Answered step by step

Verified Expert Solution

Question

1 Approved Answer

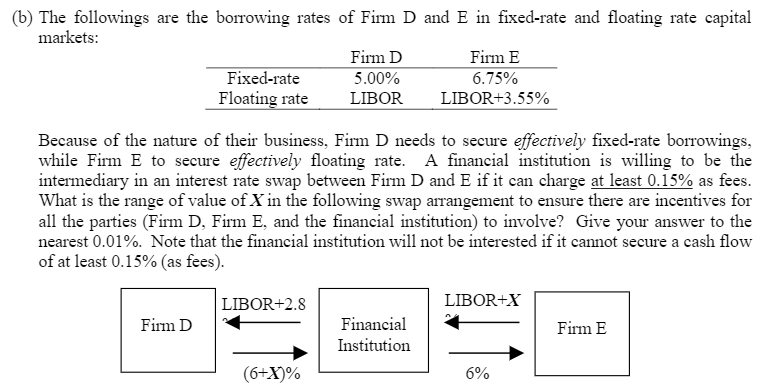

(b) The followings are the borrowing rates of Firm D and E in fixed-rate and floating rate capital markets: Firm D Firm E Fixed-rate 5.00%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Economics Business And Islamic Finance In ASEAN Economics Community

Authors: Patricia Ordoñez De Pablos Mohammad Nabil Almunawar , Muhamad Abduh

1st Edition

1799822575,1799822605