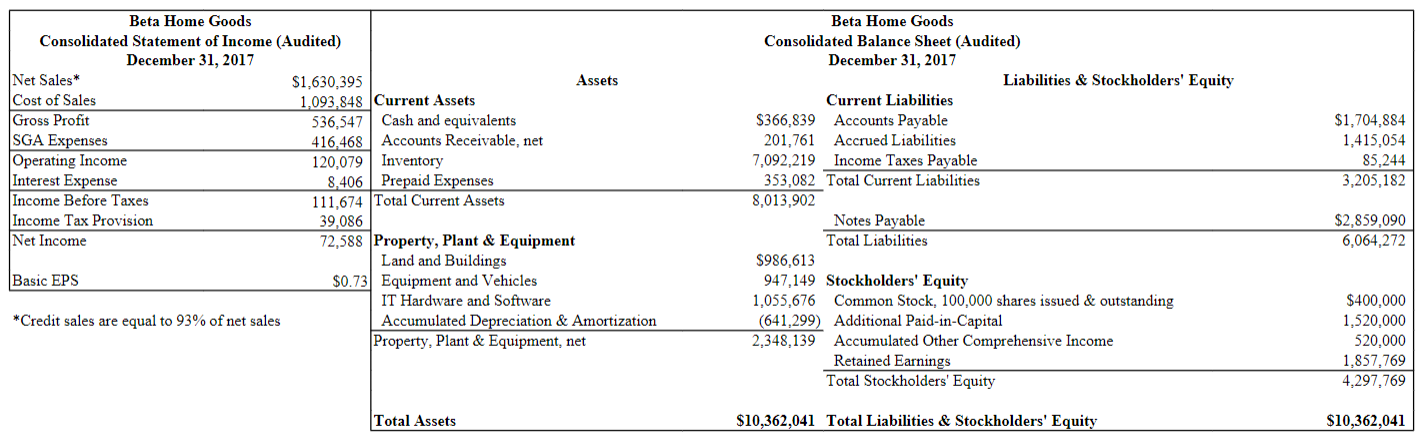

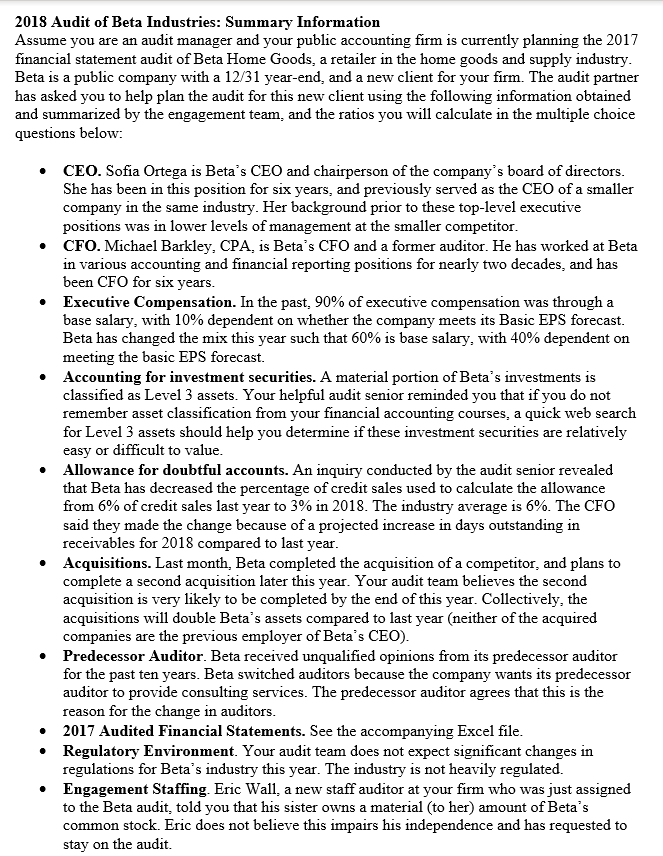

Beta Home Goods Consolidated Statement of Income (Audited) December 31, 2017 Net Sales* $1,630,395 Assets Cost of Sales 1,093,848 Current Assets Gross Profit 536,547 Cash and equivalents SGA Expenses 416,468 Accounts Receivable, net Operating Income 120,079 Inventory Interest Expense 8,406 Prepaid Expenses Income Before Taxes 111,674 Total Current Assets Income Tax Provision 39,086 Net Income 72,588 Property, Plant & Equipment Land and Buildings Basic EPS $0.73 Equipment and Vehicles IT Hardware and Software *Credit sales are equal to 93% of net sales Accumulated Depreciation & Amortization Property, Plant & Equipment, net $1,704,884 1,415,054 85,244 3,205,182 Beta Home Goods Consolidated Balance Sheet (Audited) December 31, 2017 Liabilities & Stockholders' Equity Current Liabilities $366,839 Accounts Payable 201,761 Accrued Liabilities 7,092,219 Income Taxes Payable 353,082 Total Current Liabilities 8,013,902 Notes Payable Total Liabilities $986,613 947,149 Stockholders' Equity 1,055,676 Common Stock, 100,000 shares issued & outstanding (641,299) Additional Paid-in-Capital 2.348,139 Accumulated Other Comprehensive Income Retained Earnings Total Stockholders' Equity $2,859,090 6,064,272 $400,000 1,520,000 520,000 1,857,769 4,297,769 Total Assets $10,362,041 Total Liabilities & Stockholders' Equity $10,362,041 | 2018 Audit of Beta Industries: Summary Information Assume you are an audit manager and your public accounting firm is currently planning the 2017 financial statement audit of Beta Home Goods, a retailer in the home goods and supply industry. Beta is a public company with a 12/31 year-end, and a new client for your firm. The audit partner has asked you to help plan the audit for this new client using the following information obtained and summarized by the engagement team, and the ratios you will calculate in the multiple choice questions below: CEO. Sofia Ortega is Beta's CEO and chairperson of the company's board of directors. She has been in this position for six years, and previously served as the CEO of a smaller company in the same industry. Her background prior to these top-level executive positions was in lower levels of management at the smaller competitor. CFO. Michael Barkley, CPA, is Beta's CFO and a former auditor. He has worked at Beta in various accounting and financial reporting positions for nearly two decades, and has been CFO for six years. Executive Compensation. In the past, 90% of executive compensation was through a base salary, with 10% dependent on whether the company meets its Basic EPS forecast. Beta has changed the mix this year such that 60% is base salary, with 40% dependent on meeting the basic EPS forecast. Accounting for investment securities. A material portion of Beta's investments is classified as Level 3 assets. Your helpful audit senior reminded you that if you do not remember asset classification from your financial accounting courses, a quick web search for Level 3 assets should help you determine if these investment securities are relatively easy or difficult to value. Allowance for doubtful accounts. An inquiry conducted by the audit senior revealed that Beta has decreased the percentage of credit sales used to calculate the allowance from 6% of credit sales last year to 3% in 2018. The industry average is 6%. The CFO said they made the change because of a projected increase in days outstanding in receivables for 2018 compared to last year. Acquisitions. Last month, Beta completed the acquisition of a competitor, and plans to complete a second acquisition later this year. Your audit team believes the second acquisition is very likely to be completed by the end of this year. Collectively, the acquisitions will double Beta's assets compared to last year (neither of the acquired companies are the previous employer of Beta's CEO). Predecessor Auditor. Beta received unqualified opinions from its predecessor auditor for the past ten years. Beta switched auditors because the company wants its predecessor auditor to provide consulting services. The predecessor auditor agrees that this is the reason for the change in auditors. 