Answered step by step

Verified Expert Solution

Question

1 Approved Answer

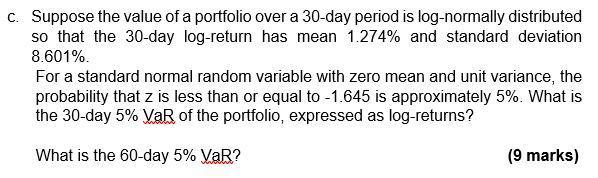

c. Suppose the value of a portfolio over a 30-day period is log-normally distributed so that the 30-day log-return has mean 1.274% and standard

c. Suppose the value of a portfolio over a 30-day period is log-normally distributed so that the 30-day log-return has mean 1.274% and standard deviation 8.601%. For a standard normal random variable with zero mean and unit variance, the probability that z is less than or equal to -1.645 is approximately 5%. What is the 30-day 5% VaR of the portfolio, expressed as log-returns? What is the 60-day 5% VaR? (9 marks)

Step by Step Solution

★★★★★

3.47 Rating (154 Votes )

There are 3 Steps involved in it

Step: 1

Calculating the 30day and 60day 5 VaR for the portfolio Given Portfolio logreturn mean 1274 Portfoli...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introductory Statistics

Authors: Prem S. Mann

8th Edition

9781118473986, 470904100, 1118473981, 978-0470904107