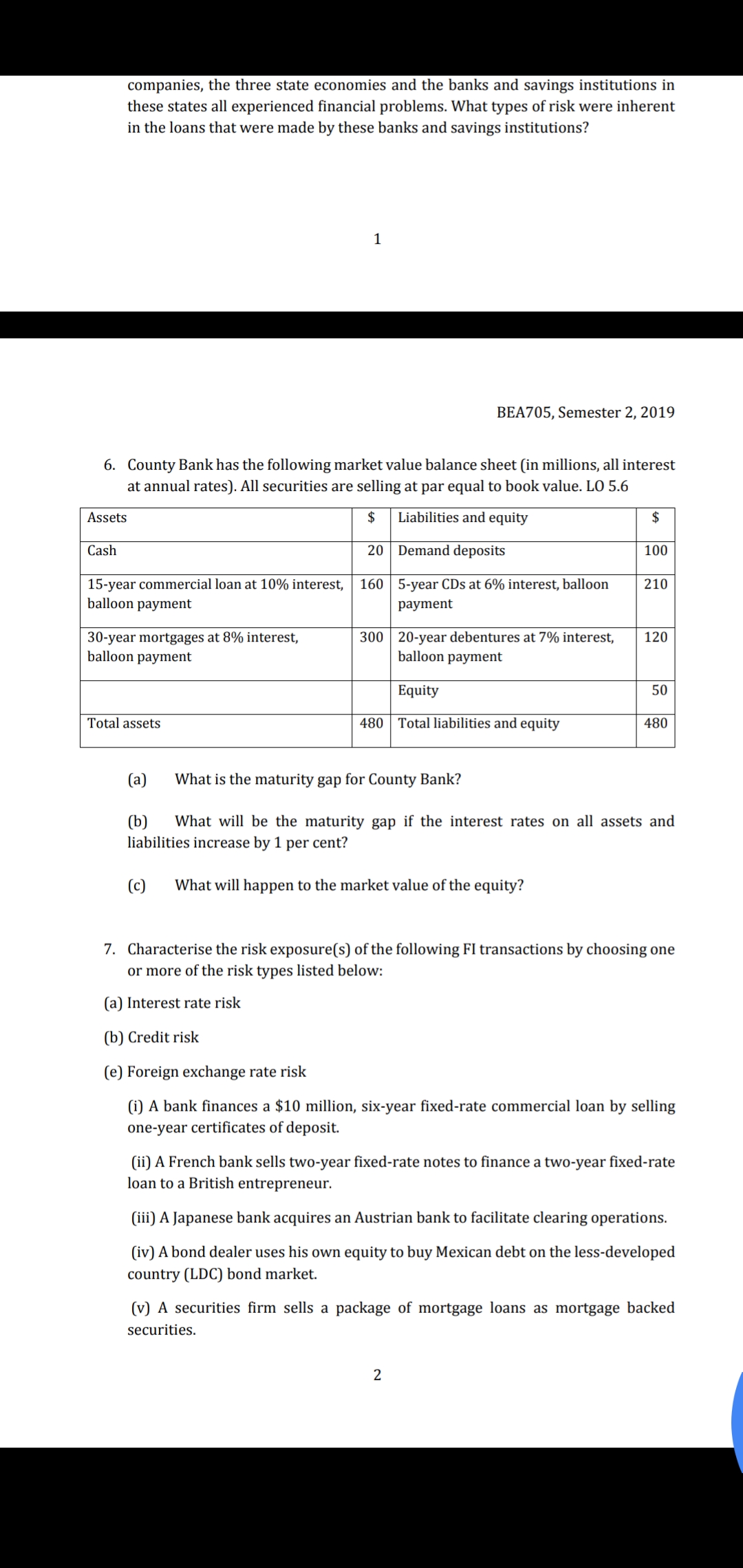

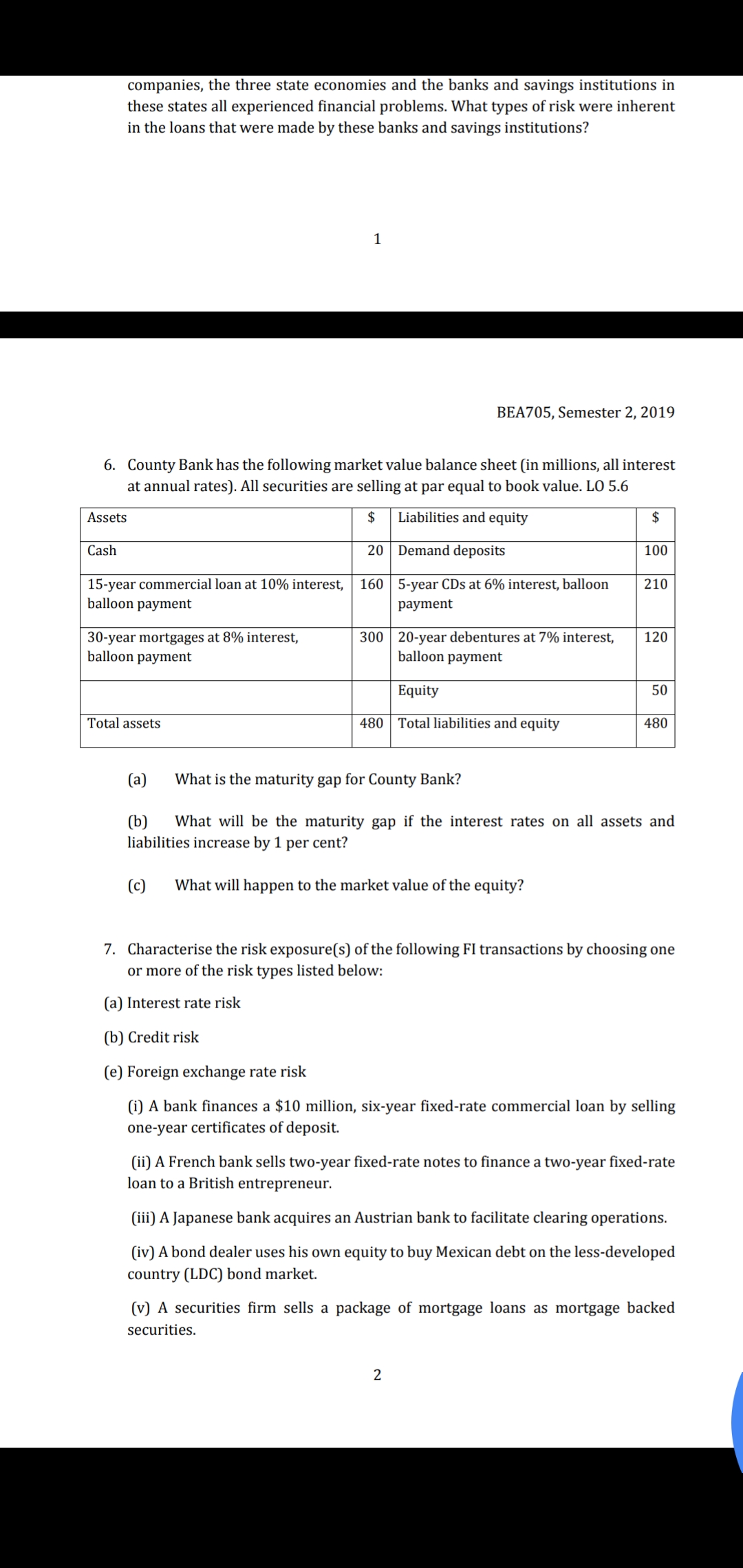

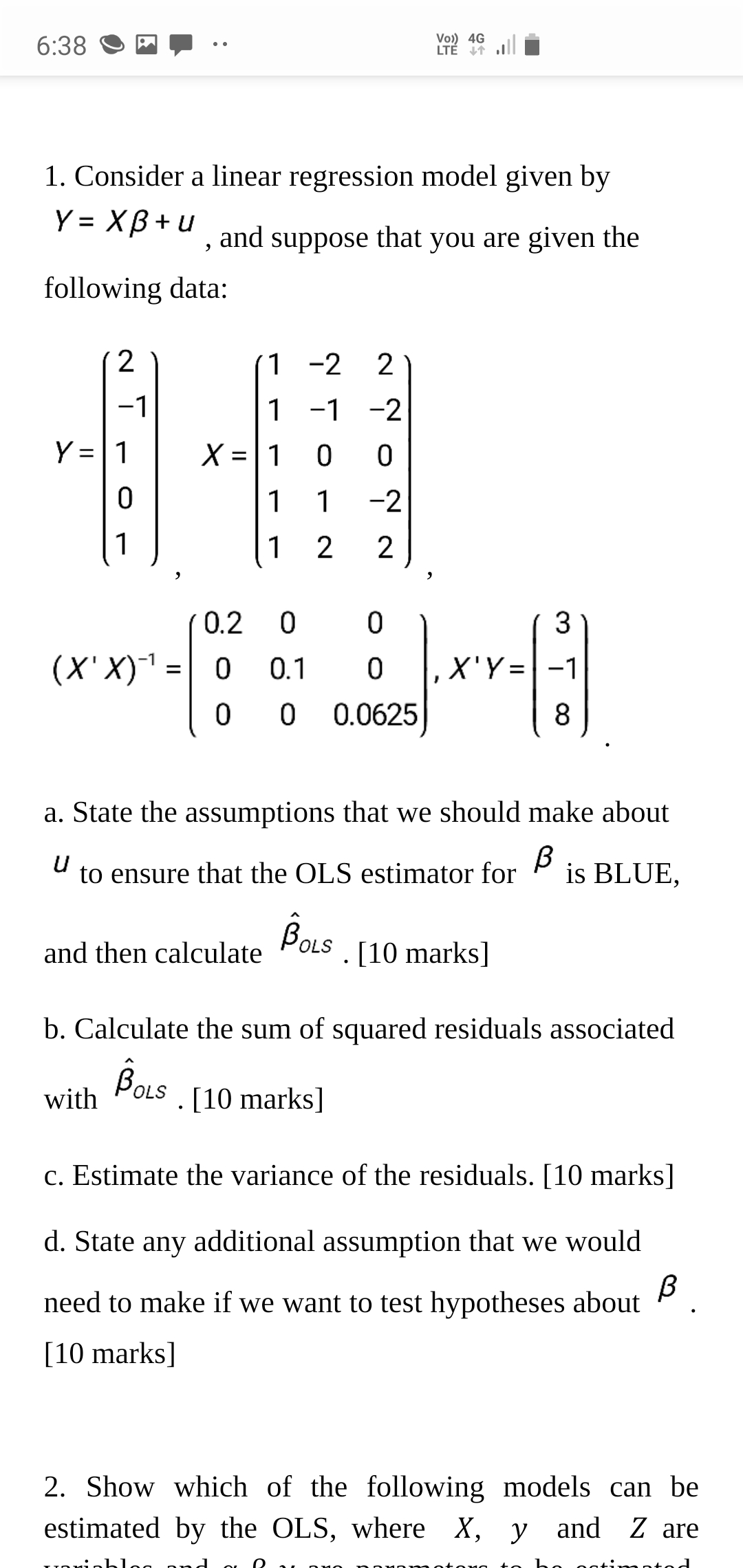

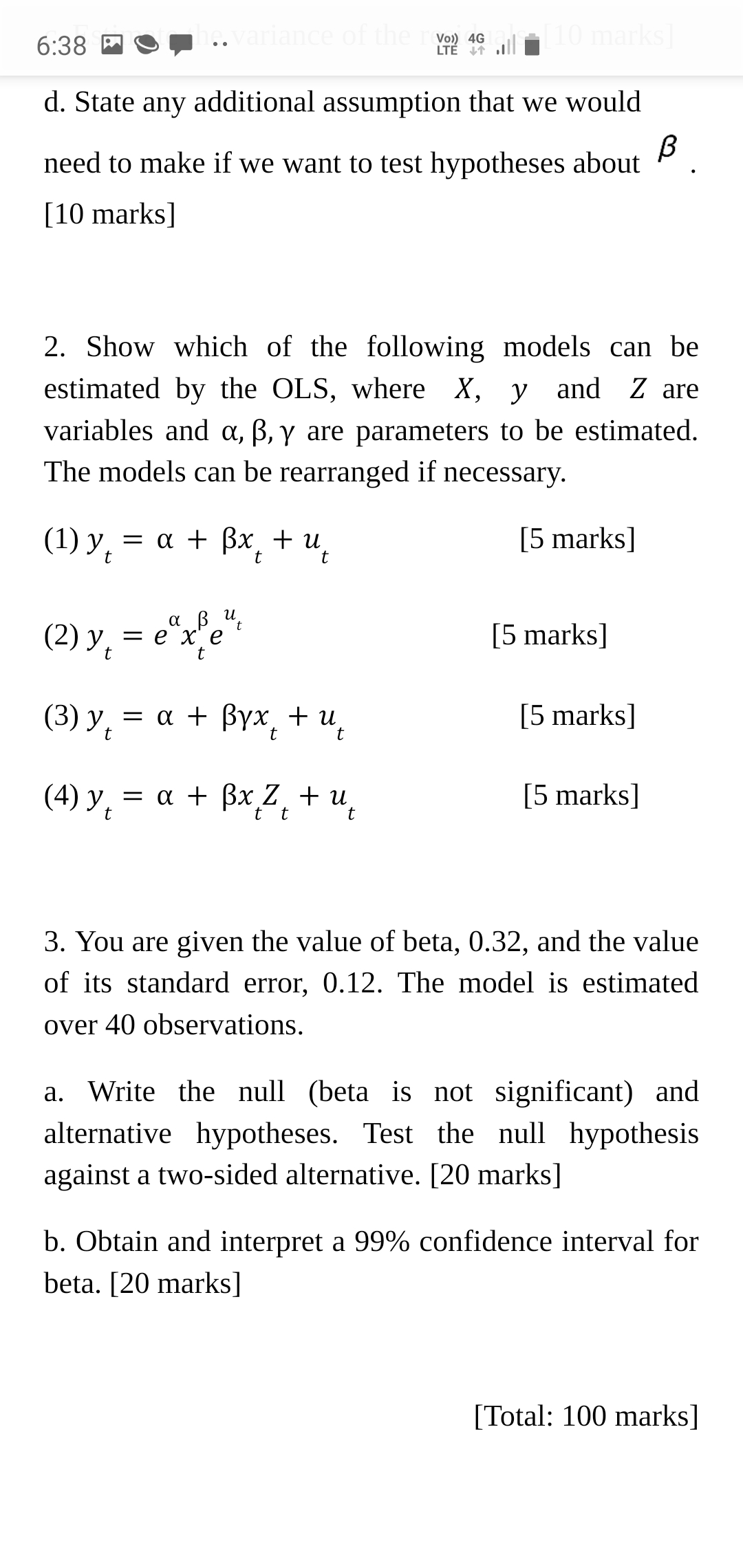

BEA705, Semester 2, 2019 BEA705 Workshop 2 W3 Problem Set 6. Two 10year bonds are being considered for an investment that may have to be liquidated before the maturity of the bonds. The rst bond is a 10-year premium bond with a coupon rate higher than its required rate of return and the second bond is a zero-coupon bond that pays only a lump-sum payment after 10 years with no interest over its life. Which bond would have more interest rate risk? That is, which bond's price would change by a larger amount for a given change in interest rates? Explain your answer. What is reinvestment risk? How is reinvestment risk part of interest rate risk? If an Fl funds short-term assets with long-term liabilities, what will be the impact on earnings of a decrease in the rate of interest? An increase in the rate of interest? Six months ago, Qualitybank Ltd issued a $100 million, one-year maturity CD denominated in euro [euro CD}. On the same date, $60 million was invested in a euro-denominated loan and A$40 million was invested in an Australian