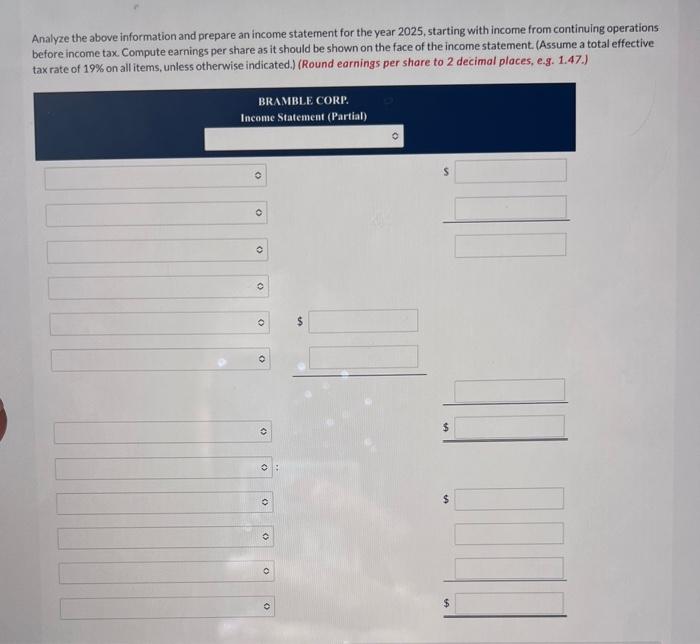

Bramble Corp. has 149,750 shares of common stock outstanding. In 2025, the company reports income from continuing operations before income tax of $1,213,100. Additional transactions not considered in the $1,213,100 are as follows. 1. In 2025, Bramble Corp. sold equipment for $37,200. The machine had originally cost $83,400 and had accumulated depreciation of $32,300. The gain or loss is considered non-recurring. 2. The company discontinued operations of one of its subsidiaries during the current year at a loss of $191,200 before taxes. Assume that this transaction meets the criteria for discontinued operations. The loss from operations of the discontinued subsidiary was $92,400 before taxes; the loss from disposal of the subsidiary was $98,800 before taxes. 3. An internal audit discovered that amortization of intangible assets was understated by $38,900 (net of tax) in a prior period. The amount was charged against retained earnings. 4. The company recorded a non-recurring gain of $127,400 on the condemnation of some of its property (included in the $1,213,100) Analyze the above information and prepare an income statement for the year 2025 , starting with income from continuing operations before income tax. Compute earnings per share as it should be shown on the face of the income statement. (Assume a total effective tax rate of 19% on all items, unless otherwise indicated.) (Round earnings per share to 2 decimal places, e.s. 1.47.) Analyze the above information and prepare an income statement for the year 2025 , starting with income from continuing operations before income tax. Compute earnings per share as it should be shown on the face of the income statement. (Assume a total effective . income tax. Compute earnings per share asit shoume unlace nthenwien indicated.) (Round earnings per share to 2 decimal places, e.g. 1.47.) Bramble Corp. has 149,750 shares of common stock outstanding. In 2025, the company reports income from continuing operations before income tax of $1,213,100. Additional transactions not considered in the $1,213,100 are as follows. 1. In 2025, Bramble Corp. sold equipment for $37,200. The machine had originally cost $83,400 and had accumulated depreciation of $32,300. The gain or loss is considered non-recurring. 2. The company discontinued operations of one of its subsidiaries during the current year at a loss of $191,200 before taxes. Assume that this transaction meets the criteria for discontinued operations. The loss from operations of the discontinued subsidiary was $92,400 before taxes; the loss from disposal of the subsidiary was $98,800 before taxes. 3. An internal audit discovered that amortization of intangible assets was understated by $38,900 (net of tax) in a prior period. The amount was charged against retained earnings. 4. The company recorded a non-recurring gain of $127,400 on the condemnation of some of its property (included in the $1,213,100) Analyze the above information and prepare an income statement for the year 2025 , starting with income from continuing operations before income tax. Compute earnings per share as it should be shown on the face of the income statement. (Assume a total effective tax rate of 19% on all items, unless otherwise indicated.) (Round earnings per share to 2 decimal places, e.s. 1.47.) Analyze the above information and prepare an income statement for the year 2025 , starting with income from continuing operations before income tax. Compute earnings per share as it should be shown on the face of the income statement. (Assume a total effective . income tax. Compute earnings per share asit shoume unlace nthenwien indicated.) (Round earnings per share to 2 decimal places, e.g. 1.47.)