Answered step by step

Verified Expert Solution

Question

1 Approved Answer

by using these answer the following questions 2. In completing the time record columns of the payroll register for all work- ers, you should place

by using these answer the following questions

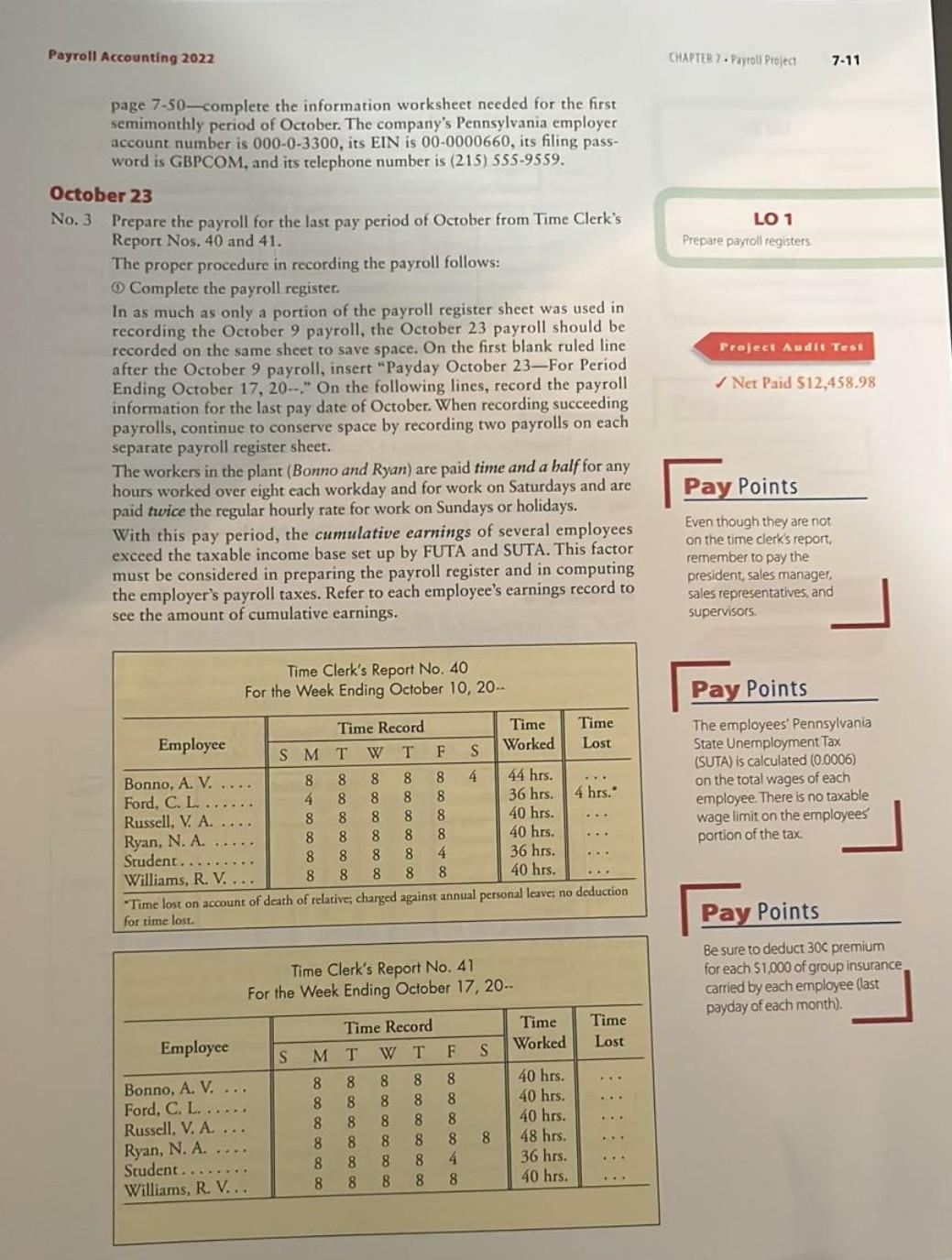

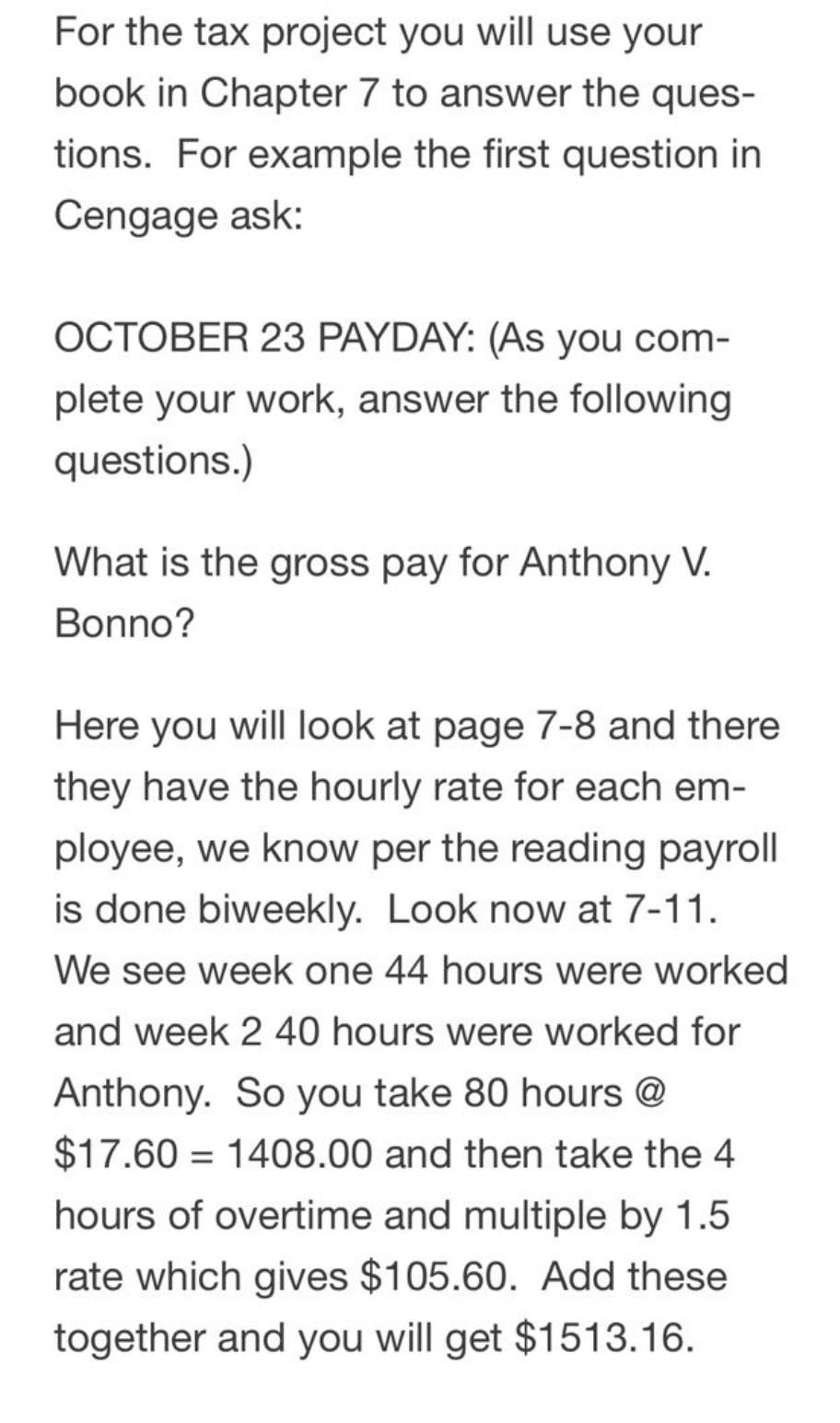

2. In completing the time record columns of the payroll register for all work- ers, you should place an 8 in the day column for each full day worked (refer to page PR-2 at the end of the book). If an employee works less than a full day, show the actual hours for which the employee will be paid. 3. In the case of an employee who begins work during a pay period, compute the earnings by paying the employees their weekly rate for any full week worked. For any partial week, compute the earnings for that week by mul- tiplying the hours worked by the hourly rate of pay. 4. If time lost is to be deducted from a salaried employee's pay, the employ- ce's pay must be determined by multiplying the actual hours worked for that week by the hourly rate. If hours are missed but no pay is deducted, include those hours in the Time Record columns on the payroll register. The following schedule shows the weekly and hourly wage rates of the salaried employees: Employee Ferguson, James Ford, Catherine L. Mann, Dewey W. O'Neill, Joseph T. Russell, Virginia A. Sokowski, Thomas). Williams, Ruth V. *O'Neill is paid on a biweekly basis. Weekly Rate $1,125.00 610.00 675.00 2,307.69* 600.00 1,025.00 611.54 Hourly Rate $28.13 15.25 16.88 28.85 15.00 25.63 15.29 5. Plant workers (Bonno and Ryan), other than supervisors, are employed on an hourly basis. Compute the wages by multiplying the number of hours worked during the pay period by the employee's hourly rate. 6. The information needed and the sequence of steps that are completed for the payroll are presented in the following discussion. Time Clerk's Report No. 38 For the Week Ending September 26, 20-- Time Record Time Time Worked Employee Lost SM T W T S F. Bonno, A. V..... Ford, C. L... Russell, V. A.... Ryan, N. A. Student Williams, R. V... 8 8 8 8 Oo ooo 0 8 8 8 8 8 8 8 8 8 8 8 D 00 00 00 00 00 00 8 8 8 8 8 8 200 00 00 00 8 8 8 8 4 8 40 hrs. 40 hrs. 40 hrs. 40 hrs. 36 hrs. 32 hrs. 8 8 00 00 00 8 hrs. *Time lost because of personal business; charged to personal leave; no deduction for this time lost. D - lost full day Payroll Accounting 2022 Time Lost S ... Employee Time Clerk's Report No. 39 For the Week Ending October 3, 20- Time Time Record Worked S M T W T F 8 8 8 8 8 40 hrs. 8 8 8 8 8 8 40 hrs. 8 8 8 8 8 40 hrs. 8 8 8 8 8 8 40 hrs. 8 8 8 8 8 4 4 36 hrs. 8 8 8 8 40 hrs. .. Bonno, A. V..... Ford, C.L. Russell, V, A. Ryan, N. A...... Student .... Williams, R. V... .. 