Answered step by step

Verified Expert Solution

Question

1 Approved Answer

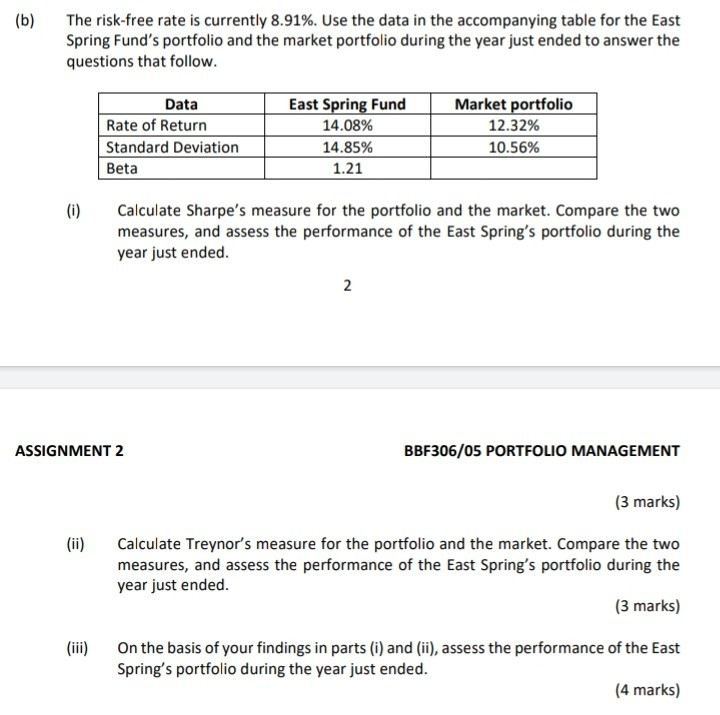

(b) The risk-free rate is currently 8.91%. Use the data in the accompanying table for the East Spring Fund's portfolio and the market portfolio during

(b) The risk-free rate is currently 8.91%. Use the data in the accompanying table for the East Spring Fund's portfolio and the market portfolio during the year just ended to answer the questions that follow. Data Rate of Return Standard Deviation Beta East Spring Fund 14.08% 14.85% 1.21 Market portfolio 12.32% 10.56% Calculate Sharpe's measure for the portfolio and the market. Compare the two measures, and assess the performance of the East Spring's portfolio during the year just ended. ASSIGNMENT 2 BBF306/05 PORTFOLIO MANAGEMENT (3 marks) (ii) Calculate Treynor's measure for the portfolio and the market. Compare the two measures, and assess the performance of the East Spring's portfolio during the year just ended. (3 marks) On the basis of your findings in parts (i) and (ii), assess the performance of the East Spring's portfolio during the year just ended. (4 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Truth About Buying Annuities Annuities Can Make Or Break Your Retirement

Authors: Steve Weisman

1st Edition

0132353083,0132701162