.6575/625 73/86 263/296 505/590 1194/135 Aside from figuring out what the caller wants to do, dealer B must also devise a strategy that Yen 154 20/30 8/6 33/27 75/62 164/137 meets her goals. If dealer B wants to sell deutsche marks (buy dollars), she might present a bid of DM2.5235 per dollar, two points higher than other banks', which are at 2.5233. The dealer must also SDR 1.2141/43 5/3 12/8 18/11 24/12 quote an offer, and this should not be better than the market since she does not want to own deutsche marks. Convention holds that the caller can choose either rate and any amount within one minute U.S. dollars per unit of currency after the quotes. After the minute, dealer B can change her quotes. When a difference in the fourth Exhibit 2 Cross-Spot Exchange Rates decimal place can represent thousands of dollars on a big transaction, good judgment and fast thinking are vital. The parties exchange confirmation papers after a deal has been arranged over the phone. Settlement occurs on the value date as the currencies are exchanged through the banks' clearing DM FF Yen accounts. Client rates are generally determined in the retail bank draft market, while the interbank DM .3050/51 1.3169/71 rate determined in the wholesale market. The largest corporate clients get rates similar to those offered to other banks. FF 3.2779/88 4.3365/84 Sometimes banks cannot make markets among themselves. When a private deal cannot be arranged, foreign exchange brokers are used as intermediaries. Banks call brokers and tell them how Yen 75.9232/350 23.1595/618 much foreign currency they want to buy or sell and at what rate they will do the transaction. The broker then takes many requests to buy or sell and tries to find banks with complementary goals. If Quotes should be interpreted as units of the currency represented in the left-hand column per unit of currency shown in the t two banks' exchange rate terms can be matched, a trade is made. The banks only learn of each other's row. Quotes for the DMlyen and FF/yen are expressed in units per 100 yen. identities after a contract is settled. Following the contract's consummation, the broker receives a fee from each bank. Banks always prefer to make their own market since the broker's fee makes the same Exhibit 3 Eurocurrency Interest Rates transaction more expensive. Currency 1 Month 3 Months 6 Months Other Foreign Exchange Instruments 12 Months U.S. Dollar 5.6875-5.8125 5.5000-5.6250 5.5000-5.6250 5.6250-5.7500 As indicated, the foreign exchange market allows individuals and corporations to transact in the spot market for immediate delivery and in the forward market for settlements in the future. Sterling 10.0625-10.1875 9.8750-9.9375 9.6875-9.7500 9.6250-9.7500 Other foreign exchange vehicles and markets are also appearing. Although they accounted for less than 1% of total foreign exchange transaction volume in 1986, their importance is likely to grow. Deutsche mark 4.4375-4.5625 4.3125-4.4375 4.3125-4.4375 4.3125-4.4375 While forward rates are quoted by commercial banks, foreign currency futures are French Franc 7.1250-7 2500 7.1875-7.3125 7.1875-7.3125 72500-7.3750 homogeneous contracts traded in physical market places such as the International Monetary Market (IMM) in Chicago. Buyers and sellers of foreign currency futures deal through the exchanges rather Yen 5.1250-5.1875 4.7500-4.8125 4.6250-4.6875 4.6250-4.6875 than directly. Advantages of these contracts are that they are relatively small, and because of their homogeneity, are highly liquid. However, homogeneity also implies inflexibility, and there are high SDR 5.9375-6.0625 5.8125-5.9375 5.7500-5.8750 5.8125-5.9375 costs on large futures transactions. Though complicated, expensive, and relatively illiquid, foreign currency options are becoming an attractive transaction alternative. Options allow a company to hedge against foreign exchange losses, but they also provide opportunities for bold speculation in the market. Unlike futures contracts, options represent the right, but not the obligation, to buy or sell a specific amount of currency at a fixed price on or before some future date. Since the option holder can always avoid exercising the option if it is uneconomical to do so, options make possible large upside gains while limiting downside losses. Costing an average of 5-6% of the underlying contract amount options are expensive compared to the spreads on interbank forward contracts. Though options are not for everyone, more companies are using them to make a profit and hedge risk in times of volatile exchange rate fluctuations. Interbank Trading Exhibit 1 Spot and Forward Exchange Rates The vast bulk of foreign exchange transactions takes place in the interbank market where banks and foreign exchange brokers determine exchange rates. Dealers try to develop a sense for where the market is going and then buy or sell currency either for their clients or for their own portfolios. After Currency Spot 1 Month 3 Months 6 Months 12 Month: dealer A decides what he wants to buy or sell, he calls foreign exchange dealers at other banks and Sterling 1.4890/00 55/52 160/156 302/289 560/523 asks for the market." He