Question

Blank 1 options: $0 , $50,000 , $100,000 , or $135,947 Blank 2 options: are not covered by his policy , are covered under Part

Blank 1 options: $0 , $50,000 , $100,000 , or $135,947

Blank 2 options: are not covered by his policy, are covered under Part C, or are covered under Part A

Blank 3 options: $20,000 , $30,000 , or $50,000

Blank 4 options: $0 , $25,907 , or $29,707

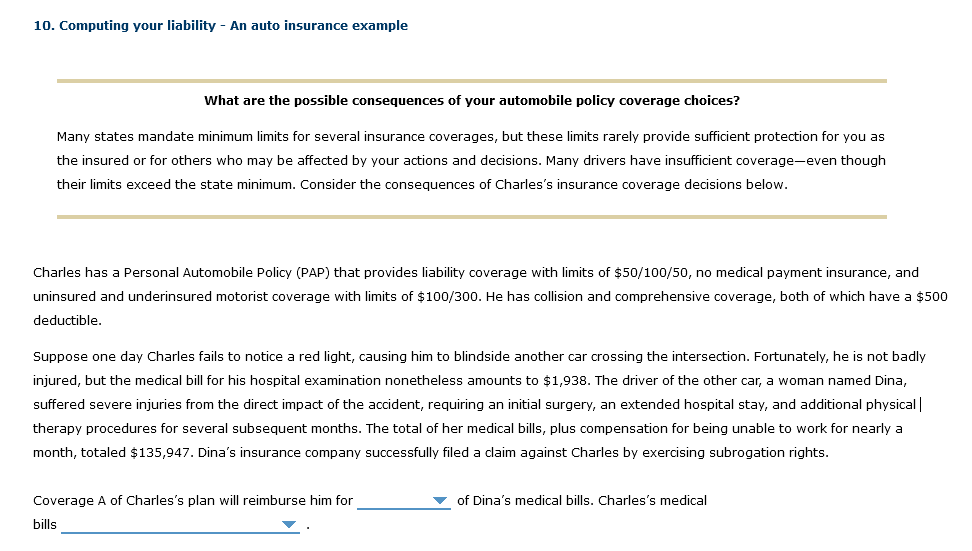

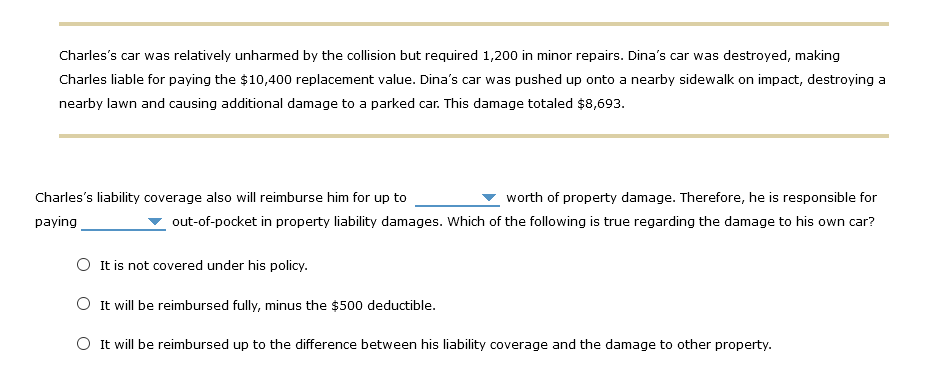

10. Computing your liability - An auto insurance example What are the possible consequences of your automobile policy coverage choices? Many states mandate minimum limits for several insurance coverages, but these limits rarely provide sufficient protection for you as the insured or for others who may be affected by your actions and decisions. Many drivers have insufficient coverage-even though their limits exceed the state minimum. Consider the consequences of Charles's insurance coverage decisions below. Charles has a Personal Automobile Policy (PAP) that provides liability coverage with limits of $50/100/50, no medical payment insurance, and uninsured and underinsured motorist coverage with limits of $100/300. He has collision and comprehensive coverage, both of which have a $500 deductible. Suppose one day Charles fails to notice a red light, causing him to blindside another car crossing the intersection. Fortunately, he is not badly injured, but the medical bill for his hospital examination nonetheless amounts to $1,938. The driver of the other car, a woman named Dina, suffered severe injuries from the direct impact of the accident, requiring an initial surgery, an extended hospital stay, and additional physical | therapy procedures for several subsequent months. The total of her medical bills, plus compensation for being unable to work for nearly a month, totaled $135,947. Dina's insurance company successfully filed a claim against Charles by exercising subrogation rights. of Dina's medical bills. Charles's medical Coverage A of Charles's plan will reimburse him for bills Charles's car was relatively unharmed by the collision but required 1,200 in minor repairs. Dina's car was destroyed, making Charles liable for paying the $10,400 replacement value. Dina's car was pushed up onto a nearby sidewalk on impact, destroying a nearby lawn and causing additional damage to a parked car. This damage totaled $8,693. Charles's liability coverage also will reimburse him for up to worth of property damage. Therefore, he is responsible for paying out-of-pocket in property liability damages. Which of the following is true regarding the damage to his own car? It is not covered under his policy. It will be reimbursed fully, minus the $500 deductible. It will be reimbursed up to the difference between his liability coverage and the damage to other property. 10. Computing your liability - An auto insurance example What are the possible consequences of your automobile policy coverage choices? Many states mandate minimum limits for several insurance coverages, but these limits rarely provide sufficient protection for you as the insured or for others who may be affected by your actions and decisions. Many drivers have insufficient coverage-even though their limits exceed the state minimum. Consider the consequences of Charles's insurance coverage decisions below. Charles has a Personal Automobile Policy (PAP) that provides liability coverage with limits of $50/100/50, no medical payment insurance, and uninsured and underinsured motorist coverage with limits of $100/300. He has collision and comprehensive coverage, both of which have a $500 deductible. Suppose one day Charles fails to notice a red light, causing him to blindside another car crossing the intersection. Fortunately, he is not badly injured, but the medical bill for his hospital examination nonetheless amounts to $1,938. The driver of the other car, a woman named Dina, suffered severe injuries from the direct impact of the accident, requiring an initial surgery, an extended hospital stay, and additional physical | therapy procedures for several subsequent months. The total of her medical bills, plus compensation for being unable to work for nearly a month, totaled $135,947. Dina's insurance company successfully filed a claim against Charles by exercising subrogation rights. of Dina's medical bills. Charles's medical Coverage A of Charles's plan will reimburse him for bills Charles's car was relatively unharmed by the collision but required 1,200 in minor repairs. Dina's car was destroyed, making Charles liable for paying the $10,400 replacement value. Dina's car was pushed up onto a nearby sidewalk on impact, destroying a nearby lawn and causing additional damage to a parked car. This damage totaled $8,693. Charles's liability coverage also will reimburse him for up to worth of property damage. Therefore, he is responsible for paying out-of-pocket in property liability damages. Which of the following is true regarding the damage to his own car? It is not covered under his policy. It will be reimbursed fully, minus the $500 deductible. It will be reimbursed up to the difference between his liability coverage and the damage to other propertyStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Money Banking And Financial Markets

Authors: Stephen G. Cecchetti

2nd International Edition

0071287728, 9780071287722