Answered step by step

Verified Expert Solution

Question

1 Approved Answer

b) is not 0.3 Consider the following information regarding the performance of a money manager in a recent month. The table represents the actual return

b) is not 0.3

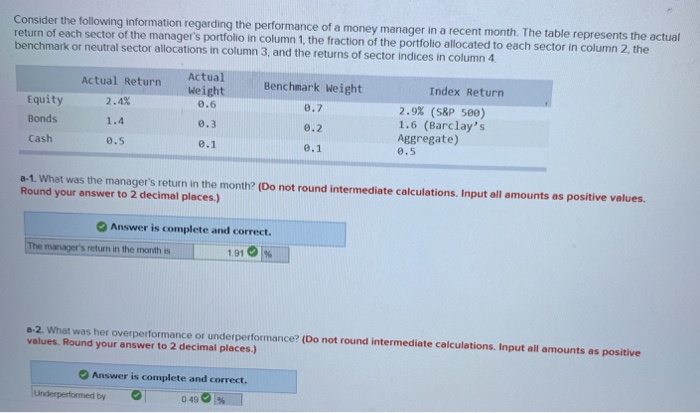

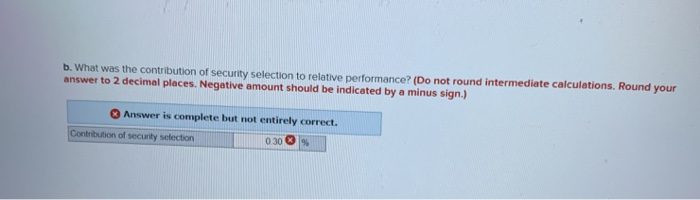

Consider the following information regarding the performance of a money manager in a recent month. The table represents the actual return of each sector of the manager's portfolio in column 1, the fraction of the portfolio allocated to each sector in column 2 the benchmark or neutral sector allocations in column 3, and the returns of sector indices in column 4. Actual Return Actual Weight 0.6 Benchmark Weight 0.7 Equity Bonds 2.4% 1.4 0.3 Index Return 2.9% (S&P 500) 1.6 (Barclay's Aggregate) 0.5 0.2 Cash 0.5 0.1 0.1 a-1. What was the manager's return in the month? (Do not round intermediate calculations. Input all amounts as positive values. Round your answer to 2 decimal places.) Answer is complete and correct. The manager's return in the month is 1.91 -2. What was her overperformance or underperformance? (Do not round intermediate calculations. Input all amounts as positive values. Round your answer to 2 decimal places.) Answer is complete and correct. Underperformed by 049 b. What was the contribution of security selection to relative performance? (Do not round intermediate calculations. Round your answer to 2 decimal places. Negative amount should be indicated by a minus sign.) Answer is complete but not entirely correct. Contribution of security selection 030 9 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Re Imagining Offshore Finance

Authors: Christopher M. Bruner

1st Edition

0190466871, 978-0190466879