Treasury bond. The exchange rate on this date was 1.7382/A$1.Msume no repayment of principal and an exchange rate today of1.3905/A$1. (a) What is the current value of the euro CD principal (in M and Q? (b) What is the current value of Qualitybank's loan principal [in AS; and (=2)? [c] What is the current value of the Australian Treasury bill [in A$ and (=3)? (d) What is Qualitybank's prot/loss from this transaction [in A3 and )? A bank invested $50 million in a twoyear asset paying 10 per cent interest per annum and simultaneously issued a $50 million, one-year liability paying 8 per cent interest per annum. What will be the bank's net interest income each year if at the end of the rst year all interest rates have increased by 1 per cent (100 basis points]? ' Many US banks and savings institutions that failed in the 19805 had made loans to oil companies in Louisiana, Texas and Oklahoma. When oil prices fell, these companies. the three state economies and the banks and savings institutions in these states all experienced nancial problems. What types of risk were inherent in the loans that were made by these banks and savings institutions? BEA705, Semester 2, 2019 County Bank has the following market value balance sheet [in millions, all interest at annual rates]. All securities are selling at par equal to book value. L0 5.6 Bsets $ Liabilities and equity 5 Cash 20 Demand deposits 100 15-year commercial loan at 10% interest, 160 5-year CDs at 6% interest, balloon 210 balloon payment payment 30'year mortgages at 8% interest, 300 20Ayear debentures at 7% interest. 120 balloon payment balloon payment companies, the three state economies and the banks and savings institutions in these states all experienced nancial problems. What types of risk were inherent in the loans that were made by these banks and savings institutions? 1 6. BEA705, Semester 2, 2019 County Bank has the following market value balance sheet [in millions. all interest at annual rates]. All securities are selling at par equal to book value. L0 5.6 Msets $ Liabilities and equity $ Cash 20 Demand deposits 100 15-year commercial loan at 10% interest, 160 5-year CDs at 6% interest, balloon 210 7. (a) [b] (e) balloon payment payment 30-year mortgages at 8% interest, 300 20-year debentures at 7% interest, 120 balloon payment balloon payment 5 Total assets 4-80 480 (a) What is the maturity gap for County Bank? (b) What