Question: BCOR 3010 Assignment 2 - The Accounting Cycle Version C You have been hired by Gnomeo, Inc., a company that buys and resells miniature garden

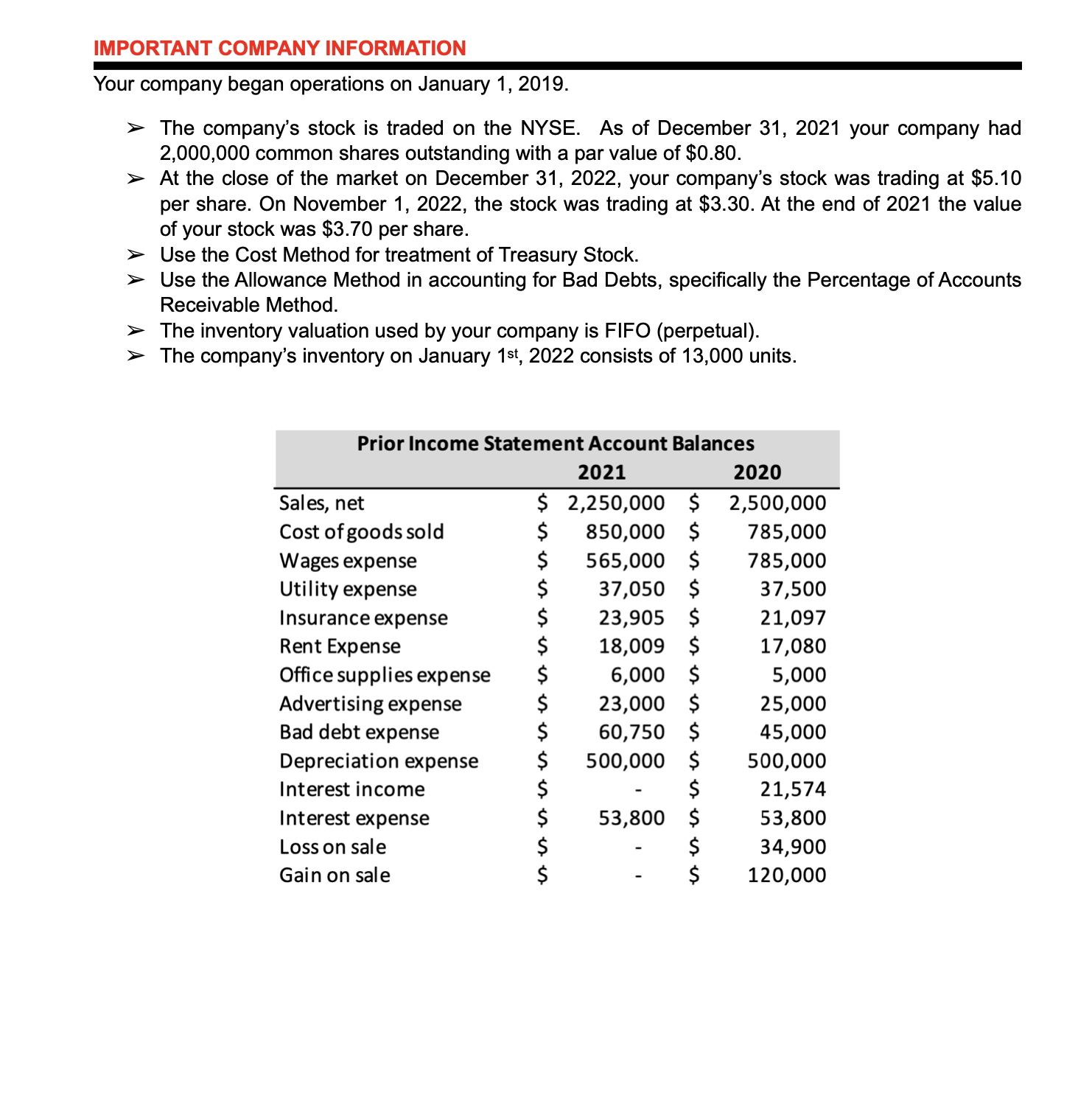

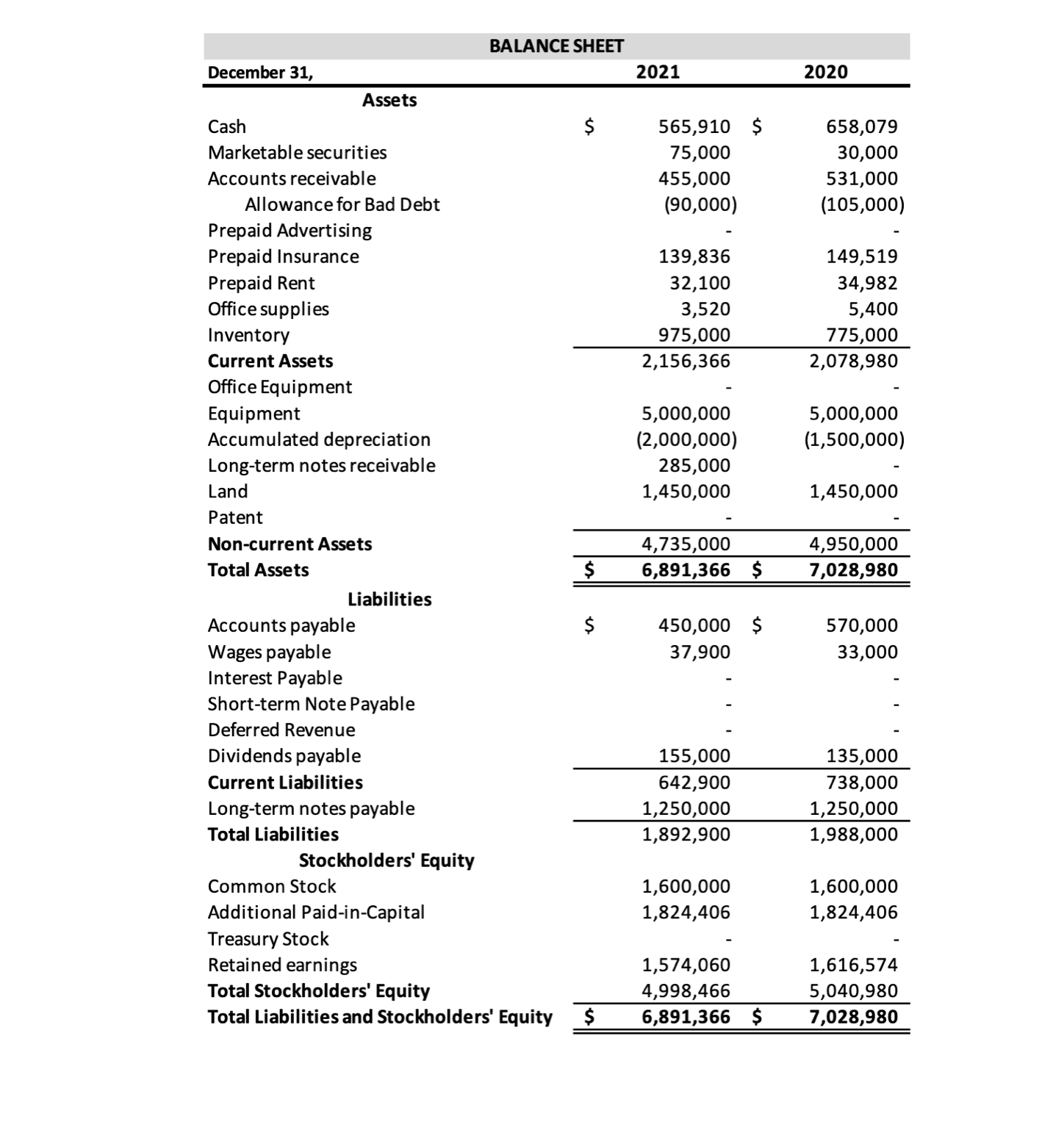

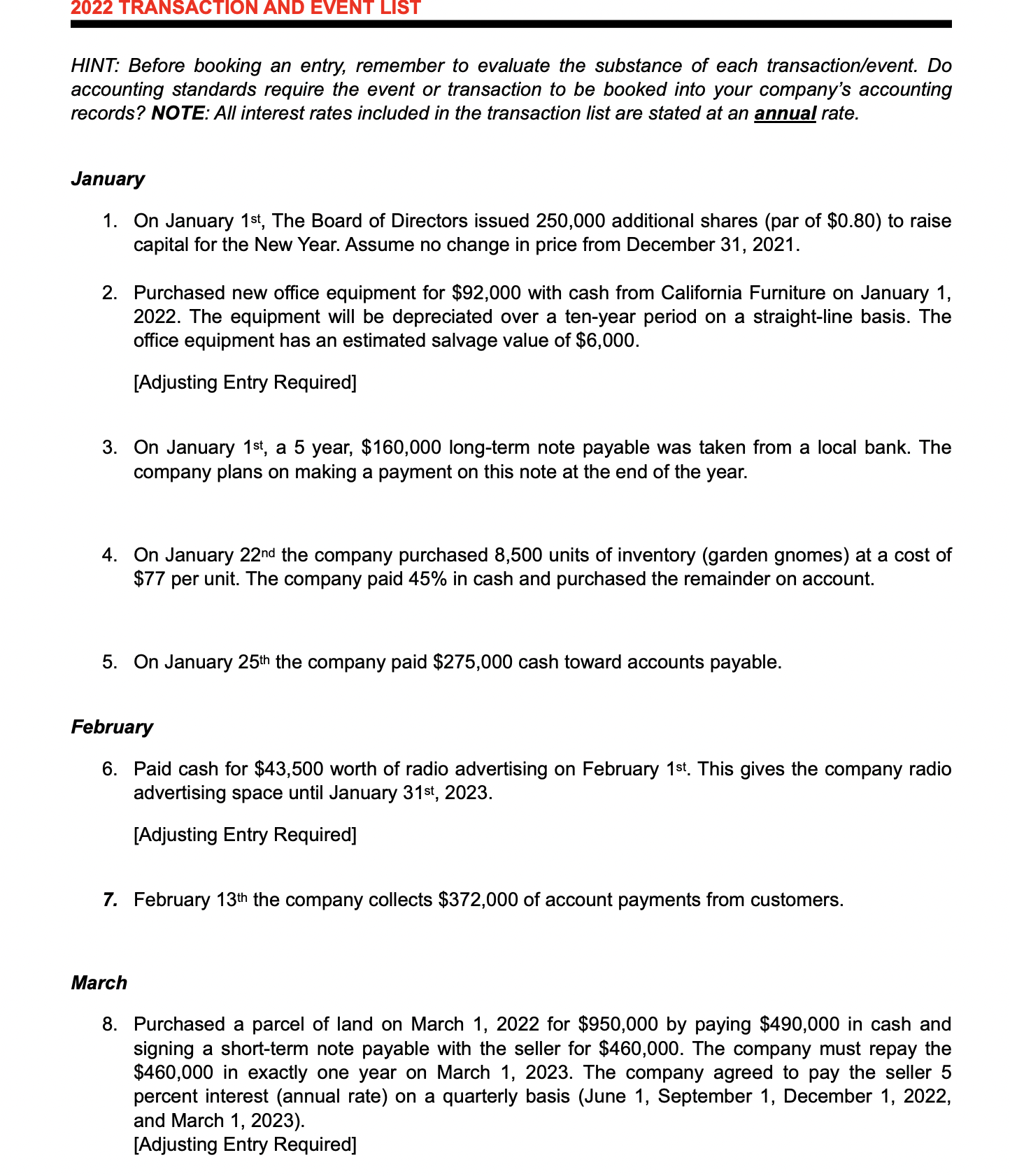

BCOR 3010 Assignment 2 - The Accounting Cycle Version C You have been hired by Gnomeo, Inc., a company that buys and resells miniature garden gnomes. The company started business on January 1,2019 . The chief accountant has asked you to compile a set of financial statements that can be presented to current and potential investors. She hands you a list of transactions that need to be recorded in the accounting records before the financial statements for the year ended December 31, 2022, can be prepared. Your job is to record the transactions, adjusting entries, post all entries and prepare the financial statements - basically complete the accounting cycle. RECORD ENTRIES AND BUILD THE FINANCIAL STATEMENTS 1. Journal Entry List Record entries from the transaction and event list provided below in proper journal entry format. NOTE: You are recording entries for the fiscal year 2022 (Jan 1 - Dec 31). This list must be organized. Make sure that I can easily identify the journal entry or adjusting journal entry with the related transaction/event. Show your work if the entry requires you to make a calculation (i.e. depreciation, interest expense, etc.). 2. Chart of T-Accounts Create a chart of T-Accounts and post each journal entry to the appropriate accounts. 3. Financial Statements Build a multi-step income statement, a statement of retained earnings, and a classified balance sheet for the year ending December 31, 2022 (include all three years of data for 2022, 2021 and 2020 on all financial statements). Create a statement of cash flows for 2022 and 2021 using the indirect method for operating cash flows. SUBMIT THE FOLLOWING You will turn in a physical copy of your work in the following order: 1. A cover page with the names of the members of your group. 2. Financial Statements (in the following order): - Income Statement (2022,2021, and 2020) - Statement of Retained Earnings (2022, 2021, and 2020) - Balance Sheet (2022,2021, and 2020) - Statement of Cash Flows (2022 and 2021) 3. Include the following supporting documentation: Journal Entry List, Chart of TAccounts, and Inventory Tracking Schedule. IMPORTANT COMPANY INFORMATION Your company began operations on January 1, 2019. > The company's stock is traded on the NYSE. As of December 31, 2021 your