8 The time clerk prepared Time Clerk's Report Nos. 38 and 39 from the time cards used by the employees for these workweeks. In as much as the president, sales manager, sales representatives, and supervisors do not ring in and out on the time clock, their records are not included in the time clerks report, but their sal- aries must be included in the payroll. The following schedule shows the hourly wage rates of the three hourly employees used in preparing the payroll register for the payday on October 9. Employee Hourly Rate $17.60 Bonno, Anthony V. 18.00 Ryan, Norman A. 15.00 Student...... The entry required for each employee is recorded in the payroll register. The names of all employees are listed in alphabetical order, including yours as Stu- dent." The fold-out payroll register forms needed to complete this project are bound at the back of the book (pages PR-2, PR-3, and PR-4). No deduction has been made for the time lost by Williams. Thus, the total num- ber of hours (80) for which payment was made is recorded in the Regular Earn- ings Hours column of the payroll register. However, a notation of the time lost (D) was made in the Time Record column. When posting to Williams's earnings record, 80 hours is recorded in the Regular Earnings Hours column (no deduc- tion for the time lost). In computing the federal income taxes to be withheld, the Wage Bracket Method Tables for Manual Payroll Systems With Forms W-4 From 2020 or Later (using standard withholding column) - Biweekly Payroll Period in Tax Table B at the back of the book were used (pages T-7 and T-8). Each payday, $8 was deducted from the earnings of the two plant workers for union dues (Bonno and Ryan). Payroll check numbers were assigned beginning with check no. 672. In the Labor Cost Distribution columns at the extreme right of the payroll reg- ister, each employee's gross earnings were recorded in the column that identifies the department in which the employee regularly works. The totals of the Labor Cost Distribution columns provide the amounts to be charged to the appropriate salary and wage expense accounts and aid department managers and supervisors in comparing the actual labor costs with the budgeted amounts. Once the net pay of each employee was computed, all the amount columns in the payroll register were footed, proved, and ruled. Payroll Accounting 2022 CHAPTER 7. Payroll Pr An entry was made in the journal (page 7-24) transferring from the regular cash account to the payroll cash account the amount of the check issued to Pay- roll to cover the net amount of the payroll; next, the entry was posted. Information from the payroll register was posted to the employees' earnings records (see pages 7-42 to 7-46). Note that when posting the deductions for each employee, a column has been provided in the earnings record for recording each deduction for FICA (OASDI and HI), FIT, SIT, SUTA, and CIT. All other deductions for each employee are to be totaled and recorded as one amount in the Other Deductions column. Subsid- iary ledgers are maintained for Group Insurance Premiums Collected and Union Dues Withheld. Thus, any question about the amounts withheld from an employ- ce's earnings may be answered by referring to the appropriate subsidiary ledger. In this project, your work will not involve any recording in or reference to the subsidiary ledgers. The proper journal entry recorded salaries, wages, taxes, and the net amount of cash paid from the totals of the payroll register. The journal entry to record the payroll for the first pay in the fourth quarter appears below and in the general journal (page 7-24). 2,307.69 4,723.08 3,600.00 4,898.00 Administrative Salaries Office Salaries Sales Salaries Plant Wages FICA Taxes Payable-OASDI FICA Taxes Payable-HI Employees FIT Payable. Employees SIT Payable Employees SUTA Payable. Employees CIT Payable Union Dues Payable Payroll Cash 962.79 225.18 841.00 476.76 9.30 601.16 16.00 12,396.58 The amounts charged the salary and wage expense accounts were obtained from the totals of the Labor Cost Distribution columns in the payroll register. The sal- aries and wages were charged as follows: Administrative Salaries Joseph T O'Neill (President) Office Salaries Catherine L. Ford (Executive Secretary) Virginia A. Russell (Time Clerk) Student (Accounting Trainee) Ruth V. Williams (Programmer) Sales Salaries James C. Ferguson (Sales Manager) Dewey W. Mann (Sales Representative) Plant Wages Anthony V. Bonno (Mixer Operator) Norman A. Ryan (Electrician) Thomas J. Sokowski (Supervisor) Payroll Accounting 2022 7. Payroll Project P $962.79 and $225.18, respectively, the amounts deducted from employees' wages. FICA Taxes Payable-OASDI and FICA Taxes Payable-HI were credited for Employees CIT Payable, and Union Dues Payable were credited for the total Employees FIT Payable, Employees SIT Payable, Employees SUTA Payable, payroll transactions, Group Insurance Premiums Collected will be credited for the amount withheld for each kind of deduction from employees' wages. In subsequent amounts withheld from employees' wages for this type of deduction. Finally, Pay- roll Cash was credited for the sum of the nct amounts paid all employees, The payroll taxes for this pay were then recorded in the general journal (page 1,390.21 7-24) as follows: 962.78 225.17 23.34 178.92 Payroll Taxes FICA Taxes Payable-OASDI FICA Taxes Payable-HI. FUTA Txes Payable SUTA Taxes Payable-Employer Payroll Taxes was debited for the sum of the employer's FICA, FUTA, and SUTA taxes. The taxable carnings used in computing each of these payroll taxes were obtained from the appropriate column totals of the payroll register . Note that only part of Ford's wages are taxable (S700 out of $1,220 gross pay) for FUTA (S7,000 limit). The computation of the debit to Payroll Taxes was: FICA-OASOL: FICAH FUTA: SUTA: Total Payroll Taxes 6.296 of $15,528.77 = 1.45% of $15,528.77= 0.6% of $3,890.00 = 3.6890% of 54,850.00 = $ 962.78 225.17 