Question

Bond #1: US Treasury note with a 2% coupon due in 5 years issued at a price of par ($100). Bond #2: ABC Corp note

Bond #1: US Treasury note with a 2% coupon due in 5 years issued at a price of par ($100).

Bond #2: ABC Corp note with a 4% coupon issued at a yield to maturity of 4.2%.

ABC's credit is rated BBB.

? Both bonds were issued and will mature on the same date.

? Coupons on both bonds are stated in annual terms above, but paid semi-annually.

? The Fed Funds rate is 0.75%. ? Below is the "benchmark" US Treasury "on-the-run" Yield Curve on date of issuance:

1y 1.00% 2y 1.25% 3y 1.50% 5y 2.00% 7y 2.50% 10y 3.00%

1. What is the Yield to Maturity of Bond #1?

2. Was Bond #2 issued (sold) at a par, premium or discount price? (You can answer this without knowing the specific price.)

3. What do bond market participants call the "difference" between the yields to maturity of Bond #2 and Bond #1?

4. What type of risk is most likely the largest component of this "yield difference?"

1. 2%

2. Discount price

3. Spread

4. Default Risk

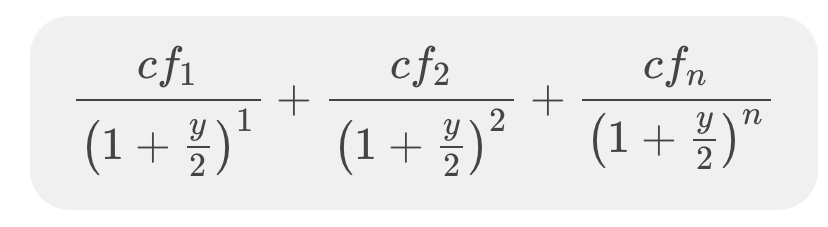

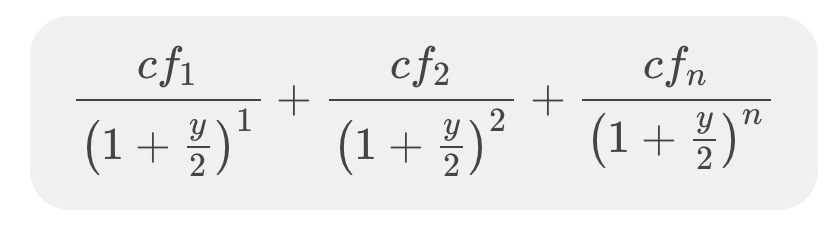

Use the Present Value of Cash Flows Model (see format below) to compute the following prices (express all calculated prices in terms of $100.00 with 2 decimals (: Also see Bond Pricing Framework at end of document (and Excel File).

a. Price of Bond #2 using yield and bond characteristics provided above (show your work.

b. Holding all other factors constant, compute the new price of Bond #2 if the Fed announced an increase the Fed Funds target rate of 1% and all other treasury yields immediately moved by the same amount (show your work).

c. Holding all other factors constant, calculate the new price of Bond #2 if ABC's credit rating increased to "A" and the current difference between yields of notes rated "A" and "BBB" (Bond #2's previous rating) was 135 basis points* (show your work):

*1 basis point = 0.01%

PRICE=

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduces Quantitative Finance

Authors: Paul Wilmott

2nd edition

470319585, 470319581, 978-0470319581