Based on the case study for Keith and Cindy Ross :

3. Ross Big-N-Tall has been profitable for the past several years. Last year's net income was $440,000. If you used a discount rate of 3% above the expected return for aggressive stocks, what would be the value of the business using the capitalized earnings approach?

4. The net income in the previous year was $440,000. The income from the company can be expected to grow in the future at least at the rate of inflation. How would these additional facts affect your valuation? What model would you use to value the company?

7. Which benchmark would be the best choice to review the performance of Keith's Growth Mutual Fund?

9. If Keith sold the shares of the growth mutual fund on January1, 2017, what would be his after-tax annualized rate of return since he first purchased the shares?

10. If Keith needs additional cash, what would be the net proceeds from the sale of the Balanced Mutual Fund IRA (listed on his personal Statement of Financial Position), including any taxes and penalties and assuming no basis?

13. What is the implication of Keith directly paying to the insurer the future premiums for Policy 1?

14. What are the consequences if, instead of directly paying the premiums, Keith simply adds $12,000 each January 1 to the trust to pay the premiums?

15. What if Cindy assigns her coverage of the term insurance policy of $100,000 to the Ross Childrens Insurance Trust?

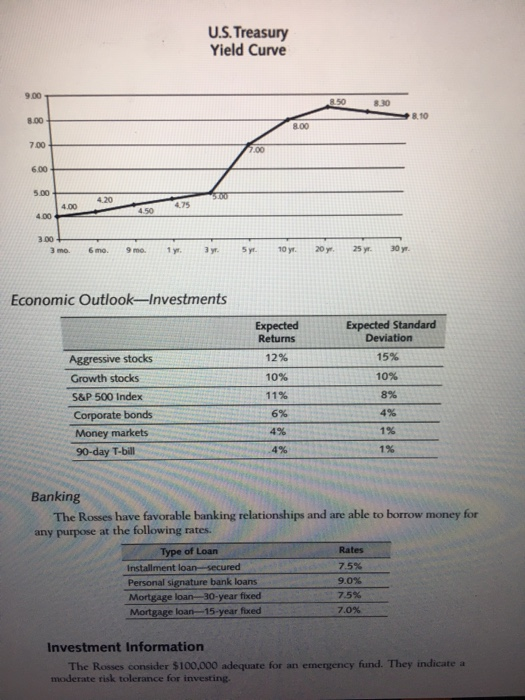

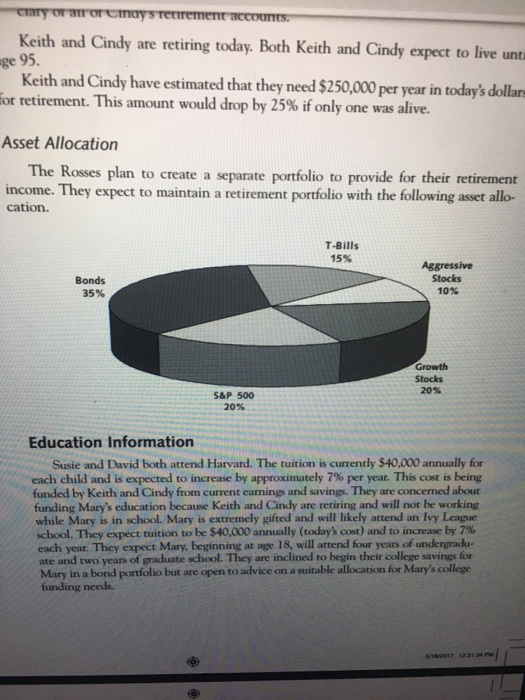

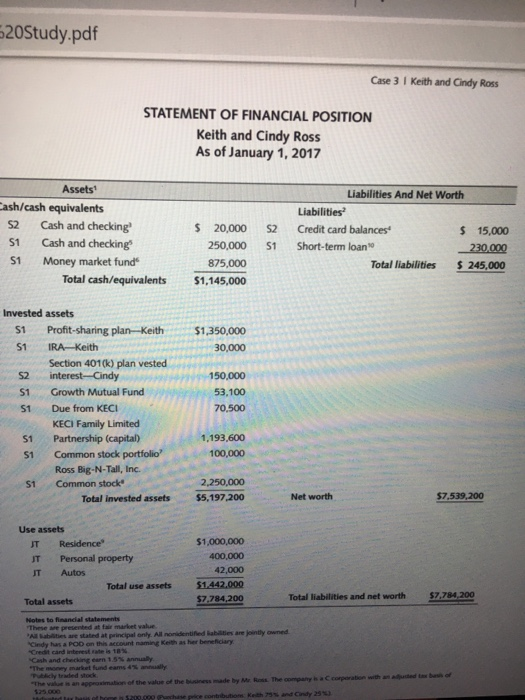

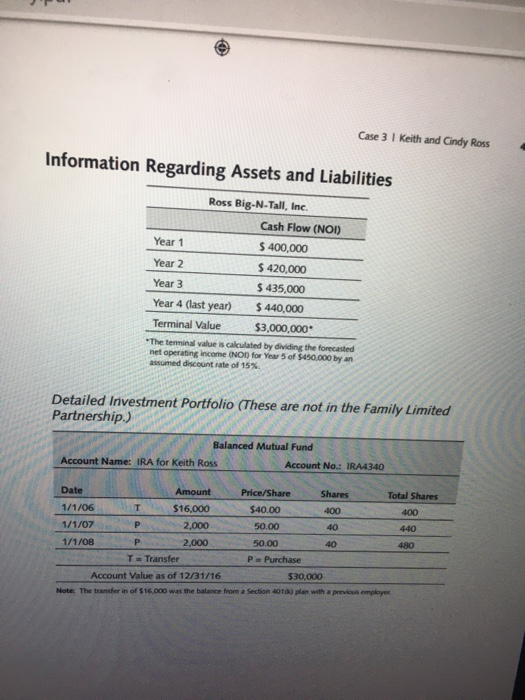

U.S. Treasury Yield Curve 8.00 3 momomo Economic Outlook-Investments Expected Returns 12% Expected Standard Deviation 15% 10% 8% 10% Aggressive stocks Growth stocks S&P 500 Index Corporate bonds Money markets 90-day T-bill Banking The Rosses have favorable banking relationships and are able to borrow money for any purpose at the following rates. Type of Loan Installment loansecured 7.5% Personal signature bank loans Mortgage loan-30-year fixed Mortgage loan 15-year foxed Investment Information The Rosses consider $100,000 adequate for an emergency fund. They indicate a moderate risk tolerance for investing. Crary Or MTOTO s Tetirement accounts. Keith and Cindy are retiring today. Both Keith and Cindy expect to live unti age 95. Keith and Cindy have estimated that they need $250,000 per year in today's dollar for retirement. This amount would drop by 25% if only one was alive. Asset Allocation The Rosses plan to create a separate portfolio to provide for their retirement income. They expect to maintain a retirement portfolio with the following asset allo- cation. T-Bills 15% Bonds 35% Aggressive Stocks 10% Growth Stocks 20% S&P 500 20% Education Information Susie and David both attend Harvard. The tuition is currently $40,000 annually for each child and is expected to increase by approximately 7% per year. This cost is being funded by Keith and Cindy from current earnings and savings. They are concerned abour funding Mary's education because Keith and Cindy