wants to know whether the dealers' rates are competitive and doesn't say whether he intends to buy or sell. Foreign exchange dealer B (being called now) must use her Deutsche mark 2.0310/20 22/18 64/54 128/105 2771228 intuition to determine what caller A wants to do before offering a quote. Many techniques are used in an effort to get the best rate. For example, if the first caller wants to buy deutsche marks, he might first ask for the market in pounds to confuse the dealer and only later ask for deutsche marks. French Franc 6.6575/625 73/86 263/296 505/590 1194/135 Aside from figuring out what the caller wants to do, dealer B must also devise a strategy that Yen 154 20/30 8/6 33/27 75/62 164/137 meets her goals. If dealer B wants to sell deutsche marks (buy dollars), she might present a bid of DM2.5235 per dollar, two points higher than other banks', which are at 2.5233. The dealer must also SDR 1.2141/43 5/3 12/8 18/11 24/12 quote an offer, and this should not be better than the market since she does not want to own deutsche marks. Convention holds that the caller can choose either rate and any amount within one minute U.S. dollars per unit of currency after the quotes. After the minute, dealer B can change her quotes. When a difference in the fourth Exhibit 2 Cross-Spot Exchange Rates decimal place can represent thousands of dollars on a big transaction, good judgment and fast thinking are vital. The parties exchange confirmation papers after a deal has been arranged over the phone. Settlement occurs on the value date as the currencies are exchanged through the banks' clearing DM FF Yen accounts. Client rates are generally determined in the retail bank draft market, while the interbank DM .3050/51 1.3169/71 rate determined in the wholesale market. The largest corporate clients get rates similar to those offered to other banks. FF 3.2779/88 4.3365/84 Sometimes banks cannot make markets among themselves. When a private deal cannot be arranged, foreign exchange brokers are used as intermediaries. Banks call brokers and tell them how Yen 75.9232/350 23.1595/618 much foreign currency they want to buy or sell and at what rate they will do the transaction. The broker then takes many requests to buy or sell and tries to find banks with complementary goals. If Quotes should be interpreted as units of the currency represented in the left-hand column per unit of currency shown in the t two banks' exchange rate terms can be matched, a trade is made. The banks only learn of each other's row. Quotes for the DMlyen and FF/yen are expressed in units per 100 yen. identities after a contract is settled. Following the contract's consummation, the broker receives a fee from each bank. Banks always prefer to make their own market since the broker's fee makes the same Exhibit 3 Eurocurrency Interest Rates transaction more expensive. Currency 1 Month 3 Months 6 Months Other Foreign Exchange Instruments 12 Months U.S. Dollar 5.6875-5.8125 5.5000-5.6250 5.5000-5.6250 5.6250-5.7500 As indicated, the foreign exchange market allows individuals and corporations to transact in the spot market for immediate delivery and in the forward market for settlements in the future. Sterling 10.0625-10.1875 9.8750-9.9375 9.6875-9.7500 9.6250-9.7500 Other foreign exchange vehicles and markets are also appearing. Although they accounted for less than 1% of total foreign exchange transaction volume in 1986, their importance is likely to grow. Deutsche mark 4.4375-4.5625 4.3125-4.4375 4.3125-4.4375 4.3125-4.4375 While forward rates are quoted by commercial banks, foreign currency futures are French Franc 7.1250-7 2500 7.1875-7.3125 7.1875-7.3125 72500-7.3750 homogeneous contracts traded in physical market places such as the International Monetary Market (IMM) in Chicago. Buyers and sellers of foreign currency futures deal through the exchanges rather Yen 5.1250-5.1875 4.7500-4.8125 4.6250-4.6875 4.6250-4.6875 than directly. Advantages of these contracts are that they are relatively small, and because of their homogeneity, are highly liquid. However, homogeneity also implies inflexibility, and there are high SDR 5.9375-6.0625 5.8125-5.9375 5.7500-5.8750 5.8125-5.9375 costs on large futures transactions. Though complicated, expensive, and relatively illiquid, foreign currency options are becoming an attractive transaction alternative. Options allow a company to hedge against foreign exchange losses, but they also provide opportunities for bold speculation in the market. Unlike futures contracts, options represent the right, but not the obligation, to buy or sell a specific amount of currency at a fixed price on or before some future date. Since the option holder can always avoid exercising the option if it is uneconomical to do so, options make possible large upside gains while limiting downside losses. Costing an average of 5-6% of the underlying contract amount options are expensive compared to the spreads on interbank forward contracts. Though options are not for everyone, more companies are using them to make a profit and hedge risk in times of volatile exchange rate fluctuations

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts