Based on the memorandum in Exhibit 4, please create a table for the capital budgeting of the case.

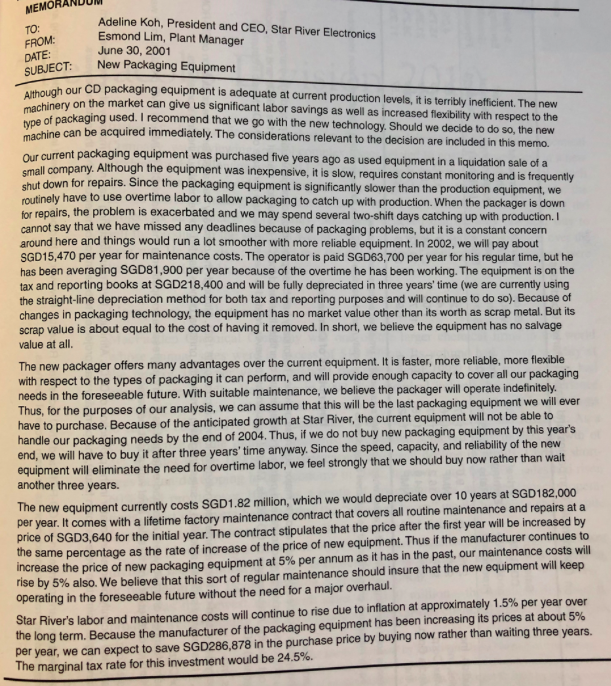

MEMOR TO FROM: DATE SUBJECT: Adeline Koh, President and CEO, Star River Electronics Esmond Lim, Plant Manager June 30, 2001 New Packaging Equipment Although our CD packaging equipment is adequate at current production levels, it is terribly inefficient. The price machinery on the market can give us significant labor savings as well as increased flexibility with respect to the type of packaging used. I recommend that we go with the new technology. Should we decide to do so, the new machine can be acquired immediately. The considerations relevant to the decision are included in this memo. Our current packaging equipment was purchased five years ago as used equipment in a liquidation sale of a small company. Although the equipment was inexpensive, it is slow, requires constant monitoring and is frequently shut down for repairs. Since the packaging equipment is significantly slower than the production equipment, we routinely have to use overtime labor to allow packaging to catch up with production. When the packager is down for repairs, the problem is exacerbated and we may spend several two-shift days catching up with production. I cannot say that we have missed any deadlines because of packaging problems, but it is a constant concern around here and things would run a lot smoother with more reliable equipment. In 2002, we will pay about SGD15,470 per year for maintenance costs. The operator is paid SGD63,700 per year for his regular time, but he has been averaging SGD81,900 per year because of the overtime he has been working. The equipment is on the tax and reporting books at SGD218,400 and will be fully depreciated in three years' time (we are currently using the straight-line depreciation method for both tax and reporting purposes and will continue to do so). Because of changes in packaging technology, the equipment has no market value other than its worth as scrap metal. But its scrap value is about equal to the cost of having it removed. In short, we believe the equipment has no salvage value at all. The new packager offers many advantages over the current equipment. It is faster, more reliable, more flexible with respect to the types of packaging it can perform, and will provide enough capacity to cover all our packaging needs in the foreseeable future. With suitable maintenance, we believe the packager will operate indefinitely. Thus, for the purposes of our analysis, we can assume that this will be the last packaging equipment we will ever have to purchase. Because of the anticipated growth at Star River, the current equipment will not be able to handle our packaging needs by the end of 2004. Thus, if we do not buy new packaging equipment by this year's end, we will have to buy it after three years' time anyway. Since the speed, capacity, and reliability of the new equipment will eliminate the need for overtime labor, we feel strongly that we should buy now rather than wait another three years. The new equipment currently costs SGD1.82 million, which we would depreciate over 10 years at SGD182,000 per year. It comes with a lifetime factory maintenance contract that covers all routine maintenance and repairs at a price of SGD3,640 for the initial year. The contract stipulates that the price after the first year will be increased by the same percentage as the rate of increase of the price of new equipment. Thus if the manufacturer continues to increase the price of new packaging equipment at 5% per annum as it has in the past, our maintenance costs will rise by 5% also. We believe that this sort of regular maintenance should insure that the new equipment will keep operating in the foreseeable future without the need for a major overhaul. Star River's labor and maintenance costs will continue to rise due to inflation at approximately 1.5% per year over the long term. Because the manufacturer of the packaging equipment has been increasing its prices at about 5% per year, we can expect to save SGD286,878 in the purchase price by buying now rather than waiting