Answered step by step

Verified Expert Solution

Question

1 Approved Answer

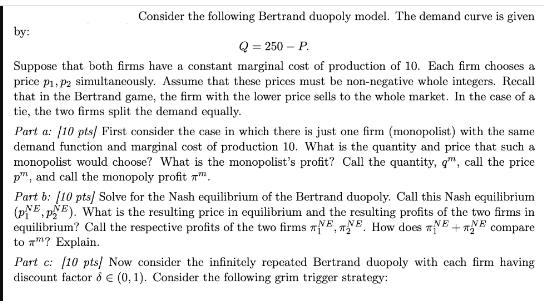

by: Consider the following Bertrand duopoly model. The demand curve is given Q=250-P. Suppose that both firms have a constant marginal cost of production

by: Consider the following Bertrand duopoly model. The demand curve is given Q=250-P. Suppose that both firms have a constant marginal cost of production of 10. Each firm chooses a price P1, P2 simultaneously. Assume that these prices must be non-negative whole integers. Recall that in the Bertrand game, the firm with the lower price sells to the whole market. In the case of a tie, the two firms split the demand equally. Part a: [10 pts/ First consider the case in which there is just one firm (monopolist) with the same demand function and marginal cost of production 10. What is the quantity and price that such a monopolist would choose? What is the monopolist's profit? Call the quantity, q", call the price p", and call the monopoly profit NE Part b: [10 pts] Solve for the Nash equilibrium of the Bertrand duopoly. Call this Nash equilibrium (pp). What is the resulting price in equilibrium and the resulting profits of the two firms in equilibrium? Call the respective profits of the two firms E, E. How does E+E compare to? Explain. Part c: [10 pts] Now consider the infinitely repeated Bertrand duopoly with each firm having discount factor (0, 1). Consider the following grim trigger strategy: Play (ppm) as long as no firm deviated from these prices in the past. Otherwise play (PNE,PE). For what values of 5 is the above grim trigger strategy a subgame perfect Nash equilibrium? Explain.

Step by Step Solution

★★★★★

3.48 Rating (151 Votes )

There are 3 Steps involved in it

Step: 1

Part a To find the quantity and price that a monopolist would choose we can maximize the monopolists profit function The monopolists profit function i...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Microeconomics

Authors: Douglas Bernheim, Michael Whinston

2nd edition

73375853, 978-0073375854