Answered step by step

Verified Expert Solution

Question

1 Approved Answer

b. Consider the following information about three stocks: From the information given, you are required to answer the following questions. i. Compute the Standard Deviation

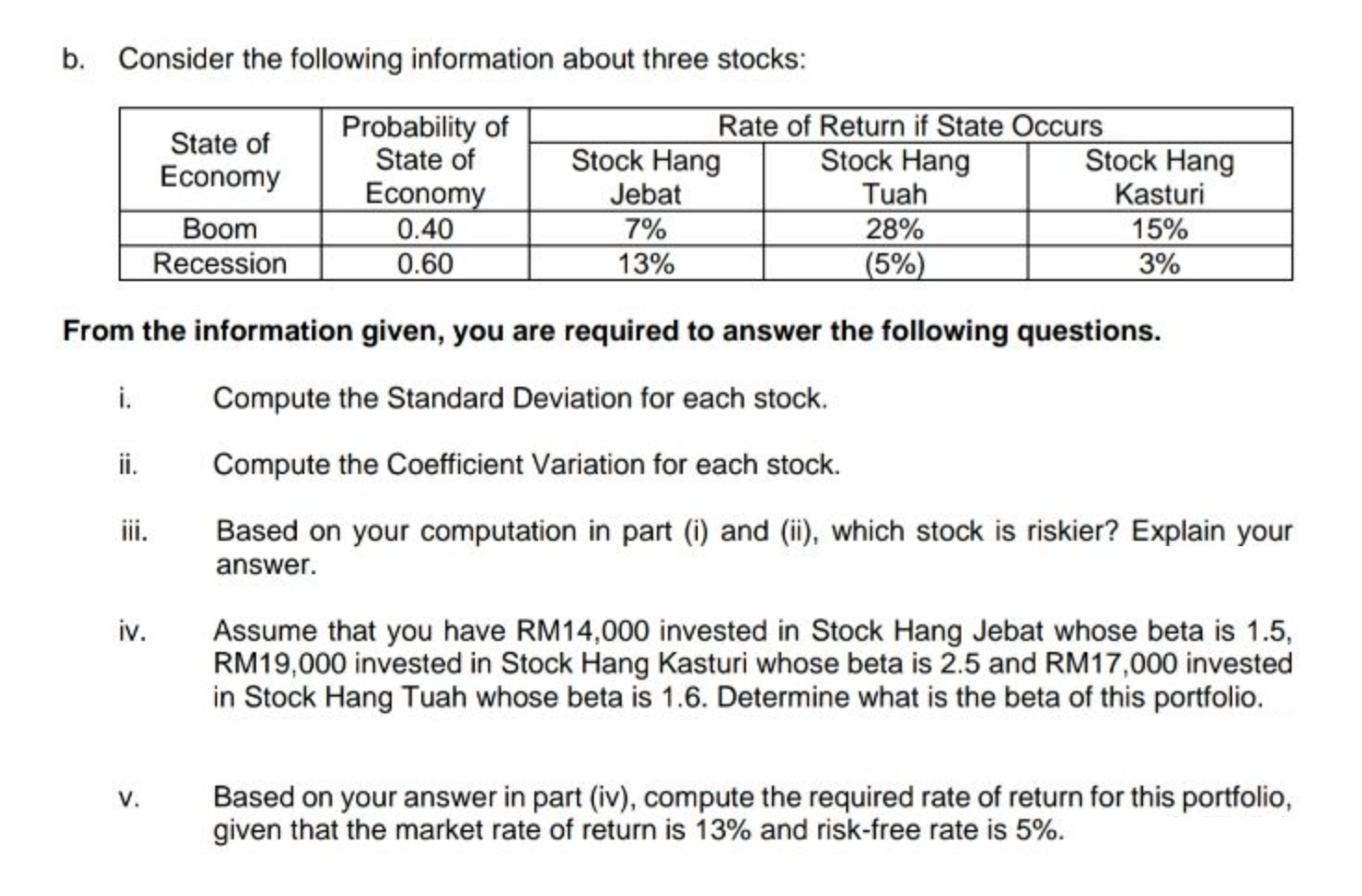

b. Consider the following information about three stocks: From the information given, you are required to answer the following questions. i. Compute the Standard Deviation for each stock. ii. Compute the Coefficient Variation for each stock. iii. Based on your computation in part (i) and (ii), which stock is riskier? Explain your answer. iv. Assume that you have RM14,000 invested in Stock Hang Jebat whose beta is 1.5, RM19,000 invested in Stock Hang Kasturi whose beta is 2.5 and RM17,000 invested in Stock Hang Tuah whose beta is 1.6. Determine what is the beta of this portfolio. v. Based on your answer in part (iv), compute the required rate of return for this portfolio, given that the market rate of return is 13% and risk-free rate is 5%

b. Consider the following information about three stocks: From the information given, you are required to answer the following questions. i. Compute the Standard Deviation for each stock. ii. Compute the Coefficient Variation for each stock. iii. Based on your computation in part (i) and (ii), which stock is riskier? Explain your answer. iv. Assume that you have RM14,000 invested in Stock Hang Jebat whose beta is 1.5, RM19,000 invested in Stock Hang Kasturi whose beta is 2.5 and RM17,000 invested in Stock Hang Tuah whose beta is 1.6. Determine what is the beta of this portfolio. v. Based on your answer in part (iv), compute the required rate of return for this portfolio, given that the market rate of return is 13% and risk-free rate is 5% Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Developments In Entrepreneurial Finance And Technology

Authors: David B. Audretsch, Maksim Belitski, Nada Rejeb, Rosa Caiazza

1st Edition

1800884338,1800884346