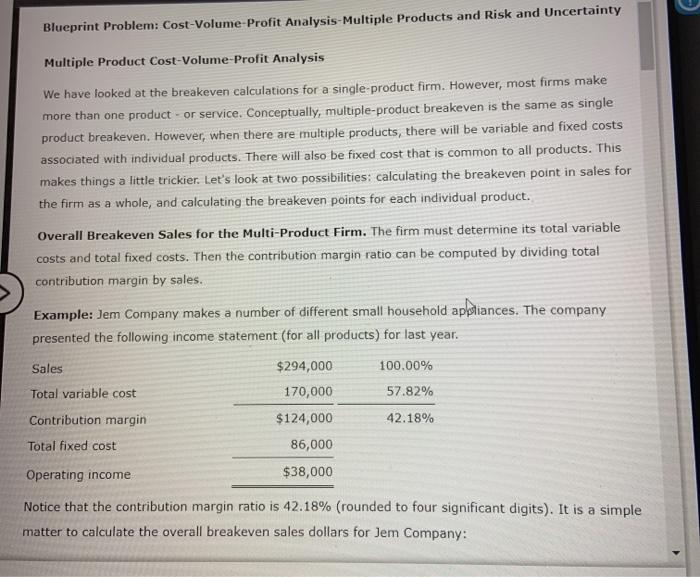

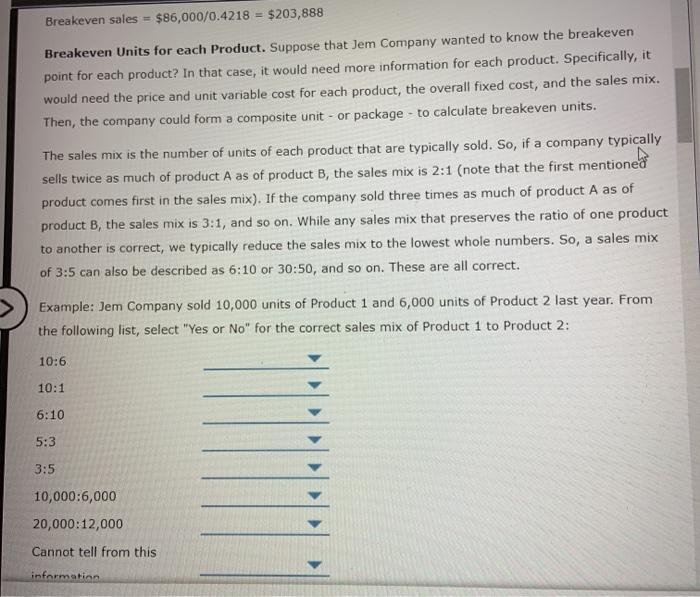

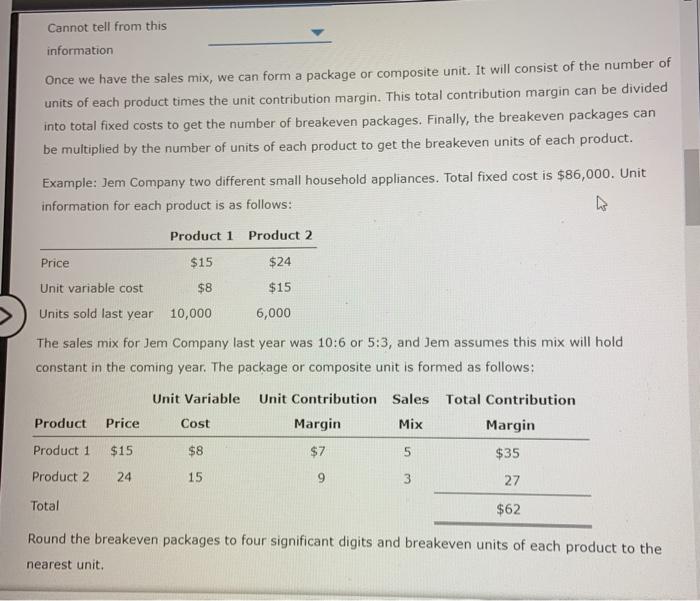

Blueprint Problem: Cost-Volume Profit Analysis Multiple Products and Risk and Uncertainty Multiple Product Cost-Volume-Profit Analysis We have looked at the breakeven calculations for a single-product firm. However, most firms make more than one product or service. Conceptually, multiple-product breakeven is the same as single product breakeven. However, when there are multiple products, there will be variable and fixed costs associated with individual products. There will also be fixed cost that is common to all products. This makes things a little trickier. Let's look at two possibilities: calculating the breakeven point in sales for the firm as a whole, and calculating the breakeven points for each individual product. Overall Breakeven Sales for the Multi-Product Firm. The firm must determine its total variable costs and total fixed costs. Then the contribution margin ratio can be computed by dividing total contribution margin by sales. Example: Jem Company makes a number of different small household appliances. The company presented the following income statement (for all products) for last year. Sales 100.00% 57.82% Total variable cost Contribution margin Total fixed cost $294,000 170,000 $124,000 86,000 42.18% Operating income $38,000 Notice that the contribution margin ratio is 42.18% (rounded to four significant digits). It is a simple matter to calculate the overall breakeven sales dollars for Jem Company: Breakeven sales $86,000/0.4218 = $203,888 Breakeven Units for each Product. Suppose that Jem Company wanted to know the breakeven point for each product? In that case, it would need more information for each product. Specifically, it would need the price and unit variable cost for each product, the overall fixed cost, and the sales mix. Then, the company could form a composite unit - or package - to calculate breakeven units. The sales mix is the number of units of each product that are typically sold. So, if a company typically sells twice as much of product A as of product B, the sales mix is 2:1 (note that the first mentioned product comes first in the sales mix). If the company sold three times as much of product A as of product B, the sales mix is 3:1, and so on. While any sales mix that preserves the ratio of one product to another is correct, we typically reduce the sales mix to the lowest whole numbers. So, a sales mix of 3:5 can also be described as 6:10 or 30:50, and so on. These are all