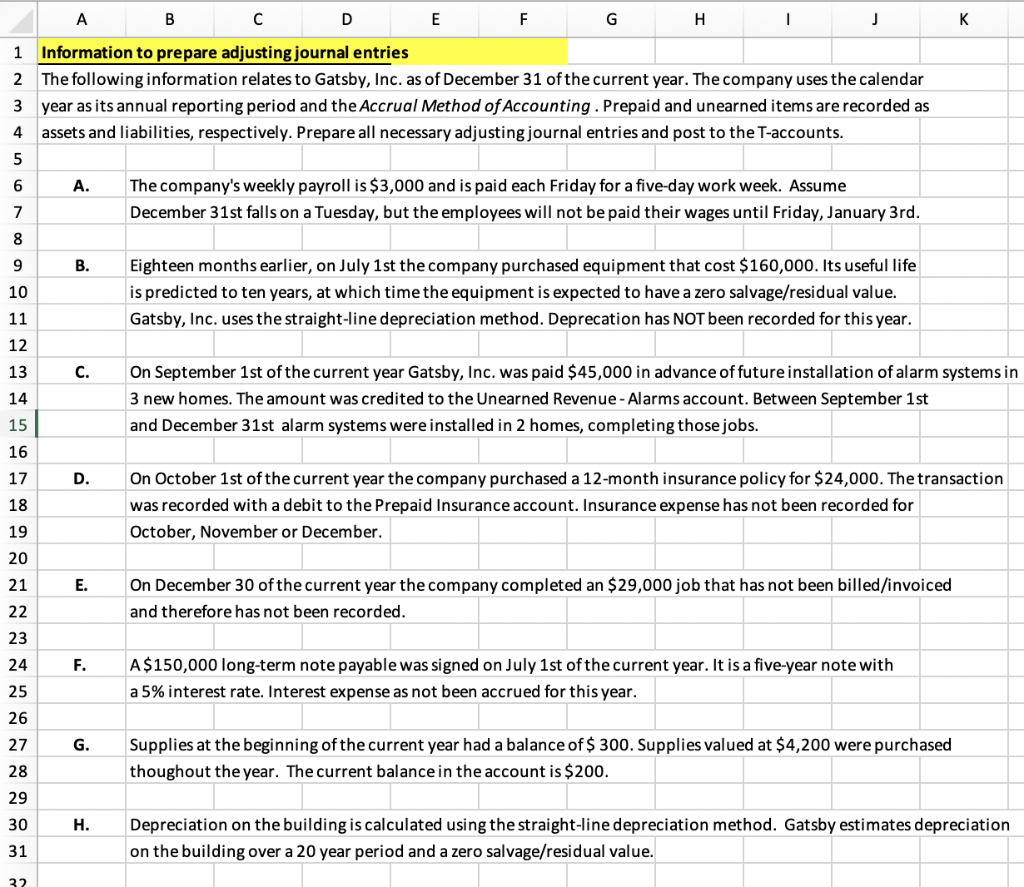

C D E F 1 Information to prepare adjusting journal entries 2 The following information relates to Gatsby, Inc. as of December 31 of the current year. The company uses the calendar 3 year as its annual reporting period and the Accrual Method of Accounting. Prepaid and unearned items are recorded as 4 assets and liabilities, respectively. Prepare all necessary adjusting journal entries and post to the T-accounts. The company's weekly payroll is $3,000 and is paid each Friday for a five-day work week. Assume December 31st falls on a Tuesday, but the employees will not be paid their wages until Friday, January 3rd. Eighteen months earlier, on July 1st the company purchased equipment that cost $160,000. Its useful life is predicted to ten years, at which time the equipment is expected to have a zero salvage/residual value. Gatsby, Inc. uses the straight-line depreciation method. Deprecation has NOT been recorded for this year. On September 1st of the current year Gatsby, Inc. was paid $45,000 in advance of future installation of alarm systems in 3 new homes. The amount was credited to the Unearned Revenue - Alarms account. Between September 1st and December 31st alarm systems were installed in 2 homes, completing those jobs. On October 1st of the current year the company purchased a 12-month insurance policy for $24,000. The transaction was recorded with a debit to the Prepaid Insurance account. Insurance expense has not been recorded for October, November or December. On December 30 of the current year the company completed an $29,000 job that has not been billed/invoiced and therefore has not been recorded. 24 F. A$ 150,000 long-term note payable was signed on July 1st of the current year. It is a five-year note with a 5% interest rate. Interest expense as not been accrued for this year. G. Supplies at the beginning of the current year had a balance of $ 300. Supplies valued at $4,200 were purchased thoughout the year. The current balance in the account is $200. H. Depreciation on the building is calculated using the straight-line depreciation method. Gatsby estimates depreciation on the building over a 20 year period and a zero salvage/residual value. C D E F 1 Information to prepare adjusting journal entries 2 The following information relates to Gatsby, Inc. as of December 31 of the current year. The company uses the calendar 3 year as its annual reporting period and the Accrual Method of Accounting. Prepaid and unearned items are recorded as 4 assets and liabilities, respectively. Prepare all necessary adjusting journal entries and post to the T-accounts. The company's weekly payroll is $3,000 and is paid each Friday for a five-day work week. Assume December 31st falls on a Tuesday, but the employees will not be paid their wages until Friday, January 3rd. Eighteen months earlier, on July 1st the company purchased equipment that cost $160,000. Its useful life is predicted to ten years, at which time the equipment is expected to have a zero salvage/residual value. Gatsby, Inc. uses the straight-line depreciation method. Deprecation has NOT been recorded for this year. On September 1st of the current year Gatsby, Inc. was paid $45,000 in advance of future installation of alarm systems in 3 new homes. The amount was credited to the Unearned Revenue - Alarms account. Between September 1st and December 31st alarm systems were installed in 2 homes, completing those jobs. On October 1st of the current year the company purchased a 12-month insurance policy for $24,000. The transaction was recorded with a debit to the Prepaid Insurance account. Insurance expense has not been recorded for October, November or December. On December 30 of the current year the company completed an $29,000 job that has not been billed/invoiced and therefore has not been recorded. 24 F. A$ 150,000 long-term note payable was signed on July 1st of the current year. It is a five-year note with a 5% interest rate. Interest expense as not been accrued for this year. G. Supplies at the beginning of the current year had a balance of $ 300. Supplies valued at $4,200 were purchased thoughout the year. The current balance in the account is $200. H. Depreciation on the building is calculated using the straight-line depreciation method. Gatsby estimates depreciation on the building over a 20 year period and a zero salvage/residual value