Answered step by step

Verified Expert Solution

Question

1 Approved Answer

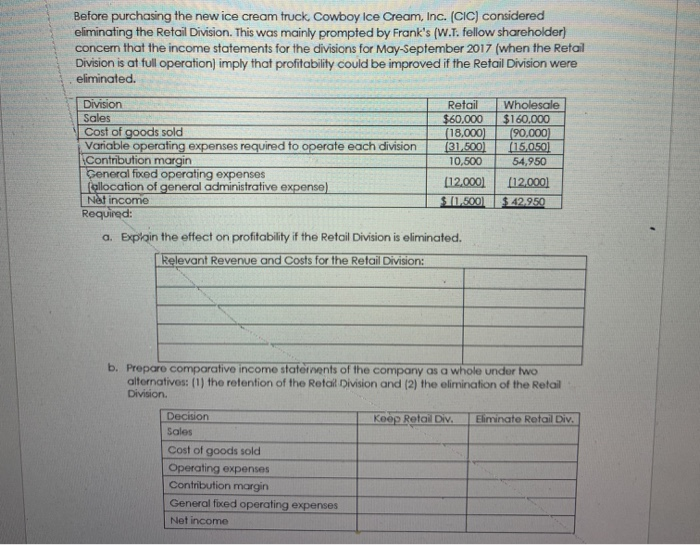

Before purchasing the new ice cream truck, Cowboy Ice Cream, Inc. (CIC) considered eliminating the Retail Division. This was mainly prompted by Frank's (W.T. fellow

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Cybersecurity Body Of Knowledge The ACM IEEE AIS IFIP Recommendations For A Complete Curriculum In Cybersecurity Internal Audit And IT Audit

Authors: Daniel Shoemaker, Anne Kohnke, Ken Sigler

1st Edition

1032400218, 978-1032400211