correct. Example: Jem Company sold 10,000 units of Product 1 and 6,000 units of Product 2 last year. From the following list, select "Yes or No" for the correct sales mix of Product 1 to Product 2: 10:6 10:1 6:10 5:3 3:5 10,000:6,000 20,000:12,000 Cannot tell from this information Cannot tell from this information Once we have the sales mix, we can form a package or composite unit. It will consist of the number of units of each product times the unit contribution margin. This total contribution margin can be divided into total fixed costs to get the number of breakeven packages. Finally, the breakeven packages can be multiplied by the number of units of each product to get the breakeven units of each product. Example: Jem Company two different small household appliances. Total fixed cost is $86,000. Unit information for each product is as follows: Product 1 Product 2 Price $15 $24 Unit variable cost $8 $15 Units sold last year 10,000 6,000 The sales mix for Jem Company last year was 10:6 or 5:3, and Jem assumes this mix will hold constant in the coming year. The package or composite unit is formed as follows: Unit Variable Product Price Cost Unit Contribution Sales Total Contribution Margin Mix Margin $7 5 $35 Product 1 $15 $8 Product 2 24 15 9 3 27 Total $62 Round the breakeven packages to four significant digits and breakeven units of each product to the nearest unit. Round the breakeven packages to four significant digits and breakeven units of each product to the nearest unit Breakeven packages - $86,000/$62 - 1,387.0968 Breakeven units Product 1 = 1,387,0968 x 5 = 6,935 Breakeven units Product 2 = 1,387.0968 3 - 4,161 Notice that we did not round the breakeven packages. This is because Jem Company is not selling packages, and the total number of packages will be multiplied by the number of units of each product in the package. However, we did round the breakeven units of each product to the nearest unit (you cannot sell a part of a unit). Let's prepare an income statement to show that these breakeven units do result in zero profit. > Product Product 1 Product 2 Total Sales $104,025 $99,864 $203,889 Total variable cost 55,480 62,415 117,895 Contribution margin $48,545 $37,449 $85,994 Total fixed cost 86,000 Operating income $(6) The operating income is very close to zero due to rounding error in computing the breakeven packages and units. Notice that the total sales revenue at breakeven is virtually identical to that computed using the contribution margin ratio on the total fixed cost from the original example income statement