Answered step by step

Verified Expert Solution

Question

1 Approved Answer

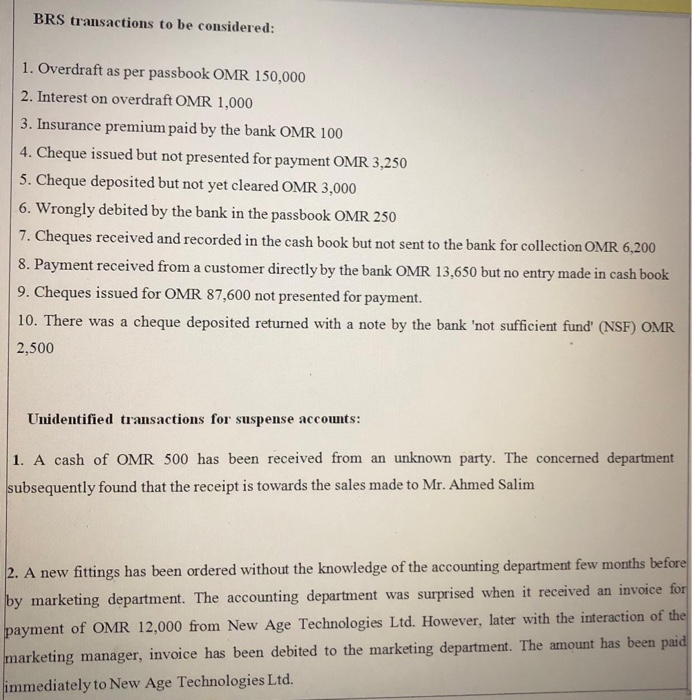

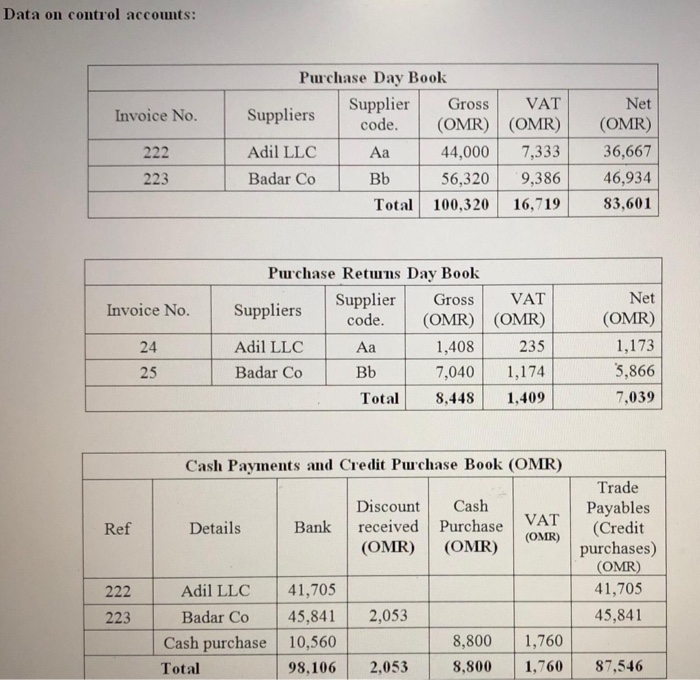

BRS transactions to be considered: 1. Overdraft as per passbook OMR 150,000 2. Interest on overdraft OMR 1,000 3. Insurance premium paid by the bank

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

CIA Part 1 Essentials Of Internal Auditing 2022

Authors: MUHAMMAD ZAIN

1st Edition

B09PHFC28N, 979-8794951356