company had 2,000,000 common shares outstanding with a par value of $0.80. > At the close of the market on December 31, 2022, your company's stock was trading at $5.10 per share. On November 1, 2022, the stock was trading at $3.30. At the end of 2021 the value of your stock was $3.70 per share. > Use the Cost Method for treatment of Treasury Stock. > Use the Allowance Method in accounting for Bad Debts, specifically the Percentage of Accounts Receivable Method. > The inventory valuation used by your company is FIFO (perpetual). > The company's inventory on January 1st, 2022 consists of 13,000 units. \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{5}{|c|}{ BALANCE SHEET } \\ \hline December 31, & & 2021 & & 2020 \\ \hline \multicolumn{5}{|l|}{ Assets } \\ \hline Cash & $ & 565,910 & $ & 658,079 \\ \hline Marketable securities & & 75,000 & & 30,000 \\ \hline Accounts receivable & & 455,000 & & 531,000 \\ \hline Allowance for Bad Debt & & (90,000) & & (105,000) \\ \hline Prepaid Advertising & & - & & - \\ \hline Prepaid Insurance & & 139,836 & & 149,519 \\ \hline Prepaid Rent & & 32,100 & & 34,982 \\ \hline Office supplies & & 3,520 & & 5,400 \\ \hline Inventory & & 975,000 & & 775,000 \\ \hline Current Assets & & 2,156,366 & & 2,078,980 \\ \hline Office Equipment & & - & & - \\ \hline Equipment & & 5,000,000 & & 5,000,000 \\ \hline Accumulated depreciation & & (2,000,000) & & (1,500,000) \\ \hline Long-term notes receivable & & 285,000 & & - \\ \hline Land & & 1,450,000 & & 1,450,000 \\ \hline Patent & & - & & - \\ \hline Non-current Assets & & 4,735,000 & & 4,950,000 \\ \hline Total Assets & $ & 6,891,366 & $ & 7,028,980 \\ \hline \multicolumn{5}{|l|}{ Liabilities } \\ \hline Accounts payable & $ & 450,000 & $ & 570,000 \\ \hline Wages payable & & 37,900 & & 33,000 \\ \hline Interest Payable & & - & & - \\ \hline Short-term Note Payable & & - & & - \\ \hline Deferred Revenue & & - & & - \\ \hline Dividends payable & & 155,000 & & 135,000 \\ \hline Current Liabilities & & 642,900 & & 738,000 \\ \hline Long-term notes payable & & 1,250,000 & & 1,250,000 \\ \hline Total Liabilities & & 1,892,900 & & 1,988,000 \\ \hline \multicolumn{5}{|l|}{ Stockholders' Equity } \\ \hline Common Stock & & 1,600,000 & & 1,600,000 \\ \hline Additional Paid-in-Capital & & 1,824,406 & & 1,824,406 \\ \hline Treasury Stock & & - & & - \\ \hline Retained earnings & & 1,574,060 & & 1,616,574 \\ \hline Total Stockholders' Equity & & 4,998,466 & & 5,040,980 \\ \hline Total Liabilities and Stockholders' Equity & $ & 6,891,366 & $ & 7,028,980 \\ \hline \end{tabular} HINT: Before booking an entry, remember to evaluate the substance of each transaction/event. Do accounting standards require the event or transaction to be booked into your company's accounting records? NOTE: All interest rates included in the transaction list are stated at an annual rate. January 1. On January 1 st, The Board of Directors issued 250,000 additional shares (par of $0.80 ) to raise capital for the New Year. Assume no change in price from December 31, 2021. 2. Purchased new office equipment for $92,000 with cash from California Furniture on January 1, 2022. The equipment will be depreciated over a ten-year period on a straight-line basis. The office equipment has an estimated salvage value of $6,000. [Adjusting Entry Required] 3. On January 1 st, a 5 year, $160,000 long-term note payable was taken from a local bank. The company plans on making a payment on this note at the end of the year. 4. On January 22nd the company purchased 8,500 units of inventory (garden gnomes) at a cost of $77 per unit. The company paid 45% in cash and purchased the remainder on account. 5. On January 25th the company paid $275,000 cash toward accounts payable. February 6. Paid cash for $43,500 worth of radio advertising on February 1 st. This gives the company radio advertising space until January 31st, 2023. [Adjusting Entry Required] 7. February 13th the company collects $372,000 of account payments from customers. March 8. Purchased a parcel of land on March 1,2022 for $950,000 by paying $490,000 in cash and signing a short-term note payable with the seller for $460,000. The company must repay the $460,000 in exactly one year on March 1,2023 . The company agreed to pay the seller 5 percent interest (annual rate) on a quarterly basis (June 1, September 1, December 1, 2022, and March 1, 2023). [Adjusting Entry Required] 9. On March 19th the company purchased $24,000 of office supplies from Super Office Supplies with cash. 4 10. On March 20th the company received a payment of $41,000 for 200 hours of service to be performed in the future. April 11. April 21 st, customers bought 15,000 garden gnomes for $148 per unit. The cost of goods sold is determined by the method of inventory valuation used by the company (Hint: Your company has beginning inventory). Customers paid the company 55% in cash and the remainder was on account. 12. On April 27nd the company purchased 9,250 units of inventory at a cost of $79 per unit. The company paid 70% in cash and purchased the remainder on account. 