23.34 178.92 51,390.21 EICA Taxes Payable-OASDI was credited for $962.78, the amount of the lia- bility for the employer's portion of the tax. FICA Taxes Payable-HI was cred- ited for $225.17, the amount of the liability for the employer's share of this tax. FUTA Taxes Payable was credited for the amount of the tax on the employer for federal unemployment purposes ($23.34). SUTA Taxes Payable-Employer was credited for $178.92, which is the amount of the contribution required of the employer under the state unemployment compensation law. The journal entries were posted to the proper ledger accounts (pages 7-33 to 7-40). October 15 This is the day on which the deposits of FICA and FIT taxes and the city of Philadelphia income taxes for the September payrolls are due. However, in order to concentrate on the fourth-quarter payrolls, we will assume that the deposits for the third quarter and the appropriate entries were already completed. October 20 No.2 On this date, Glo-Brite Paint Company must deposit the Pennsylvania state income taxes withheld from the October 9 payroll. The deposit rule states that if the employer expects the aggregate amount withheld each quarter to be $1,000 or more, the employer must pay the withheld tax semimonthly. The tax must be remitted within three banking days after the close of the semimonthly periods ending on the 15th and the last day of the month. Prepare the journal entry to record the deposit of the taxes, and post to the appropriate ledger accounts. Pennsylvania has eliminated the filing of paper forms (replaced by telefile or online filing). The information needed to telefile is listed on Payroll Accounting 2022 CHAPTER 2. Payroll Project 7-11 LO 1 Prepare payroll registers Project Audit Test page 7-50-complete the information worksheet needed for the first semimonthly period of October. The company's Pennsylvania employer account number is 000-0-3300, its EIN is 00-0000660, its filing pass- word is GBPCOM, and its telephone number is (215) 555-9559. October 23 No. 3 Prepare the payroll for the last pay period of October from Time Clerk's Report Nos. 40 and 41. The proper procedure in recording the payroll follows: : Complete the payroll register. In as much as only a portion of the payroll register sheet was used in recording the October 9 payroll, the October 23 payroll should be recorded on the same sheet to save space. On the first blank ruled line after the October 9 payroll, insert "Payday October 23-For Period Ending October 17, 20--" On the following lines, record the payroll information for the last pay date of October. When recording succeeding payrolls, continue to conserve space by recording two payrolls on each separate payroll register sheet. The workers in the plant (Bonno and Ryan) are paid time and a half for any hours worked over eight each workday and for work on Saturdays and are paid twice the regular hourly rate for work