Answered step by step

Verified Expert Solution

Question

1 Approved Answer

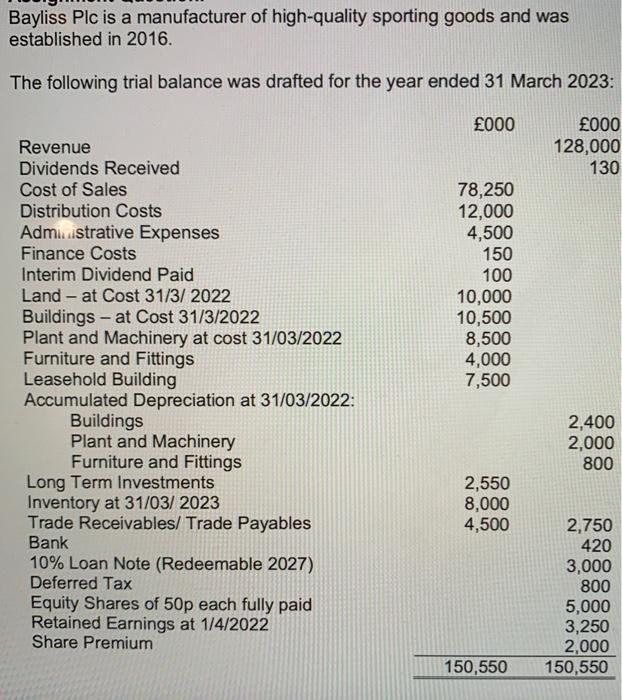

Bayliss Plc is a manufacturer of high-quality sporting goods and was established in 2016. The following trial balance was drafted for the year ended

