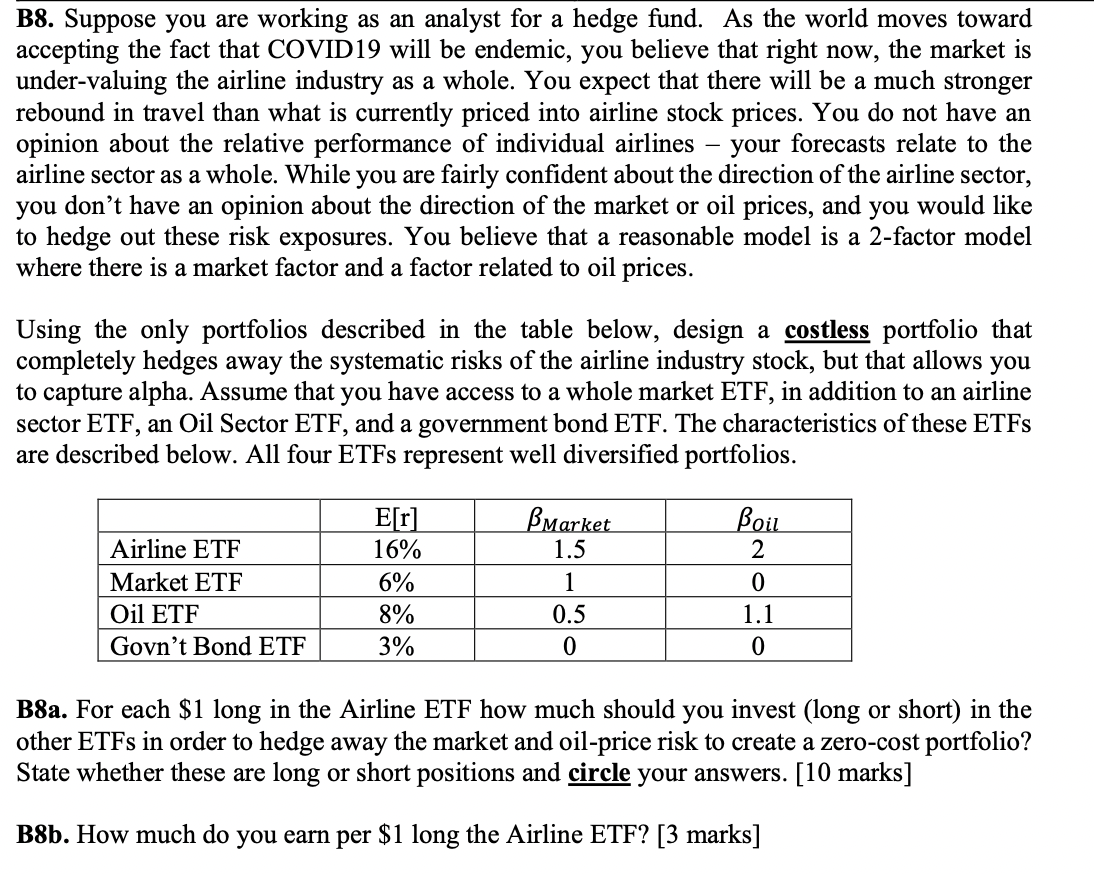

B8. Suppose you are working as an analyst for a hedge fund. As the world moves toward accepting the fact that COVID19 will be endemic, you believe that right now, the market is under-valuing the airline industry as a whole. You expect that there will be a much stronger rebound in travel than what is currently priced into airline stock prices. You do not have an opinion about the relative performance of individual airlines your forecasts relate to the airline sector as a whole. While you are fairly confident about the direction of the airline sector, you don't have an opinion about the direction of the market or oil prices, and you would like to hedge out these risk exposures. You believe that a reasonable model is a 2-factor model where there is a market factor and a factor related to oil prices. Using the only portfolios described in the table below, design a costless portfolio that completely hedges away the systematic risks of the airline industry stock, but that allows you to capture alpha. Assume that you have access to a whole market ETF, in addition to an airline sector ETF, an Oil Sector ETF, and a government bond ETF. The characteristics of these ETFs are described below. All four ETFs represent well diversified portfolios. E[r] BMarket Boil Airline ETF 16% 1.5 2 Market ETF 6% 1 0 Oil ETF 8% 0.5 1.1 Govn't Bond ETF 3% 0 0 B8a. For each $1 long in the Airline ETF how much should you invest (long or short) in the other ETFs in order to hedge away the market and oil-price risk to create a zero-cost portfolio? State whether these are long or short positions and circle your answers. [10 marks] B8b. How much do you earn per $1 long the Airline ETF? [3 marks] B8. Suppose you are working as an analyst for a hedge fund. As the world moves toward accepting the fact that COVID19 will be endemic, you believe that right now, the market is under-valuing the airline industry as a whole. You expect that there will be a much stronger rebound in travel than what is currently priced into airline stock prices. You do not have an opinion about the relative performance of individual airlines your forecasts relate to the airline sector as a whole. While you are fairly confident about the direction of the airline sector, you don't have an opinion about the direction of the market or oil prices, and you would like to hedge out these risk exposures. You believe that a reasonable model is a 2-factor model where there is a market factor and a factor related to oil prices. Using the only portfolios described in the table below, design a costless portfolio that completely hedges away the systematic risks of the airline industry stock, but that allows you to capture alpha. Assume that you have access to a whole market ETF, in addition to an airline sector ETF, an Oil Sector ETF, and a government bond ETF. The characteristics of these ETFs are described below. All four ETFs represent well diversified portfolios. E[r] BMarket Boil Airline ETF 16% 1.5 2 Market ETF 6% 1 0 Oil ETF 8% 0.5 1.1 Govn't Bond ETF 3% 0 0 B8a. For each $1 long in the Airline ETF how much should you invest (long or short) in the other ETFs in order to hedge away the market and oil-price risk to create a zero-cost portfolio? State whether these are long or short positions and circle your answers. [10 marks] B8b. How much do you earn per $1 long the Airline ETF? [3 marks]