13. On April 29th the company paid $510,000 cash toward its accounts payable. May 14. On May 1 st the company paid all dividends owed to its owners. June 15. Leased additional warehouse space from Leasing Solutions for two years on June 1st due to expiration of the previous rental contract. $69,000 cash was paid for the new contract on this date which covers the rental fee for two years. There is no value left in the previous contract (Hint: the balance in prepaid rent at the beginning of the year has been "used" and should be recorded as an expense). [Adjusting Entry Required] 16. Wage expenses from January 1 - June 30$494,000. This was paid in full, including the beginning balance in wages payable. 17. On July 1 st, $134,000 of prepaid insurance was used. August 18. Purchased a Patent (Intangible Asset) for $76,000 on August 1 st with cash. The patent will be amortized over a 10 year period on a straight-line basis. [Adjusting Entry Required] 5 19. On August 6th, a piece of land that was originally purchased for $1,150,000 was sold for $1,240,000 cash. 20. August 15th, customers bought 9,000 garden gnomes at $148 per unit. The cost of goods sold is determined by the method of inventory valuation used by the company. Customers paid 45% in cash and the remainder was on account. 21. Received on August 25th a $129,000 cash payment from a customer paying on their account. September 22. On September 12th, a piece of equipment was sold for $510,000 cash. The equipment was originally purchased for $570,000. At the time of the sale, it had been depreciated by $70,000. October 23. The company's top sales officer met with a new customer to discuss a potential future contract. She informs the company that the customer is considering signing the $250,000 deal, which would become effective February 2023. 24. On October 1 st, the company purchased 11,250 units of inventory at a cost of $78.50 per unit. The purchase was made on account. 25. On October 10th, the company paid its supplier $98,000 cash for inventory that had been purchased on account. ovember 26. November 1st, the CEO, in an effort to adjust ratios, ordered the repurchasing of the company's own stock. The quantity of stock repurchased was 160,000 shares. 27. Purchased a two-year building insurance policy on November 1 st for $335,000 cash. [Adjusting Entry Required] 6 28. On November 17th a customer paid $561,000 for work that the company will finish in January of 2023. 