2017 Audited Financial Statements. See the accompanying Excel file. Regulatory Environment. Your audit team does not expect significant changes in regulations for Beta's industry this year. The industry is not heavily regulated. Engagement Staffing. Eric Wall, a new staff auditor at your firm who was just assigned to the Beta audit, told you that his sister owns a material (to her) amount of Beta's common stock. Eric does not believe this impairs his independence and has requested to stay on the audit. 1. An auditor calculating Beta's quick ratio should exclude which of the following item(s) from current assets? a. Cash and equivalents b. Inventory c. Prepaid Expenses d. B & C only 2. The numerator of Beta's receivables turnover is equal to a. Eighty-seven percent of Beta's cost of sales b. Eighty-seven percent of Beta's net sales c. Ninety-three percent of Beta's cost of sales d. Ninety-three percent of Beta's net sales 3. An auditor calculating Beta's inventory turnover should include which financial statement item in the denominator? a. Cost of goods sold b. Inventory c. Sales d. Total current assets 4. An auditor calculating Beta's current ratio should include which financial statement item in the numerator? a. Current assets b. Current liabilities c. Interest expense d. Long-term debt 5. Assuming a 365 day year, Beta's days outstanding in accounts receivables is ___ days. a. 47.90 b. 48.57 c. 61.55 6. Beta's quick ratio is_% a. 0.18 b. 0.30 c. 2.72 7. Beta's return on equity (ROE) is __%. a. 0.70 b. 1.69 c. 1.84 8. Beta's profit margin is __%. a. 2.50 b. 4.45 c. 32.91 9. Assume Beta's usual credit terms are 2/10, net 30. Beta's days outstanding in accounts receivables suggests bad debts are likely_ to accounts receivable. a. Immaterial b. Material c. Neither A nor B: Bad debts have no relationship with accounts receivable 10. Beta's profit margin, relative to the industry of average of 12%, suggests a _ level of detection risk. a. Low b. High c. Neither A nor B: profit margin is irrelevant to detection risk 11. Beta's ROA, relative to the industry average of 4%, suggests a _ level of inherent risk. a. Low b. High c. Neither A nor B: ROA is irrelevant to assessing inherent risk 12. Beta's current ratio may be distorted because the company a. Has not fully depreciated and amortized all of its fixed assets b. Did not present diluted EPS in its financial statements c. Likely has a high level of bad debts 13. List four issues from the summary information on p.2 that could impact IR at Beta 14. Summarize the information from the predecessor auditor. How does this information impact overall IR? Explain your answer. 15. What is your assessment of inherent risk for Beta's allowance for doubtful accounts (low moderate, or high)? Explain your answer. 16. What is your overall IR assessment (low, moderate, or high)? Support your conclusion using the summary information in this document and the 2017 financial statements, including the analytical procedures you performed in Part 1. 17. Describe your responsibility to the public interest in considering Eric's issue? How does this responsibility impact your consideration of whether to remove him from the Beta audit? 18. Will you allow Eric to serve on the Beta audit? Explain your reasoning, including how investors and regulators might view his participation on the audit. 19. Assume an auditor in Eric's position were allowed to stay on the Beta audit. Could this person be objective (be sure to explain your answer)? What specific advice would you give this person on how to maintain her/his objectivity