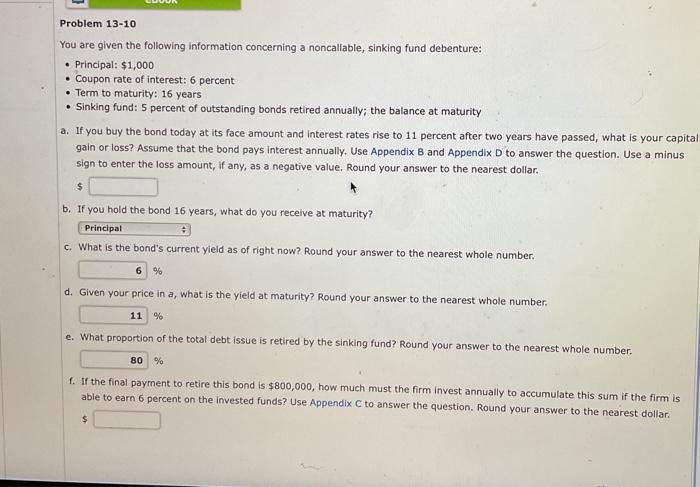

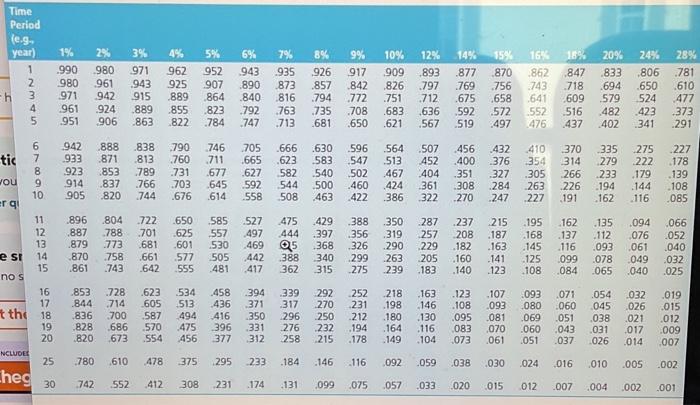

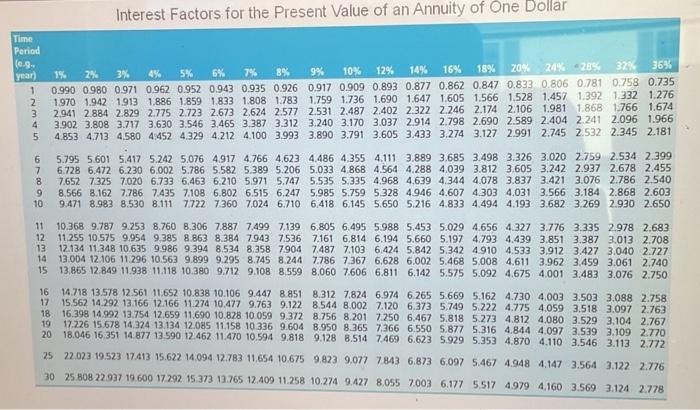

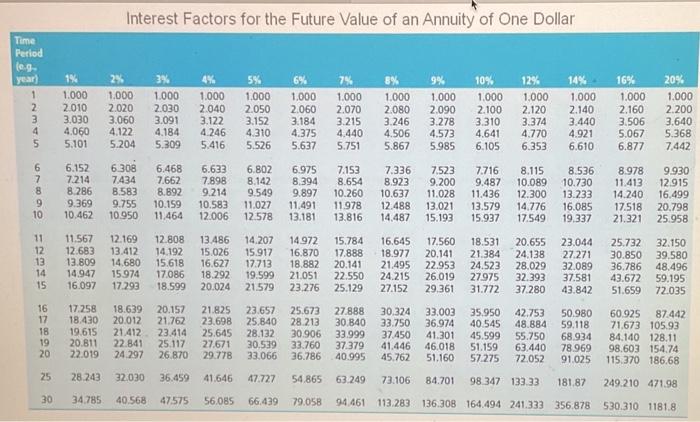

You are given the following information concerning a noncallable, sinking fund debenture: - Principal: $1,000 - Coupon rate of interest: 6 percent - Term to maturity: 16 years - Sinking fund: 5 percent of outstanding bonds retired annually; the balance at maturity a. If you buy the bond today at its face amount and interest rates rise to 11 percent after two years have passed, what is your capita gain or loss? Assume that the bond pays interest annually. Use Appendix B and Appendix D to answer the question. Use a minus sign to enter the loss amount, if any, as a negative value, Round your answer to the nearest dollar. b. If you hold the bond 16 years, what do you recelve at maturity? c. What is the bond's current yield as of right now? Round your answer to the nearest whole number. % d. Given your price in a, what is the yield at maturity? Round your answer to the nearest whole number. % e. What proportion of the total debt issue is retired by the sinking fund? Round your answer to the nearest whole number. % 1. If the final payment to retire this bond is $800,000, how much must the firm invest annually to accumulate this sum if the firm is able to earn 6 percent on the invested funds? Use Appendix C to answer the question. Round your answer to the nearest dollar. $ \begin{tabular}{|c|c|c|c|c|c|c|c|c|c|c|c|c|c|c|c|c|c|c|} \hline \begin{tabular}{l} Time \\ Period \\ (eg. \\ year) \end{tabular} & 1% & 2% & 3% & 4% & 5% & 6% & 7% & 8% & 9% & 10% & 12% & 14% & 15% & & & 20% & 24% & \\ \hline \begin{tabular}{l} 1 \\ 2 \\ 3 \\ 4 \\ 5 \end{tabular} & \begin{tabular}{l} 990 \\ 980 \\ 971 \\ 961 \\ .951 \end{tabular} & \begin{tabular}{l} 980 \\ 961 \\ 942 \\ .924 \\ 906 \end{tabular} & \begin{tabular}{l} 971 \\ .943 \\ 915 \\ .889 \\ .863 \end{tabular} & \begin{tabular}{l} 962 \\ 925 \\ .889 \\ .855 \\ 822 \end{tabular} & \begin{tabular}{l} 952 \\ 907 \\ .864 \\ 823 \\ .784 \end{tabular} & \begin{tabular}{l} .943 \\ .890 \\ .840 \\ .792 \\ .747 \end{tabular} & \begin{tabular}{l} 935 \\ .873 \\ 816 \\ .763 \\ .713 \end{tabular} & \begin{tabular}{l} .926 \\ .857 \\ .794 \\ .735 \\ .681 \end{tabular} & \begin{tabular}{l} 917 \\ .842 \\ .772 \\ .708 \\ .650 \end{tabular} & \begin{tabular}{l} .909 \\ .826 \\ .751 \\ .683 \\ .621 \end{tabular} & \begin{tabular}{l} .893 \\ .797 \\ .712 \\ .636 \\ .567 \end{tabular} & \begin{tabular}{l} .877 \\ .769 \\ .675 \\ .592 \\ .519 \end{tabular} & \begin{tabular}{l} .870 \\ .756 \\ .658 \\ .572 \\ .497 \end{tabular} & \begin{tabular}{l} .862 \\ .743 \\ .641 \\ .552 \\ .476 \end{tabular} & \begin{tabular}{l} .847 \\ .718 \\ 609 \\ .516 \\ .437 \end{tabular} & \begin{tabular}{l} .833 \\ .694 \\ .579 \\ .482 \\ .402 \end{tabular} & \begin{tabular}{l} .806 \\ .650 \\ 524 \\ .423 \\ .341 \end{tabular} & \begin{tabular}{l} .781 \\ .610 \\ .477 \\ .373 \\ .291 \end{tabular} \\ \hline \begin{tabular}{c} 6 \\ 7 \\ 8 \\ 9 \\ 10 \end{tabular} & \begin{tabular}{l} 942 \\ 933 \\ 923 \\ 914 \\ 905 \end{tabular} & \begin{tabular}{l} 888 \\ .871 \\ 853 \\ .837 \\ 820 \end{tabular} & \begin{tabular}{l} .838 \\ .813 \\ .789 \\ .766 \\ .744 \end{tabular} & \begin{tabular}{l} .790 \\ .760 \\ .731 \\ .703 \\ .676 \end{tabular} & \begin{tabular}{l} .746 \\ .711 \\ .677 \\ .645 \\ .614 \end{tabular} & \begin{tabular}{l} .705 \\ .665 \\ .627 \\ .592 \\ .558 \end{tabular} & \begin{tabular}{l} .666 \\ .623 \\ 582 \\ .544 \\ .508 \end{tabular} & \begin{tabular}{l} .500 \\ .463 \end{tabular} & \begin{tabular}{l} .460 \\ .422 \end{tabular} & \begin{tabular}{l} .564 \\ .513 \\ .467 \\ .424 \\ .386 \end{tabular} & \begin{tabular}{l} .507 \\ 452 \\ 404 \\ .361 \\ .322 \end{tabular} & \begin{tabular}{l} .351 \\ .308 \\ .270 \end{tabular} & \begin{tabular}{l} .432 \\ .376 \\ .327 \\ .284 \\ .247 \end{tabular} & \begin{tabular}{l} .305 \\ .263 \\ .227 \end{tabular} & \begin{tabular}{l} 370 \\ 314 \\ 266 \\ .226 \\ .191 \end{tabular} & \begin{tabular}{l} .335 \\ .279 \\ .233 \\ .194 \\ .162 \end{tabular} & \begin{tabular}{l} .275 \\ .222 \\ .179 \\ .144 \\ .116 \end{tabular} & \begin{tabular}{l} .227 \\ .178 \\ .139 \\ .108 \\ .085 \end{tabular} \\ \hline \begin{tabular}{l} 14 \\ 15 \end{tabular} & \begin{tabular}{l} .896 \\ .887 \\ .879 \\ .870 \\ .861 \end{tabular} & \begin{tabular}{l} .804 \\ .788 \\ .773 \\ .758 \\ .743 \end{tabular} & \begin{tabular}{l} .722 \\ .701 \\ .681 \\ .661 \\ .642 \end{tabular} & \begin{tabular}{l} .650 \\ .625 \\ .601 \\ .577 \\ .555 \end{tabular} & \begin{tabular}{l} 585 \\ 557 \\ 530 \\ 505 \\ .481 \end{tabular} & \begin{tabular}{l} .527 \\ .497 \\ 469 \\ .442 \\ .417 \end{tabular} & \begin{tabular}{l} .475 \\ 444 \\ 95 \\ .388 \\ 362 \end{tabular} & \begin{tabular}{l} .429 \\ .397 \\ .368 \\ 340 \\ 315 \end{tabular} & \begin{tabular}{l} .356 \\ .326 \\ .299 \\ .275 \end{tabular} & \begin{tabular}{l} .350 \\ .319 \\ .290 \\ .263 \\ .239 \end{tabular} & \begin{tabular}{l} .287 \\ .257 \\ .229 \\ .205 \\ .183 \end{tabular} & \begin{tabular}{l} .237 \\ .208 \\ .182 \\ .160 \\ .140 \end{tabular} & \begin{tabular}{l} .215 \\ .187 \\ .163 \\ .141 \\ .123 \end{tabular} & \begin{tabular}{l} .195 \\ .168 \\ .145 \\ .125 \\ .108 \end{tabular} & \begin{tabular}{l} .137 \\ .116 \\ .099 \\ .084 \end{tabular} & \begin{tabular}{l} .135 \\ .112 \\ .093 \\ .078 \\ .065 \end{tabular} & \begin{tabular}{l} .094 \\ .076 \\ .061 \\ .049 \\ .040 \end{tabular} & \begin{tabular}{l} .066 \\ .052 \\ .040 \\ .032 \\ .025 \end{tabular} \\ \hline \begin{tabular}{l} 16 \\ 17 \\ 18 \\ 19 \\ 20 \end{tabular} & \begin{tabular}{l} 853 \\ .844 \\ 836 \\ 828 \\ .820 \end{tabular} & \begin{tabular}{l} 728 \\ .714 \\ .700 \\ .686 \\ .673 \end{tabular} & \begin{tabular}{l} .623 \\ .605 \\ .587 \\ .570 \\ .554 \end{tabular} & \begin{tabular}{l} .534 \\ 513 \\ .494 \\ .475 \\ .456 \end{tabular} & \begin{tabular}{l} .458 \\ .436 \\ .416 \\ .396 \\ 377 \end{tabular} & \begin{tabular}{l} .394 \\ .371 \\ .350 \\ .331 \\ .312 \end{tabular} & \begin{tabular}{l} 339 \\ .317 \\ 296 \\ 276 \\ 258 \end{tabular} & \begin{tabular}{l} 292 \\ 270 \\ .250 \\ .232 \\ .215 \end{tabular} & \begin{tabular}{l} .252 \\ .231 \\ .212 \\ .194 \\ .178 \end{tabular} & \begin{tabular}{l} .218 \\ .198 \\ .180 \\ .164 \\ .149 \end{tabular} & \begin{tabular}{l} .163 \\ .146 \\ .130 \\ .116 \\ .104 \end{tabular} & \begin{tabular}{l} .123 \\ .108 \\ .095 \\ .083 \\ .073 \end{tabular} & \begin{tabular}{l} .107 \\ .093 \\ .081 \\ .070 \\ .061 \end{tabular} & \begin{tabular}{l} .093 \\ .080 \\ .069 \\ .060 \\ .051 \end{tabular} & \begin{tabular}{l} .071 \\ .060 \\ .051 \\ .043 \\ .037 \end{tabular} & \begin{tabular}{l} .054 \\ .045 \\ .038 \\ .031 \\ .026 \end{tabular} & \begin{tabular}{l} .032 \\ .026 \\ .021 \\ .017 \\ .014 \end{tabular} & \begin{tabular}{l} .019 \\ .015 \\ .012 \\ .009 \\ .007 \end{tabular} \\ \hline 25 & 780 & .610 & .478 & 375 & 295 & 233 & .184 & .146 & .116 & 092 & .059 & .038 & .030 & .024 & .016 & .010 & .005 & .002 \\ \hline 30 & 742 & .552 & .412 & 308 & .231 & .174 & .13 & .099 & .075 & .057 & .033 & .020 & .015 & 012 & .007 & .004 & .002 & .001 \\ \hline \end{tabular} Interest Factors for the Future Value of an Annuitv of One Dolla