Answered step by step

Verified Expert Solution

Question

1 Approved Answer

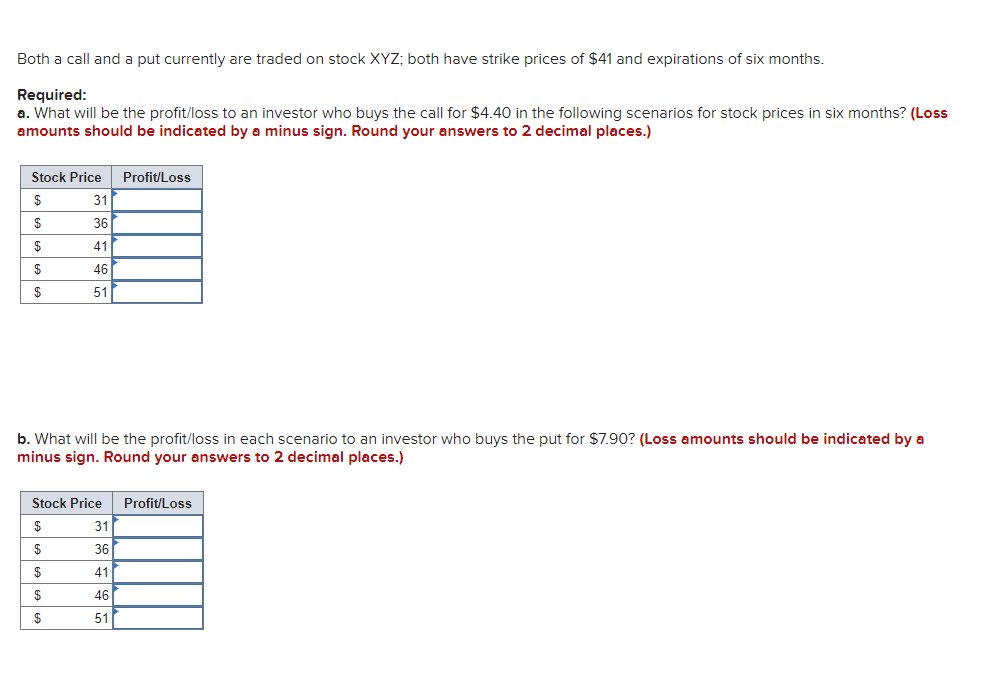

Both a call and a put currently are traded on stock XYZ; both have strike prices of $41 and expirations of six months. Required: a.

Both a call and a put currently are traded on stock XYZ; both have strike prices of $41 and expirations of six months. Required: a. What will be the profit/loss to an investor who buys the call for $4.40 in the following scenarios for stock prices in six months? (Loss amounts should be indicated by a minus sign. Round your answers to 2 decimal places.) b. What will be the profit/loss in each scenario to an investor who buys the put for $7.90 ? (Loss amounts should be indicated by a minus sign. Round your answers to 2 decimal places.)

Both a call and a put currently are traded on stock XYZ; both have strike prices of $41 and expirations of six months. Required: a. What will be the profit/loss to an investor who buys the call for $4.40 in the following scenarios for stock prices in six months? (Loss amounts should be indicated by a minus sign. Round your answers to 2 decimal places.) b. What will be the profit/loss in each scenario to an investor who buys the put for $7.90 ? (Loss amounts should be indicated by a minus sign. Round your answers to 2 decimal places.) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management For Technology Start Ups

Authors: Alnoor Bhimani

2nd Edition

1398603082, 978-1398603080