29. November 19th, customers bought 8,650 garden gnomes at $148 per unit. The cost of goods sold is determined by the method of inventory valuation used by the company. Customers paid 45% in cash and the remainder was on account. BCOR 3010 Assignment 2 - The Accounting Cycle Version C You have been hired by Gnomeo, Inc., a company that buys and resells miniature garden gnomes. The company started business on January 1,2019 . The chief accountant has asked you to compile a set of financial statements that can be presented to current and potential investors. She hands you a list of transactions that need to be recorded in the accounting records before the financial statements for the year ended December 31, 2022, can be prepared. Your job is to record the transactions, adjusting entries, post all entries and prepare the financial statements - basically complete the accounting cycle. RECORD ENTRIES AND BUILD THE FINANCIAL STATEMENTS 1. Journal Entry List Record entries from the transaction and event list provided below in proper journal entry format. NOTE: You are recording entries for the fiscal year 2022 (Jan 1 - Dec 31). This list must be organized. Make sure that I can easily identify the journal entry or adjusting journal entry with the related transaction/event. Show your work if the entry requires you to make a calculation (i.e. depreciation, interest expense, etc.). 2. Chart of T-Accounts Create a chart of T-Accounts and post each journal entry to the appropriate accounts. 3. Financial Statements Build a multi-step income statement, a statement of retained earnings, and a classified balance sheet for the year ending December 31, 2022 (include all three years of data for 2022, 2021 and 2020 on all financial statements). Create a statement of cash flows for 2022 and 2021 using the indirect method for operating cash flows. SUBMIT THE FOLLOWING You will turn in a physical copy of your work in the following order: 1. A cover page with the names of the members of your group. 2. Financial Statements (in the following order): - Income Statement (2022,2021, and 2020) - Statement of Retained Earnings (2022, 2021, and 2020) - Balance Sheet (2022,2021, and 2020) - Statement of Cash Flows (2022 and 2021) 3. Include the following supporting documentation: Journal Entry List, Chart of TAccounts, and Inventory Tracking Schedule. IMPORTANT COMPANY INFORMATION Your company began operations on January 1, 2019. > The company's stock is traded on the NYSE. As of December 31, 2021 your company had 2,000,000 common shares outstanding with a par value of $0.80. > At the close of the market on December 31, 2022, your company's stock was trading at $5.10 per share. On November 1, 2022, the stock was trading at $3.30. At the end of 2021 the value of your stock was $3.70 per share. > Use the Cost Method for treatment of Treasury Stock. > Use the Allowance Method in accounting for Bad Debts, specifically the Percentage of Accounts Receivable Method. > The inventory valuation used by your company is FIFO (perpetual). > The company's inventory on January 1st, 2022 consists of 13,000 units. \begin{tabular}{|c|c|c|c|c|} \hline \multicolumn{5}{|c|}{ BALANCE SHEET } \\ \hline December 31, & & 2021 & & 2020 \\ \hline \multicolumn{5}{|l|}{ Assets } \\ \hline Cash & $ & 565,910 & $ & 658,079 \\ \hline Marketable securities & & 75,000 & & 30,000 \\ \hline Accounts receivable & & 455,000 & & 531,000 \\ \hline Allowance for Bad Debt & & (90,000) & & (105,000) \\ \hline Prepaid Advertising & & - & & - \\ \hline Prepaid Insurance & & 139,836 & & 149,519 \\ \hline Prepaid Rent & & 32,100 & & 34,982 \\ \hline Office supplies & & 3,520 & & 5,400 \\ \hline Inventory & & 975,000 & & 775,000 \\ \hline Current Assets & & 2,156,366 & & 2,078,980 \\ \hline Office Equipment & & - & & - \\ \hline Equipment & & 5,000,000 & & 5,000,000 \\ \hline Accumulated depreciation & & (2,000,000) & & (1,500,000) \\ \hline Long-term notes receivable & & 285,000 & & - \\ \hline Land & & 1,450,000 & & 1,450,000 \\ \hline Patent & & - & & - \\ \hline Non-current Assets & & 4,735,000 & & 4,950,000 \\ \hline Total Assets & $ & 6,891,366 & $ & 7,028,980 \\ \hline \multicolumn{5}{|l|}{ Liabilities } \\ \hline Accounts payable & $ & 450,000 & $ & 570,000 \\ \hline Wages payable & & 37,900 & & 33,000 \\ \hline Interest Payable & & - & & - \\ \hline Short-term Note Payable & & - & & - \\ \hline Deferred Revenue & & - & & - \\ \hline Dividends payable & & 155,000 & & 135,000 \\ \hline Current Liabilities & & 642,900 & & 738,000 \\ \hline Long-term notes payable & & 1,250,000 & & 1,250,000 \\ \hline Total Liabilities & & 1,892,900 & & 1,988,000 \\ \hline \multicolumn{5}{|l|}{ Stockholders' Equity } \\ \hline Common Stock & & 1,600,000 & & 1,600,000 \\ \hline Additional Paid-in-Capital & & 1,824,406 & & 1,824,406 \\ \hline Treasury Stock & & - & & - \\ \hline Retained earnings & & 1,574,060 & & 1,616,574 \\ \hline Total Stockholders' Equity & & 4,998,466 & & 5,040,980 \\ \hline Total Liabilities and Stockholders' Equity & $ & 6,891,366 & $ & 7,028,980 \\ \hline \end{tabular} HINT: Before booking an entry, remember to evaluate the substance of each transaction/event. Do accounting standards require the event or transaction to be booked into your company's accounting records? NOTE: All interest rates included in the transaction list are stated at an annual rate. January 1. On January 1 st, The Board of Directors issued 250,000 additional shares (par of $0.80 ) to raise capital for the New Year. Assume no change in price from December 31, 2021. 