Answered step by step

Verified Expert Solution

Question

1 Approved Answer

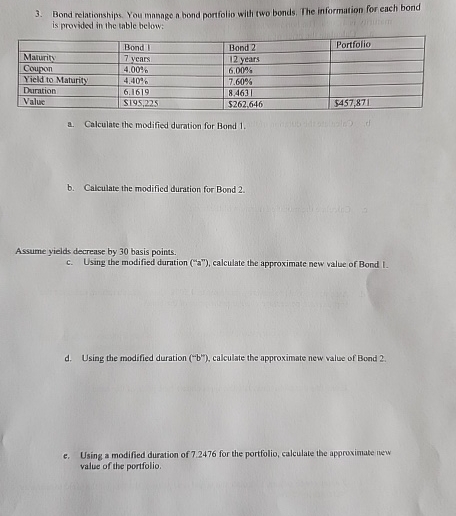

Bond relationships. You manage a bond portfolio with two bonds. The information for each bond is providest in the table below: table [ [

Bond relationships. You manage a bond portfolio with two bonds. The information for each bond is providest in the table below:

tableBond I,Bond PortfolioMaturity years, years,CouponYield to Maturity,DurationValue$$

a Calculate the modified duration for Bond

b Calculate the modificd duration for Bond

Assume yields decrease by basis points.

c Using the modified duration a calculate the approximate new value of Bond I.

d Using the modified duration b calculate the approximate new value of Bond

e Using a modified duration of for the portfolio, calculate the approximate new value of the portfolio.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Agricultural Finance

Authors: Charles Moss

1st Edition

0415599075, 978-0415599078