on Sundays or holidays. With this pay period, the cumulative earnings of several employees exceed the taxable income base set up by FUTA and SUTA. This factor must be considered in preparing the payroll register and in computing the employer's payroll taxes. Refer to each employee's earnings record to see the amount of cumulative earnings. Net Paid $12,458.98 Pay Points Even though they are not on the time clerk's report, remember to pay the president, sales manager, sales representatives, and supervisors. Time Clerk's Report No. 40 For the Week Ending October 10, 20. Pay Points The employees' Pennsylvania State Unemployment Tax (SUTA) is calculated (0.0006) on the total wages of each employee. There is no taxable wage limit on the employees portion of the tax --- Time Record Time Time Employee Lost F S M T W T S S Worked Bonno, A. V. .... 8 8 8 8 8 4 44 hrs. Ford, C. L. ..... 4 8 8 8 8 36 hrs. 4 hrs. Russell, V. A. 8 8 8 8 8 40 hrs. Ryan, N. A...... 8 8 8 8 8 40 hrs. Student..... 8 8 8 8 4 36 hrs. Williams, R. V.... 8 8 8 8 8 8 40 hrs. "Time lost on account of death of relative; charged against annual personal leave; no deduction for time lost. --- Pay Points Time Clerk's Report No. 41 For the Week Ending October 17, 20.. Be sure to deduct 30C premium for each $1,000 of group insurance carried by each employee (last payday of each month). Time Worked Time Lost Employee S S Time Record M T W T F 8 8 8 8 8 8 8 8 8 8 8 8 8 8 8 8 8 8 8 8 8 8 8 8 8 4 8 8 8 8 8 Bonno, A. V. ... Ford, C. L. ... Russell, V. A. Ryan, N. A..... Student.. Williams, R. V... .. 40 hrs. 40 hrs. 40 hrs. 48 hrs. 36 hrs. 40 hrs. 8 ...... OCTOBER 23 PAYDAY: (As you complete your work, answer the following questions.) What is the gross pay for Anthony V. Bonno? ur.com... NOVEMBER 6 PAYDAY: (As you complete your work, answer the following questions.) What is the amount of Sales Salaries paid to date? our.com... NOVEMBER 6 PAYDAY: (As you complete your work, answer the following questions.) What is the balance in the Cash (account number 11) account? For the tax project you will use your book in Chapter 7 to answer the ques- tions. For example the first question in Cengage ask: OCTOBER 23 PAYDAY: (As you com- plete your work, answer the following questions.) What is the gross pay for Anthony V. Bonno? Here you will look at page 7-8 and there they have the hourly rate for each em- ployee, we know per the reading payroll is done biweekly. Look now at 7-11. We see week one 44 hours were worked and week 2 40 hours were worked for Anthony. So you take 80 hours @ $17.60 = 1408.00 and then take the 4 hours of overtime and multiple by 1.5 rate which gives $105.60. Add these together and you will get $1513.16. =

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting

Authors: Donald E. Kieso, Jerry J. Weygandt, and Terry D. Warfield

15th edition

978-1118159644, 9781118562185, 1118159640, 1118147294, 978-1118147290