2. Purchased new office equipment for $92,000 with cash from California Furniture on January 1, 2022. The equipment will be depreciated over a ten-year period on a straight-line basis. The office equipment has an estimated salvage value of $6,000. [Adjusting Entry Required] 3. On January 1 st, a 5 year, $160,000 long-term note payable was taken from a local bank. The company plans on making a payment on this note at the end of the year. 4. On January 22nd the company purchased 8,500 units of inventory (garden gnomes) at a cost of $77 per unit. The company paid 45% in cash and purchased the remainder on account. 5. On January 25th the company paid $275,000 cash toward accounts payable. February 6. Paid cash for $43,500 worth of radio advertising on February 1 st. This gives the company radio advertising space until January 31st, 2023. [Adjusting Entry Required] 7. February 13th the company collects $372,000 of account payments from customers. March 8. Purchased a parcel of land on March 1,2022 for $950,000 by paying $490,000 in cash and signing a short-term note payable with the seller for $460,000. The company must repay the $460,000 in exactly one year on March 1,2023 . The company agreed to pay the seller 5 percent interest (annual rate) on a quarterly basis (June 1, September 1, December 1, 2022, and March 1, 2023). [Adjusting Entry Required] 9. On March 19th the company purchased $24,000 of office supplies from Super Office Supplies with cash. 4 10. On March 20th the company received a payment of $41,000 for 200 hours of service to be performed in the future. April 11. April 21 st, customers bought 15,000 garden gnomes for $148 per unit. The cost of goods sold is determined by the method of inventory valuation used by the company (Hint: Your company has beginning inventory). Customers paid the company 55% in cash and the remainder was on account. 12. On April 27nd the company purchased 9,250 units of inventory at a cost of $79 per unit. The company paid 70% in cash and purchased the remainder on account. 