Answered step by step

Verified Expert Solution

Question

1 Approved Answer

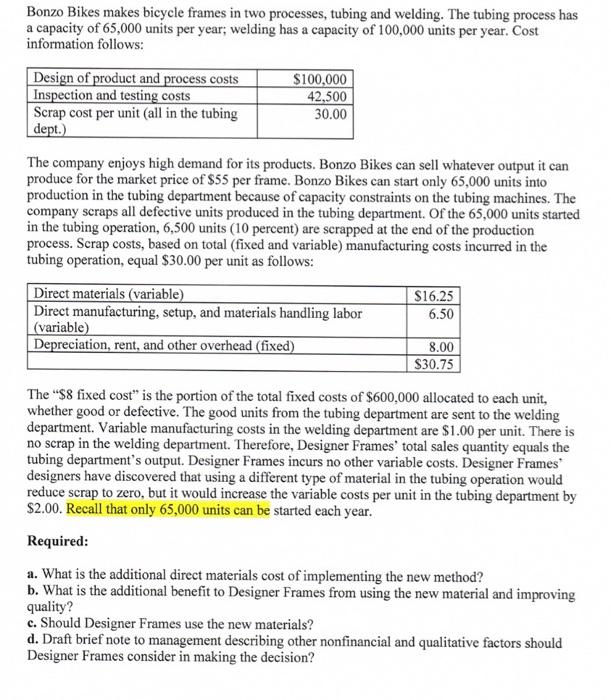

Bonzo Bikes makes bicycle frames in two processes, tubing and welding. The tubing process has a capacity of 65,000 units per year; welding has a

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Boundaries In Financial And Non-Financial Reporting A Comparative Analysis Of Their Constitutive Role

Authors: Laura Girella

1st Edition

1138586900, 9781138586901