are retiring and will not be working while Mary is in school. Mary is extremely gifted and will likely attend an Ivy League school. They expect tuition to be $40,000 annually (today cost) and to increase by 7% each year. They expect Mary, beginning at age 18, will attend four years of undergradu ate and two years of graduate school. They are inclined to begin their college savings for Mary in a bond portfolio but are open to advice on a suitable allocation for Mary's college funding needs. 7 12:31:34 20Study.pdf Case 3 Keith and Cindy Ross STATEMENT OF FINANCIAL POSITION Keith and Cindy Ross As of January 1, 2017 Assets ash/cash equivalents 52 Cash and checking! 51 Cash and checkings 51 Money market funds Total cash/equivalents S2 51 $ 20,000 250,000 875,000 $1,145,000 Liabilities And Net Worth Liabilities Credit card balances $ 15,000 Short-term loan 230.000 Total liabilities $245,000 $1,350,000 30,000 Invested assets 51 Profit-sharing plan-Keith S1 TRA Keith Section 401(k) plan vested S2 interest-Cindy S1 Growth Mutual Fund 51 Due from KECI KECI Family Limited 51 Partnership (capital) 51 Common stock portfolio Ross Big-N-Tall, Inc. 51 Common stock Total invested assets 150,000 53,100 70.500 1,193,600 100,000 2,250,000 $5,197,200 Net worth 57,539,200 Use assets JT Residence JT Personal property JT Autos Total use assets Total assets $1,000,000 400,000 42,000 51.442.000 57.784 200 Total liabilities and net worth $7.784200 A are stated at walan Allied Beatly owned dy has a POD on this account namine kehas her beneficiary Case 3 | Keith and Cindy Ross Information Regarding Assets and Liabilities Ross Big.N Tall, Inc Cash Flow (NOI) Year 1 $ 400,000 Year 2 $ 420,000 Year 3 $ 435,000 Year 4 (last year) $440,000 Terminal Value $3,000,000 *The terminal value is calculated by dividing the forecasted net operating income NON for Year 5 of $450.000 by an assumed discount rate of 15% Detailed Investment Portfolio (These are not in the Family Limited Partnership.) Balanced Mutual Fund Account Name: IRA for Keith Ross Account No.: RA4340 Date Amount Price/Share Shares Total Shares 1/1/06 H T $16,000 $40.00 400 400 1/1/07 P 2 ,000 50.00 40 4 40 1/1/0B P 2 ,000 50.00 40 4 80 T-Transfer P Purchase Account Value as of 12/31/16 $30,000 Note: The transfer in of $16,000 was the balance from a Section 40103 plan with a previous employer U.S. Treasury Yield Curve 8.00 3 momomo Economic Outlook-Investments Expected Returns 12% Expected Standard Deviation 15% 10% 8% 10% Aggressive stocks Growth stocks S&P 500 Index Corporate bonds Money markets 90-day T-bill Banking The Rosses have favorable banking relationships and are able to borrow money for any purpose at the following rates. Type of Loan Installment loansecured 7.5% Personal signature bank loans Mortgage loan-30-year fixed Mortgage loan 15-year foxed Investment Information The Rosses consider $100,000 adequate for an emergency fund. They indicate a moderate risk tolerance for investing. Crary Or MTOTO s Tetirement accounts. Keith and Cindy are retiring today. Both Keith and Cindy expect to live unti age 95. Keith and Cindy have estimated that they need $250,000 per year in today's dollar for retirement. This amount would drop by 25% if only one was alive. Asset Allocation The Rosses plan to create a separate portfolio to provide for their retirement income. They expect to maintain a retirement portfolio with the following asset allo- cation. T-Bills 15% Bonds 35% Aggressive Stocks 10% Growth Stocks 20% S&P 500 20% Education Information Susie and David both attend Harvard. The tuition is currently $40,000 annually for each child and is expected to increase by approximately 7% per year. This cost is being funded by Keith and Cindy from current earnings and savings. They are concerned abour funding Mary's education because Keith and Cindy are retiring and will not be working while Mary is in school. Mary is extremely gifted and will likely attend an Ivy League school. They expect tuition to be $40,000 annually (today cost) and to increase by 7% each year. They expect Mary, beginning at age 18, will attend four years of undergradu ate and two years of graduate school. They are inclined to begin their college savings for Mary in a bond portfolio but are open to advice on a suitable allocation for Mary's college funding needs. 7 12:31:34 20Study.pdf Case 3 Keith and Cindy Ross STATEMENT OF FINANCIAL POSITION Keith and Cindy Ross As of January 1, 2017 Assets ash/cash equivalents 52 Cash and checking! 51 Cash and checkings 51 Money market funds Total cash/equivalents S2 51 $ 20,000 250,000 875,000 $1,145,000 Liabilities And Net Worth Liabilities Credit card balances $ 15,000 Short-term loan 230.000 Total liabilities $245,000 $1,350,000 30,000 Invested assets 51 Profit-sharing plan-Keith S1 TRA Keith Section 401(k) plan vested S2 interest-Cindy S1 Growth Mutual Fund 51 Due from KECI KECI Family Limited 51 Partnership (capital) 51 Common stock portfolio Ross Big-N-Tall, Inc. 51 Common stock Total invested assets 150,000 53,100 70.500 1,193,600 100,000 2,250,000 $5,197,200 Net worth 57,539,200 Use assets JT Residence JT Personal property JT Autos Total use assets Total assets $1,000,000 400,000 42,000 51.442.000 57.784 200 Total liabilities and net worth $7.784200 A are stated at walan Allied Beatly owned dy has a POD on this account namine kehas her beneficiary Case 3 | Keith and Cindy Ross Information Regarding Assets and Liabilities Ross Big.N Tall, Inc Cash Flow (NOI) Year 1 $ 400,000 Year 2 $ 420,000 Year 3 $ 435,000 Year 4 (last year) $440,000 Terminal Value $3,000,000 *The terminal value is calculated by dividing the forecasted net operating income NON for Year 5 of $450.000 by an assumed discount rate of 15% Detailed Investment Portfolio (These are not in the Family Limited Partnership.) Balanced Mutual Fund Account Name: IRA for Keith Ross Account No.: RA4340 Date Amount Price/Share Shares Total Shares 1/1/06 H T $16,000 $40.00 400 400 1/1/07 P 2 ,000 50.00 40 4 40 1/1/0B P 2 ,000 50.00 40 4 80 T-Transfer P Purchase Account Value as of 12/31/16 $30,000 Note: The transfer in of $16,000 was the balance from a Section 40103 plan with a previous employer