13. On April 29th the company paid $510,000 cash toward its accounts payable. May 14. On May 1 st the company paid all dividends owed to its owners. June 15. Leased additional warehouse space from Leasing Solutions for two years on June 1st due to expiration of the previous rental contract. $69,000 cash was paid for the new contract on this date which covers the rental fee for two years. There is no value left in the previous contract (Hint: the balance in prepaid rent at the beginning of the year has been "used" and should be recorded as an expense). [Adjusting Entry Required] 16. Wage expenses from January 1 - June 30$494,000. This was paid in full, including the beginning balance in wages payable. 17. On July 1 st, $134,000 of prepaid insurance was used. August 18. Purchased a Patent (Intangible Asset) for $76,000 on August 1 st with cash. The patent will be amortized over a 10 year period on a straight-line basis. [Adjusting Entry Required] 5 19. On August 6th, a piece of land that was originally purchased for $1,150,000 was sold for $1,240,000 cash. 20. August 15th, customers bought 9,000 garden gnomes at $148 per unit. The cost of goods sold is determined by the method of inventory valuation used by the company. Customers paid 45% in cash and the remainder was on account. 21. Received on August 25th a $129,000 cash payment from a customer paying on their account. September 22. On September 12th, a piece of equipment was sold for $510,000 cash. The equipment was originally purchased for $570,000. At the time of the sale, it had been depreciated by $70,000. October 23. The company's top sales officer met with a new customer to discuss a potential future contract. She informs the company that the customer is considering signing the $250,000 deal, which would become effective February 2023. 24. On October 1 st, the company purchased 11,250 units of inventory at a cost of $78.50 per unit. The purchase was made on account. 25. On October 10th, the company paid its supplier $98,000 cash for inventory that had been purchased on account. ovember 26. November 1st, the CEO, in an effort to adjust ratios, ordered the repurchasing of the company's own stock. The quantity of stock repurchased was 160,000 shares. 27. Purchased a two-year building insurance policy on November 1 st for $335,000 cash. [Adjusting Entry Required] 6 28. On November 17th a customer paid $561,000 for work that the company will finish in January of 2023. 29. November 19th, customers bought 8,650 garden gnomes at $148 per unit. The cost of goods sold is determined by the method of inventory valuation used by the company. Customers paid 45% in cash and the remainder was on account

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts