Answered step by step

Verified Expert Solution

Question

1 Approved Answer

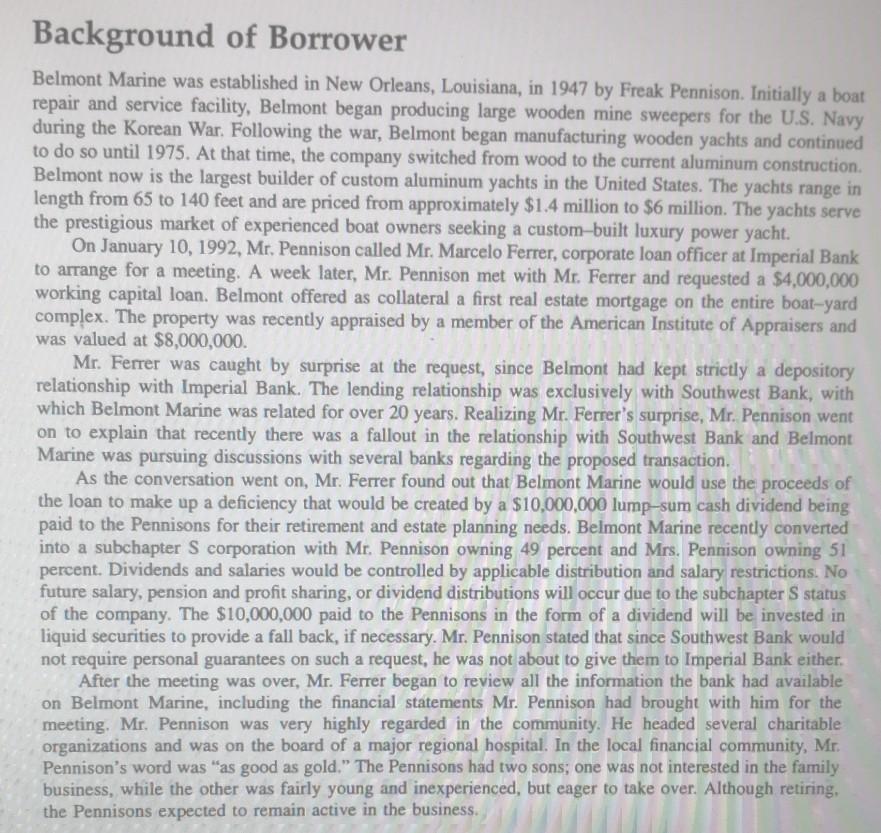

Background of Borrower Belmont Marine was established in New Orleans, Louisiana, in 1947 by Freak Pennison. Initially a boat repair and service facility, Belmont began

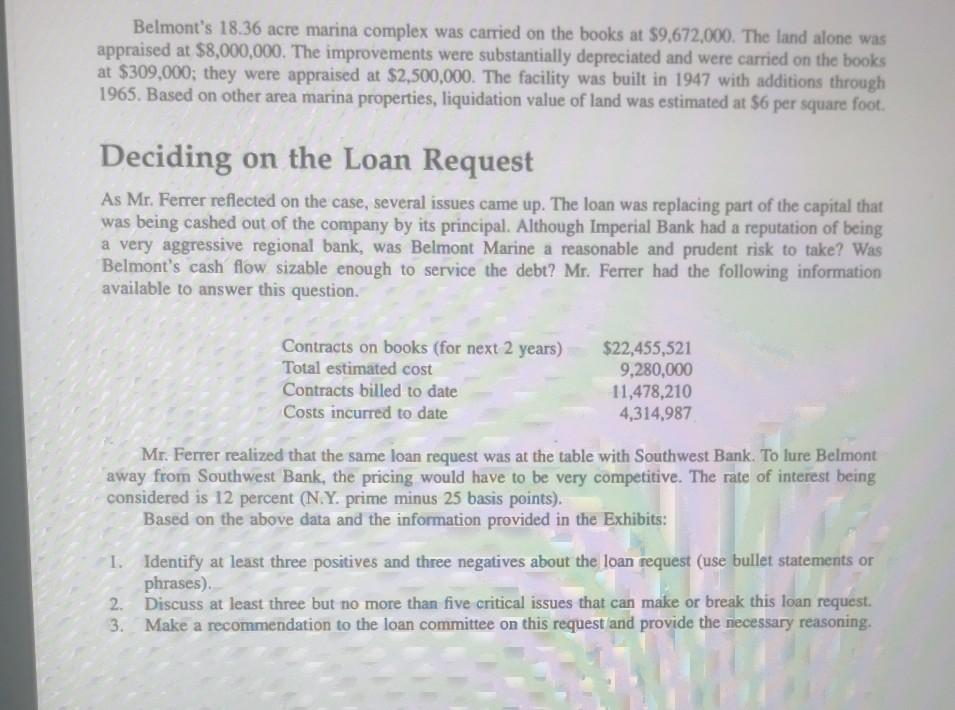

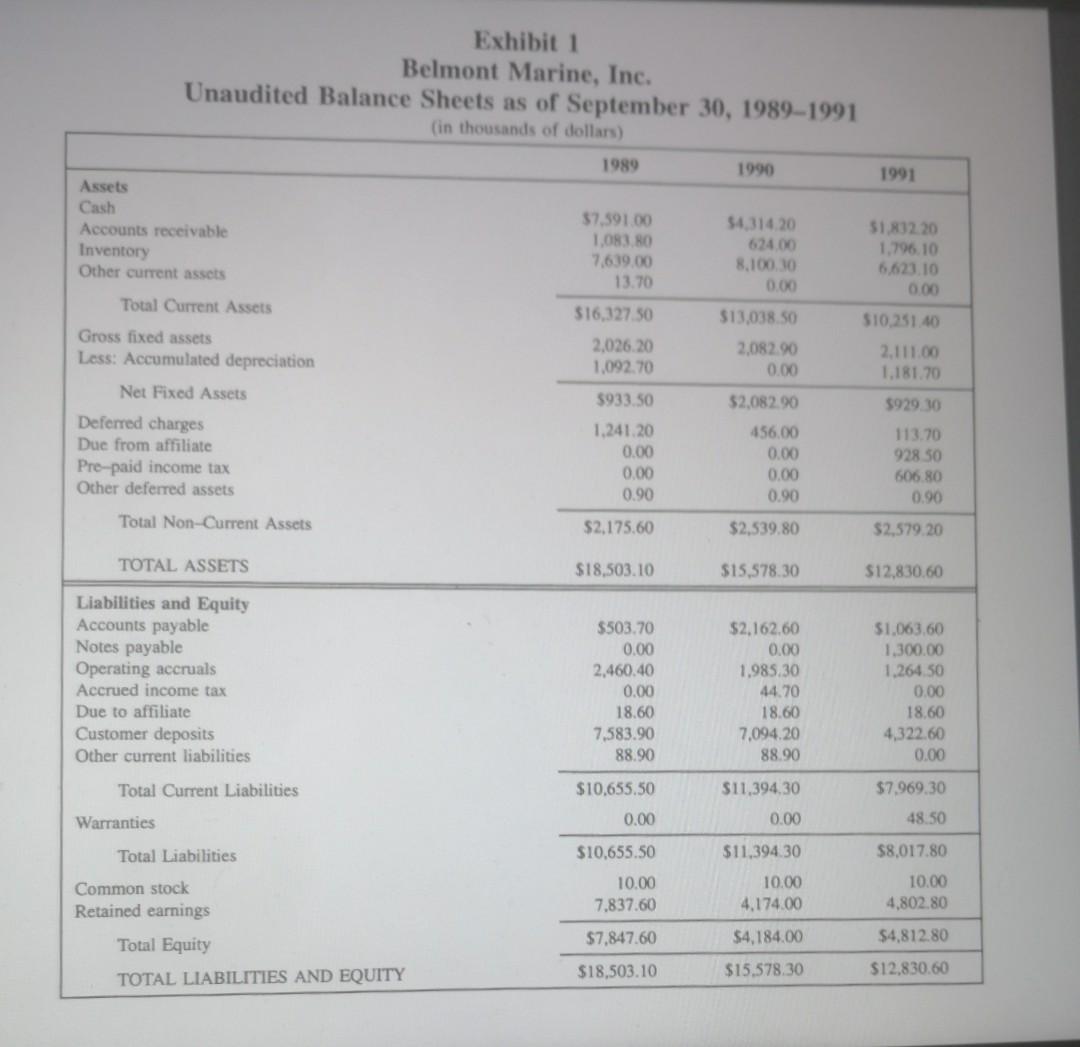

Background of Borrower Belmont Marine was established in New Orleans, Louisiana, in 1947 by Freak Pennison. Initially a boat repair and service facility, Belmont began producing large wooden mine sweepers for the U.S. Navy during the Korean War. Following the war, Belmont began manufacturing wooden yachts and continued to do so until 1975. At that time, the company switched from wood to the current aluminum construction. Belmont now is the largest builder of custom aluminum yachts in the United States. The yachts range in length from 65 to 140 feet and are priced from approximately $1.4 million to $6 million. The yachts serve the prestigious market of experienced boat owners seeking a custom-built luxury power yacht. On January 10, 1992, Mr. Pennison called Mr. Marcelo Ferrer, corporate loan officer at Imperial Bank to arrange for a meeting. A week later, Mr. Pennison met with Mr. Ferrer and requested a $4,000,000 working capital loan. Belmont offered as collateral a first real estate mortgage on the entire boat-yard complex. The property was recently appraised by a member of the American Institute of Appraisers and was valued at $8,000,000. Mr. Ferrer was caught by surprise at the request, since Belmont had kept strictly a depository relationship with Imperial Bank. The lending relationship was exclusively with Southwest Bank, with which Belmont Marine was related for over 20 years. Realizing Mr. Ferrer's surprise, Mr. Pennison went on to explain that recently there was a fallout in the relationship with Southwest Bank and Belmont Marine was pursuing discussions with several banks regarding the proposed transaction. As the conversation went on, Mr. Ferrer found out that Belmont Marine would use the proceeds of the loan to make up a deficiency that would be created by a $10,000,000 lump-sum cash dividend being paid to the Pennisons for their retirement and estate planning needs. Belmont Marine recently converted into a subchapter S corporation with Mr. Pennison owning 49 percent and Mrs. Pennison owning 51 percent. Dividends and salaries would be controlled by applicable distribution and salary restrictions. No future salary, pension and profit sharing, or dividend distributions will occur due to the subchapter S status of the company. The $10,000,000 paid to the Pennisons in the form of a dividend will be invested in liquid securities to provide a fall back, if necessary. Mr. Pennison stated that since Southwest Bank would not require personal guarantees on such a request, he was not about to give them to Imperial Bank either. After the meeting was over, Mr. Ferrer began to review all the information the bank had available on Belmont Marine, including the financial statements Mr. Pennison had brought with him for the meeting, Mr. Pennison was very highly regarded in the community. He headed several charitable organizations and was on the board of a major regional hospital. In the local financial community, Mr. Pennison's word was "as good as gold." The Pennisons had two sons; one was not interested in the family business, while the other was fairly young and inexperienced, but eager to take over. Although retiring, the Pennisons expected to remain active in the business. Belmont's 18.36 acre marina complex was carried on the books at $9,672,000. The land alone was appraised at $8,000,000. The improvements were substantially depreciated and were carried on the books at $309,000; they were appraised at $2,500,000. The facility was built in 1947 with additions through 1965. Based on other area marina properties, liquidation value of land was estimated at $6 per square foot. Deciding on the Loan Request As Mr. Ferrer reflected on the case, several issues came up. The loan was replacing part of the capital that was being cashed out of the company by its principal. Although Imperial Bank had a reputation of being a very aggressive regional bank, was Belmont Marine a reasonable and prudent risk to take? Was Belmont's cash flow sizable enough to service the debt? Mr. Ferrer had the following information available to answer this question. Contracts on books (for next 2 years) Total estimated cost Contracts billed to date Costs incurred to date $22,455,521 9,280,000 11,478,210 4,314,987 Mr. Ferrer realized that the same loan request was at the table with Southwest Bank. To lure Belmont away from Southwest Bank, the pricing would have to be very competitive. The rate of interest being considered is 12 percent (N.Y. prime minus 25 basis points). Based on the above data and the information provided in the Exhibits: 1. Identify at least three positives and three negatives about the loan request (use bullet statements or phrases). 2. Discuss at least three but no more than five critical issues that can make or break this loan request. 3. Make a recommendation to the loan committee on this request and provide the necessary reasoning. 1991 Exhibit 1 Belmont Marine, Inc. Unaudited Balance Sheets as of September 30, 1989-1991 (in thousands of dollars) 1989 1990 Assets Cash $7.591.00 54.314.20 Accounts receivable 1,083.80 624.00 Inventory 7,639.00 8.100.30 Other current assets 13.70 0.00 Total Current Assets 516,327.50 $13.038.50 Gross fixed assets 2,026 20 2,082.90 Less: Accumulated depreciation 1.092.70 0.00 Net Fixed Assets $933 50 52.082.00 Deferred charges 1.241.20 456.00 Due from affiliate 0.00 0.00 Pre-paid income tax 0.00 0.00 Other deferred assets 0.90 0.90 5181220 1.796.10 6,623.10 0.00 $10.251.40 2.111.00 1,181.70 5929 30 113.70 928 50 606 80 0.00 Total Non-Current Assets $2,175.60 $2,539.80 $2,579,20 TOTAL ASSETS $18,503.10 $15.578.30 $12,830.60 Liabilities and Equity Accounts payable Notes payable Operating accruals Accrued income tax Due to affiliate Customer deposits Other current liabilities $1.063.60 1.300.00 1.264.50 $503.70 0.00 2,460.40 0.00 18.60 7,583.90 88.90 $2.162.60 0.00 1.985.30 44.70 18.60 7,094.20 88.90 0.00 18.60 4,322.60 0.00 Total Current Liabilities $10.655.50 $7,969.30 $11,394,30 0.00 Warranties 0.00 48.50 Total Liabilities $10,655.50 $11.394.30 10.00 7.837.60 10.00 4.174.00 $8,017.80 10.00 4,802.80 Common stock Retained earnings Total Equity TOTAL LIABILITIES AND EQUITY $7,847.60 $4,184.00 $4,812.80 $18,503.10 $15.578.30 $12,830.60 Exhibit 2 Belmont Marine, Inc. Unaudited Income Statements for Years Ended September 30, 1989-1991 (in thousands of dollars) 1989 1990 1991 Sales Cost of sales $21.228.20 13,608.70 $17.447.70 11,729.60 $17.961.60 11.999.40 Gross Profit $7,619.50 $5,718.10 $5.962.20 Officers' salaries Pension sharing General and administrative expenses Total Expenses 2.250.00 1,863.80 2,351.80 1.000.10 522.00 3.290.10 1,000.00 536.30 2,940.40 $6,465.60 $4,812.20 $4,476.70 Operating Income $1.153.90 $905.90 $1,485.50 0.00 615.80 0.00 378.30 149.80 545.30 Interest expense Other income Profit before taxes Income taxes Net profit after taxes Extraordinary income $1.769.70 0.00 1,769.00 0.00 $1.284.20 651.00 633.20 $1.881.00 675.10 1.205.90 (290.60) 0.00 Net Income $1.769,70 $633.20 $915.30 Exhibit 3 Key Financial Data 1989 1990 1991 Working capital Tangible net worth Current ratio Sales/Working capital Past days sales in A/R* Past days cost of goods sold in inventory** Debt to worth Debt to tangible net worth -A/R X 365 - Sales. **Inventory x 365 - Cost of sales, $5,672.00 $7,847.60 1.53 3.74 18.63 204.89 1.36 1.36 $1,644.20 $4,184.00 1.14 10.61 13.05 252.06 2.72 2.72 $2,282.10 $3,884.30 1.25 7.87 36.50 201.46 1.67 2.06 Background of Borrower Belmont Marine was established in New Orleans, Louisiana, in 1947 by Freak Pennison. Initially a boat repair and service facility, Belmont began producing large wooden mine sweepers for the U.S. Navy during the Korean War. Following the war, Belmont began manufacturing wooden yachts and continued to do so until 1975. At that time, the company switched from wood to the current aluminum construction. Belmont now is the largest builder of custom aluminum yachts in the United States. The yachts range in length from 65 to 140 feet and are priced from approximately $1.4 million to $6 million. The yachts serve the prestigious market of experienced boat owners seeking a custom-built luxury power yacht. On January 10, 1992, Mr. Pennison called Mr. Marcelo Ferrer, corporate loan officer at Imperial Bank to arrange for a meeting. A week later, Mr. Pennison met with Mr. Ferrer and requested a $4,000,000 working capital loan. Belmont offered as collateral a first real estate mortgage on the entire boat-yard complex. The property was recently appraised by a member of the American Institute of Appraisers and was valued at $8,000,000. Mr. Ferrer was caught by surprise at the request, since Belmont had kept strictly a depository relationship with Imperial Bank. The lending relationship was exclusively with Southwest Bank, with which Belmont Marine was related for over 20 years. Realizing Mr. Ferrer's surprise, Mr. Pennison went on to explain that recently there was a fallout in the relationship with Southwest Bank and Belmont Marine was pursuing