will be the maturity gap if the interest rates on all assets and liabilities increase by 1 per cent? [c] What will happen to the market value ofthe equity? Characterise the risk exposure[s) of the following Fl transactions by choosing one or more of the risk types listed below: interest rate risk Credit risk Foreign exchange rate risk [i] A bank nances a $10 million, six-year xed-rate commercial loan by selling one-year certicates ofdeposit (ii) A French hank sells two-year xed-rate notes to nance a two-year xed-rate loan to a British entrepreneur. [iii] A Japanese bank acquires an Austrian bank to facilitate clearing operations. [iv] A bond dealer uses his own equity to buy Mexican debt on the lessdeveloped country (LDC) bond market. (v) A securities rm sells a package of mortgage loans as mortgage backed securities. 6:38 9) IE . ' '1'?' '1? .l" I 1. Consider a linear regression model given by Y: X + u , and suppose that you are given the following data: 2 1 2 2 1 1 1 2 Y: 1 X: 1 0 0 0 1 1 2 1 1 2 2 0.2 0 o 3 (X'X)"'= 0 0.1 o ,X'Y= 1 o 0 0.0625 8 a. State the assumptions that we should make about u to ensure that the OLS estimator for B is BLUE, and then calculate 30" . [10 marks] b. Calculate the sum of squared residuals associated with 3'" . [10 marks] c. Estimate the variance of the residuals. [10 marks] d. State any additional assumption that we would 13 need to make if we want to test hypotheses about . [10 marks] 2. Show which of the following models can be estimated by the OLS, where X, y and Z are -vnuinL'lnn r._.'l n. D -- nun _.-._..-.__....a...__.-. a... 1" nnLlnLnJ 6:38 Ii 9 . ' '3' '1? .l" i d. State any additional assumption that we would i8 need to make if we want to test hypotheses about . [10 marks] 2. Show which of the following models can be estimated by the OLS, where X, y and Z are variables and a, [3,y are parameters to be estimated. The models can be rearranged if necessary. (1) yt = a + th + at [5 marks] (2) yt = eaxfeut [5 marks] (3) yt = 0i + BYxt + ut [5 marks] (4) yt = 01 + thzt + u: [5 marks] 3. You are given the value of beta, 0.32, and the value of its standard error, 0.12. The model is estimated over 40 observations. a. Write the null (beta is not significant) and alternative hypotheses. Test the null hypothesis against a two-sided alternative. [20 marks] b. Obtain and interpret a 99% confidence interval for beta. [20 marks] [Total: 100 marks]