three years. The marginal tax rate for this investment would be 24.5%. MEMOR TO FROM: DATE SUBJECT: Adeline Koh, President and CEO, Star River Electronics Esmond Lim, Plant Manager June 30, 2001 New Packaging Equipment Although our CD packaging equipment is adequate at current production levels, it is terribly inefficient. The price machinery on the market can give us significant labor savings as well as increased flexibility with respect to the type of packaging used. I recommend that we go with the new technology. Should we decide to do so, the new machine can be acquired immediately. The considerations relevant to the decision are included in this memo. Our current packaging equipment was purchased five years ago as used equipment in a liquidation sale of a small company. Although the equipment was inexpensive, it is slow, requires constant monitoring and is frequently shut down for repairs. Since the packaging equipment is significantly slower than the production equipment, we routinely have to use overtime labor to allow packaging to catch up with production. When the packager is down for repairs, the problem is exacerbated and we may spend several two-shift days catching up with production. I cannot say that we have missed any deadlines because of packaging problems, but it is a constant concern around here and things would run a lot smoother with more reliable equipment. In 2002, we will pay about SGD15,470 per year for maintenance costs. The operator is paid SGD63,700 per year for his regular time, but he has been averaging SGD81,900 per year because of the overtime he has been working. The equipment is on the tax and reporting books at SGD218,400 and will be fully depreciated in three years' time (we are currently using the straight-line depreciation method for both tax and reporting purposes and will continue to do so). Because of changes in packaging technology, the equipment has no market value other than its worth as scrap metal. But its scrap value is about equal to the cost of having it removed. In short, we believe the equipment has no salvage value at all. The new packager offers many advantages over the current equipment. It is faster, more reliable, more flexible with respect to the types of packaging it can perform, and will provide enough capacity to cover all our packaging needs in the foreseeable future. With suitable maintenance, we believe the packager will operate indefinitely. Thus, for the purposes of our analysis, we can assume that this will be the last packaging equipment we will ever have to purchase. Because of the anticipated growth at Star River, the current equipment will not be able to handle our packaging needs by the end of 2004. Thus, if we do not buy new packaging equipment by this year's end, we will have to buy it after three years' time anyway. Since the speed, capacity, and reliability of the new equipment will eliminate the need for overtime labor, we feel strongly that we should buy now rather than wait another three years. The new equipment currently costs SGD1.82 million, which we would depreciate over 10 years at SGD182,000 per year. It comes with a lifetime factory maintenance contract that covers all routine maintenance and repairs at a price of SGD3,640 for the initial year. The contract stipulates that the price after the first year will be increased by the same percentage as the rate of increase of the price of new equipment. Thus if the manufacturer continues to increase the price of new packaging equipment at 5% per annum as it has in the past, our maintenance costs will rise by 5% also. We believe that this sort of regular maintenance should insure that the new equipment will keep operating in the foreseeable future without the need for a major overhaul. Star River's labor and maintenance costs will continue to rise due to inflation at approximately 1.5% per year over the long term. Because the manufacturer of the packaging equipment has been increasing its prices at about 5% per year, we can expect to save SGD286,878 in the purchase price by buying now rather than waiting three years. The marginal tax rate for this investment would be 24.5%