discussions with several banks regarding the proposed transaction. As the conversation went on, Mr. Ferrer found out that Belmont Marine would use the proceeds of the loan to make up a deficiency that would be created by a $10,000,000 lump-sum cash dividend being paid to the Pennisons for their retirement and estate planning needs. Belmont Marine recently converted into a subchapter S corporation with Mr. Pennison owning 49 percent and Mrs. Pennison owning 51 percent. Dividends and salaries would be controlled by applicable distribution and salary restrictions. No future salary, pension and profit sharing, or dividend distributions will occur due to the subchapter S status of the company. The $10,000,000 paid to the Pennisons in the form of a dividend will be invested in liquid securities to provide a fall back, if necessary. Mr. Pennison stated that since Southwest Bank would not require personal guarantees on such a request, he was not about to give them to Imperial Bank either. After the meeting was over, Mr. Ferrer began to review all the information the bank had available on Belmont Marine, including the financial statements Mr. Pennison had brought with him for the meeting, Mr. Pennison was very highly regarded in the community. He headed several charitable organizations and was on the board of a major regional hospital. In the local financial community, Mr. Pennison's word was "as good as gold." The Pennisons had two sons; one was not interested in the family business, while the other was fairly young and inexperienced, but eager to take over. Although retiring, the Pennisons expected to remain active in the business. Belmont's 18.36 acre marina complex was carried on the books at $9,672,000. The land alone was appraised at $8,000,000. The improvements were substantially depreciated and were carried on the books at $309,000; they were appraised at $2,500,000. The facility was built in 1947 with additions through 1965. Based on other area marina properties, liquidation value of land was estimated at $6 per square foot. Deciding on the Loan Request As Mr. Ferrer reflected on the case, several issues came up. The loan was replacing part of the capital that was being cashed out of the company by its principal. Although Imperial Bank had a reputation of being a very aggressive regional bank, was Belmont Marine a reasonable and prudent risk to take? Was Belmont's cash flow sizable enough to service the debt? Mr. Ferrer had the following information available to answer this question. Contracts on books (for next 2 years) Total estimated cost Contracts billed to date Costs incurred to date $22,455,521 9,280,000 11,478,210 4,314,987 Mr. Ferrer realized that the same loan request was at the table with Southwest Bank. To lure Belmont away from Southwest Bank, the pricing would have to be very competitive. The rate of interest being considered is 12 percent (N.Y. prime minus 25 basis points). Based on the above data and the information provided in the Exhibits: 1. Identify at least three positives and three negatives about the loan request (use bullet statements or phrases). 2. Discuss at least three but no more than five critical issues that can make or break this loan request. 3. Make a recommendation to the loan committee on this request and provide the necessary reasoning. 1991 Exhibit 1 Belmont Marine, Inc. Unaudited Balance Sheets as of September 30, 1989-1991 (in thousands of dollars) 1989 1990 Assets Cash $7.591.00 54.314.20 Accounts receivable 1,083.80 624.00 Inventory 7,639.00 8.100.30 Other current assets 13.70 0.00 Total Current Assets 516,327.50 $13.038.50 Gross fixed assets 2,026 20 2,082.90 Less: Accumulated depreciation 1.092.70 0.00 Net Fixed Assets $933 50 52.082.00 Deferred charges 1.241.20 456.00 Due from affiliate 0.00 0.00 Pre-paid income tax 0.00 0.00 Other deferred assets 0.90 0.90 5181220 1.796.10 6,623.10 0.00 $10.251.40 2.111.00 1,181.70 5929 30 113.70 928 50 606 80 0.00 Total Non-Current Assets $2,175.60 $2,539.80 $2,579,20 TOTAL ASSETS $18,503.10 $15.578.30 $12,830.60 Liabilities and Equity Accounts payable Notes payable Operating accruals Accrued income tax Due to affiliate Customer deposits Other current liabilities $1.063.60 1.300.00 1.264.50 $503.70 0.00 2,460.40 0.00 18.60 7,583.90 88.90 $2.162.60 0.00 1.985.30 44.70 18.60 7,094.20 88.90 0.00 18.60 4,322.60 0.00 Total Current Liabilities $10.655.50 $7,969.30 $11,394,30 0.00 Warranties 0.00 48.50 Total Liabilities $10,655.50 $11.394.30 10.00 7.837.60 10.00 4.174.00 $8,017.80 10.00 4,802.80 Common stock Retained earnings Total Equity TOTAL LIABILITIES AND EQUITY $7,847.60 $4,184.00 $4,812.80 $18,503.10 $15.578.30 $12,830.60 Exhibit 2 Belmont Marine, Inc. Unaudited Income Statements for Years Ended September 30, 1989-1991 (in thousands of dollars) 1989 1990 1991 Sales Cost of sales $21.228.20 13,608.70 $17.447.70 11,729.60 $17.961.60 11.999.40 Gross Profit $7,619.50 $5,718.10 $5.962.20 Officers' salaries Pension sharing General and administrative expenses Total Expenses 2.250.00 1,863.80 2,351.80 1.000.10 522.00 3.290.10 1,000.00 536.30 2,940.40 $6,465.60 $4,812.20 $4,476.70 Operating Income $1.153.90 $905.90 $1,485.50 0.00 615.80 0.00 378.30 149.80 545.30 Interest expense Other income Profit before taxes Income taxes Net profit after taxes Extraordinary income $1.769.70 0.00 1,769.00 0.00 $1.284.20 651.00 633.20 $1.881.00 675.10 1.205.90 (290.60) 0.00 Net Income $1.769,70 $633.20 $915.30 Exhibit 3 Key Financial Data 1989 1990 1991 Working capital Tangible net worth Current ratio Sales/Working capital Past days sales in A/R* Past days cost of goods sold in inventory** Debt to worth Debt to tangible net worth -A/R X 365 - Sales. **Inventory x 365 - Cost of sales, $5,672.00 $7,847.60 1.53 3.74 18.63 204.89 1.36 1.36 $1,644.20 $4,184.00 1.14 10.61 13.05 252.06 2.72 2.72 $2,282.10 $3,884.30 1.25 7.87 36.50 201.46 1.67 2.06

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Designing Strategic Cost Systems How To Unleash The Power Of Cost Information

Authors: Lianabel Oliver

1st Edition

9780471653585