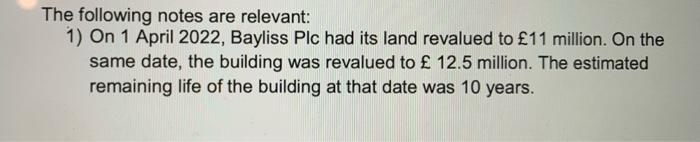

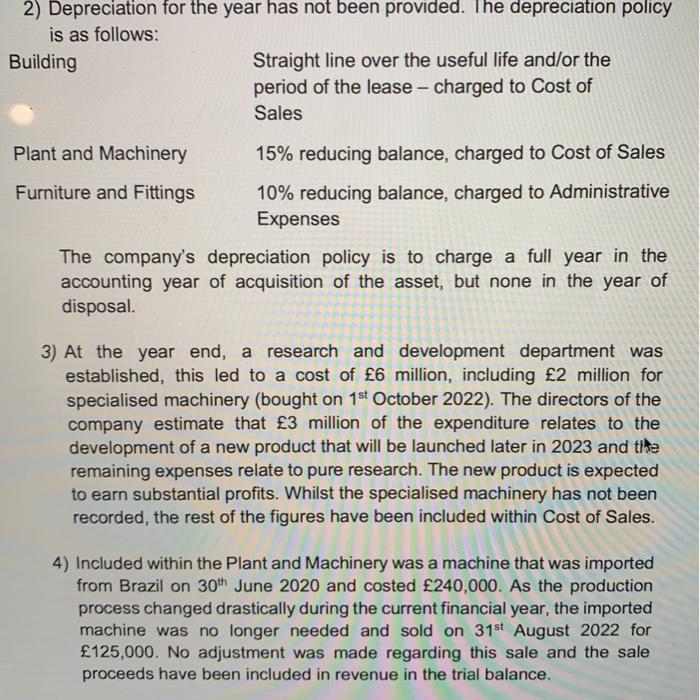

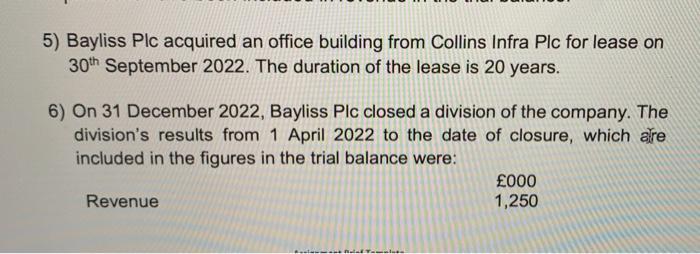

Bayliss Plc is a manufacturer of high-quality sporting goods and was established in 2016. The following trial balance was drafted for the year ended 31 March 2023: 000 Cost of Sales Revenue Dividends Received Distribution Costs Administrative Expenses Finance Costs Interim Dividend Paid 000 128,000 130 78,250 12,000 4,500 150 100 - Land at Cost 31/3/2022 10,000 - Buildings at Cost 31/3/2022 10,500 Plant and Machinery at cost 31/03/2022 8,500 Furniture and Fittings 4,000 Leasehold Building 7,500 Accumulated Depreciation at 31/03/2022: Buildings 2,400 Plant and Machinery 2,000 Furniture and Fittings 800 Long Term Investments 2,550 Inventory at 31/03/2023 8,000 Trade Receivables/ Trade Payables 4,500 2,750 Bank 420 10% Loan Note (Redeemable 2027) 3,000 Deferred Tax 800 Equity Shares of 50p each fully paid Retained Earnings at 1/4/2022 5,000 3,250 Share Premium 2,000 150,550 150,550 The following notes are relevant: 1) On 1 April 2022, Bayliss Plc had its land revalued to 11 million. On the same date, the building was revalued to 12.5 million. The estimated remaining life of the building at that date was 10 years. 2) Depreciation for the year has not been provided. The depreciation policy is as follows: Building Plant and Machinery Furniture and Fittings Straight line over the useful life and/or the period of the lease - charged to Cost of Sales 15% reducing balance, charged to Cost of Sales 10% reducing balance, charged to Administrative Expenses The company's depreciation policy is to charge a full year in the accounting year of acquisition of the asset, but none in the year of disposal. 3) At the year end, a research and development department was established, this led to a cost of 6 million, including 2 million for specialised machinery (bought on 1st October 2022). The directors of the company estimate that 3 million of the expenditure relates to the development of a new product that will be launched later in 2023 and the remaining expenses relate to pure research. The new product is expected to earn substantial profits. Whilst the specialised machinery has not been recorded, the rest of the figures have been included within Cost of Sales. 4) Included within the Plant and Machinery was a machine that was imported from Brazil on 30th June 2020 and costed 240,000. As the production process changed drastically during the current financial year, the imported machine was no longer needed and sold on 31st August 2022 for 125,000. No adjustment was made regarding this sale and the sale proceeds have been included in revenue in the trial balance. 5) Bayliss Plc acquired an office building from Collins Infra Plc for lease on 30th September 2022. The duration of the lease is 20 years. 6) On 31 December 2022, Bayliss Plc closed a division of the company. The division's results from 1 April 2022 to the date of closure, which are included in the figures in the trial balance were: Revenue 000 1,250 Cost of Sales 1,650 The directors of the company decided to sell the plant and machinery used by the discontinued division and started to locate a buyer. The plant had a carrying value at 1 April 2022 of 800,000 made up of a cost of 3.5 million and accumulated depreciation of 2.7 million. As there is demand for such an asset, the company is relatively confident that this asset would be sold in a short amount of time. The current market value of the plant is 1 million and it would cost 300,000 to dismantle the machinery to make it available to the purchaser. 7) The inventory at 31 March 2023 includes 5 million of slow-moving goods. Bayliss Plc is trying to sell these to another company but has not been successful in obtaining a reasonable offer. The best price it has been offered is 3 million. 8) Furthermore, inventory had a number of slow-moving items which had cost value of 4 million and a market value of 3 million, these slow moving items have not been included within the accounts. Additionally, during the year end stock-take the auditors noticed that 550,000 of inventory was missing, this had been included in the trial balance. The auditors suspect that the missing inventory might have been stolen. 9) Corporate taxation is to be provided at a rate of 20% of the net profit on continuing activities as shown in the statement of profit and loss. Bayliss Plc accounts for deferred taxation in accordance with IAS 12. At 31st March 2023 the difference between the carrying amounts of the net assets of Bayliss Plc and their (lower) tax base was 3,750,000.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Economics In Minutes 200 Key Concepts Explained In An Instant

Authors: Niall Kishtainy

1st Edition

1782066470, 9781782066477