Answered step by step

Verified Expert Solution

Question

1 Approved Answer

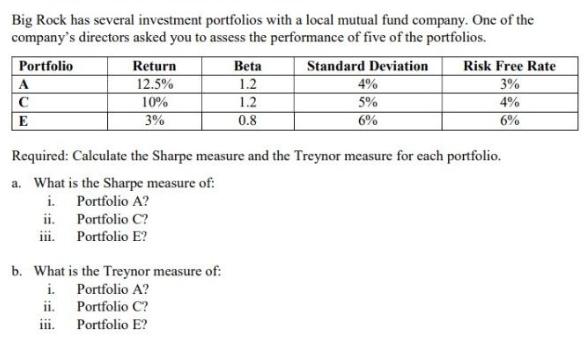

Big Rock has several investment portfolios with a local mutual fund company. One of the company's directors asked you to assess the performance of

Big Rock has several investment portfolios with a local mutual fund company. One of the company's directors asked you to assess the performance of five of the portfolios. Portfolio Beta Standard Deviation Risk Free Rate Return 12.5% A 1.2 4% 3% 10% 1.2 5% 4% E 3% 0.8 6% 6% Required: Calculate the Sharpe measure and the Treynor measure for each portfolio. a. What is the Sharpe measure of: i. Portfolio A? ii. Portfolio C? iii. Portfolio E? b. What is the Treynor measure of: i. Portfolio A? ii. Portfolio C? Portfolio E?

Step by Step Solution

★★★★★

3.36 Rating (149 Votes )

There are 3 Steps involved in it

Step: 1

Sharpe Measure Formula Return on portfolioRisk free rateSt...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Principles

Authors: Jerry J. Weygandt, Donald E. Kieso, Paul D. Kimmel, Barbara Trenholm, Valerie Warren, Lori Novak

7th Canadian Edition Volume 1

1119048508, 978-1119048503