Answered step by step

Verified Expert Solution

Question

1 Approved Answer

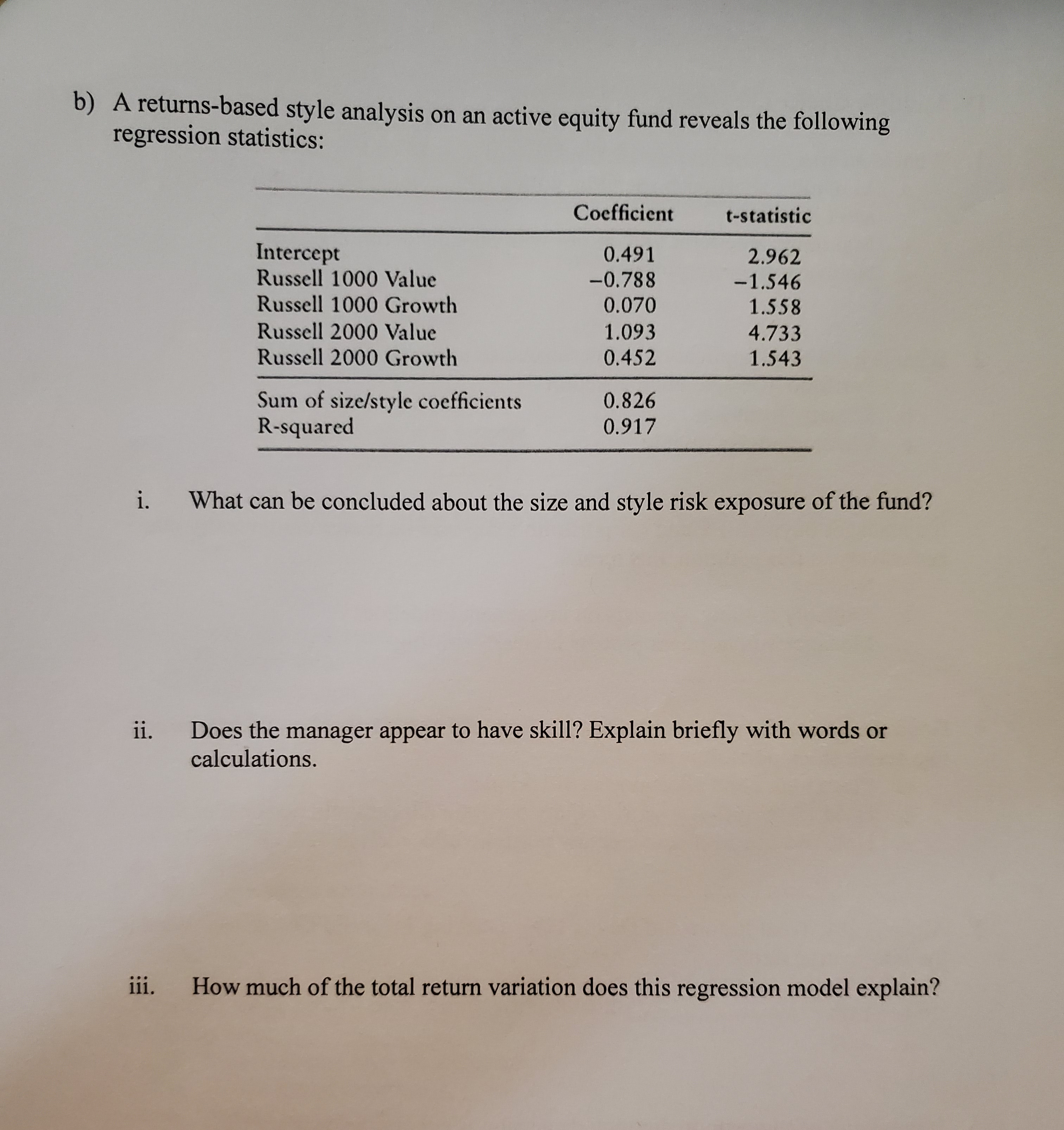

b) A returns-based style analysis on an active equity fund reveals the following regression statistics: Coefficient t-statistic Intercept 0.491 2.962 Russell 1000 Value -0.788

b) A returns-based style analysis on an active equity fund reveals the following regression statistics: Coefficient t-statistic Intercept 0.491 2.962 Russell 1000 Value -0.788 -1.546 Russell 1000 Growth 0.070 1.558 Russell 2000 Value 1.093 4.733 Russell 2000 Growth 0.452 1.543 Sum of size/style coefficients 0.826 R-squared 0.917 i. What can be concluded about the size and style risk exposure of the fund? ii. Does the manager appear to have skill? Explain briefly with words or calculations. iii. How much of the total return variation does this regression model explain?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance Applications and Theory

Authors: Marcia Cornett, Troy Adair

3rd edition

1259252221, 007786168X, 9781259252228, 978-0077861681