C16.48 Activity-based costing; activity-based management; non-value-added costs; LO16.2 BPR; target costing: manufacturer 16.3 Schmidtke's Meat Pty Ltd manufactures smoked meat products in the Barossa Valley,

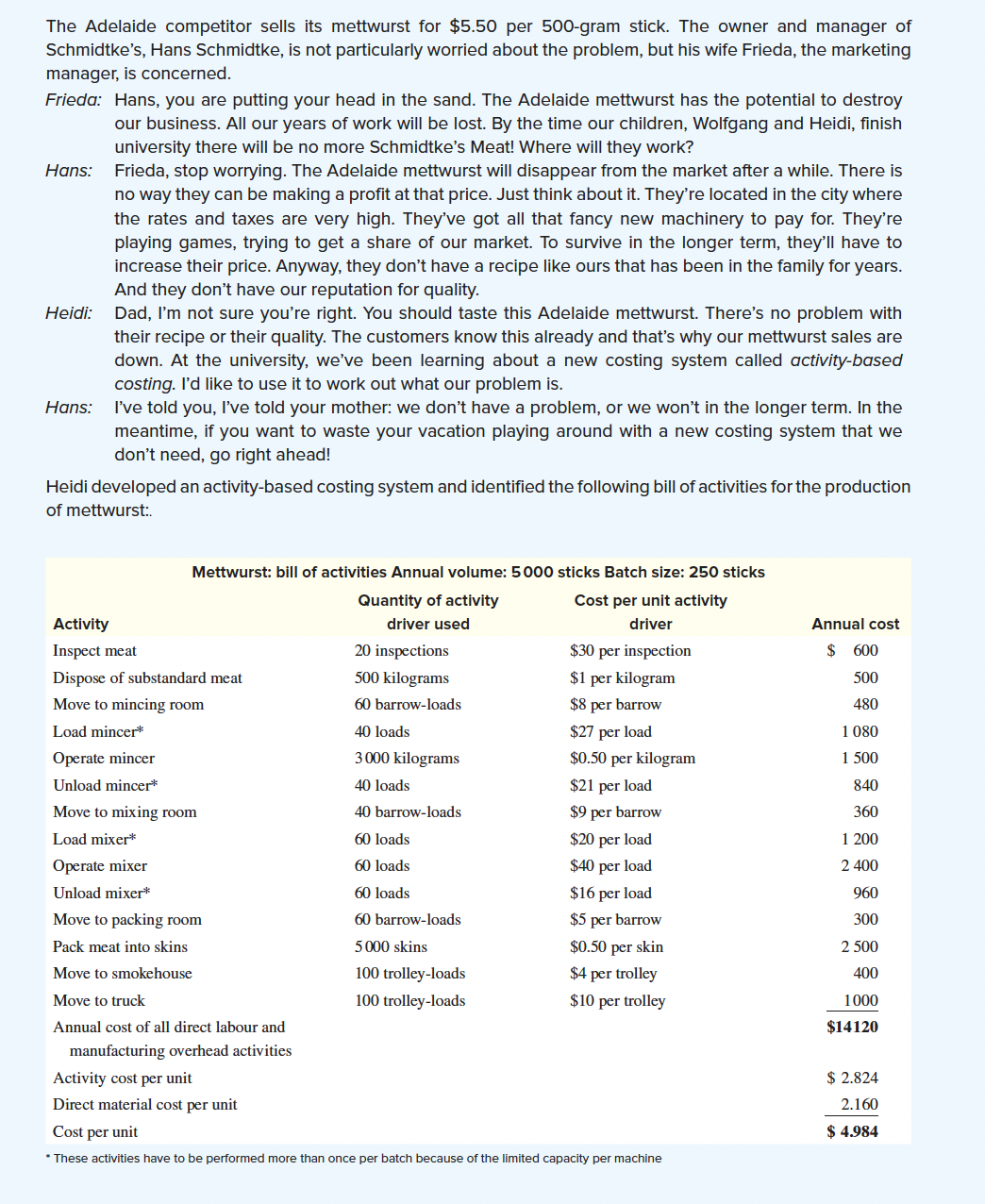

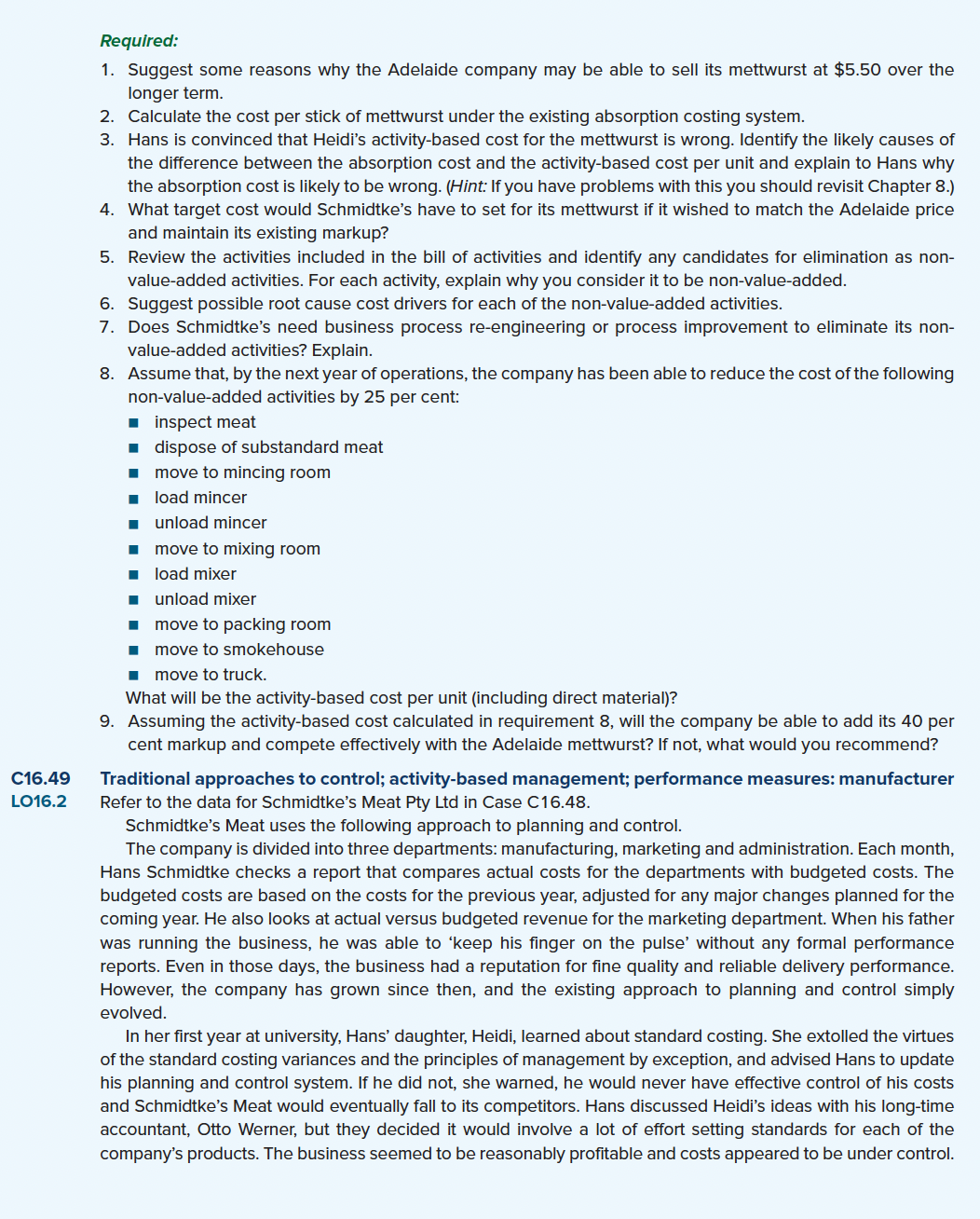

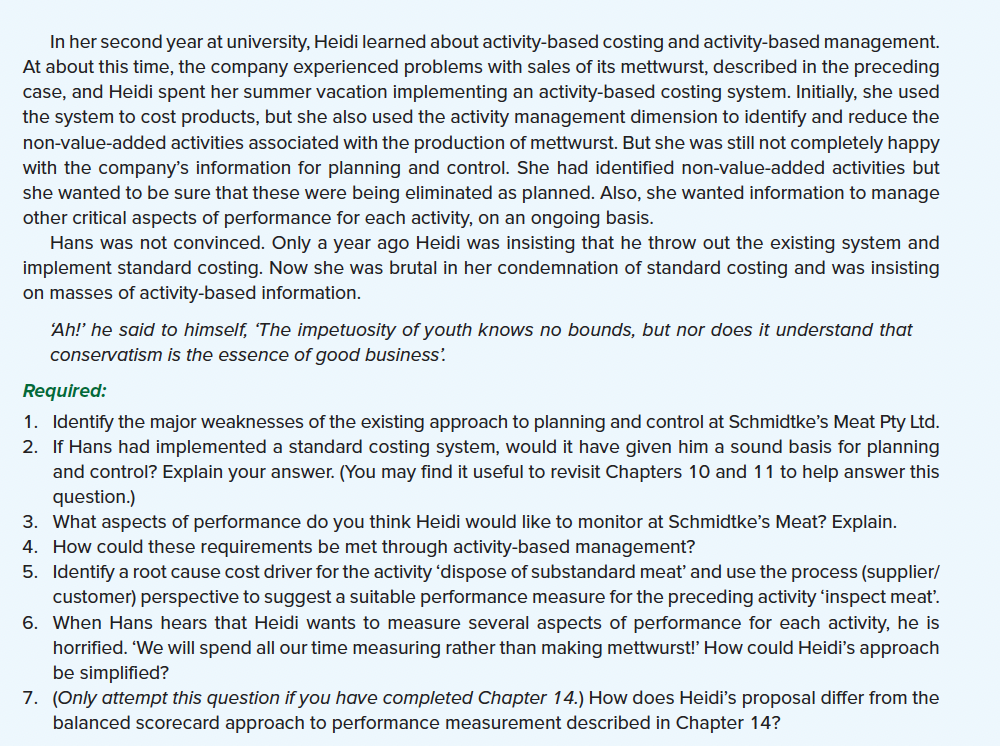

C16.48 Activity-based costing; activity-based management; non-value-added costs; LO16.2 BPR; target costing: manufacturer 16.3 Schmidtke's Meat Pty Ltd manufactures smoked meat products in the Barossa Valley, using processes that 16.5 have been handed down from one generation of Schmidtkes to the next. Recently, one of the company's major high-volume products, mettwurst, has come under intense pressure from an Adelaide manufacturer that uses modern manufacturing processes. Schmidtke's mettwurst sells for $7 per 500-gram stick, based on a cost-plus pricing system. (The company applies manufacturing overhead using a plantwide overhead rate based on the number of direct labour hours worked. Prices are based on absorption cost plus a 40 per cent markup.)|The Adelaide competitor sells its mettwurst for $5.50 per SOD-gram stick. The owner and manager of Schmidtke's, Hans Schmidtke, is not particularty worried about the problem, but his wife Frieda, the marketing manager, is concerned. Frieda: Hans, you are putting your head in the sand. The Adelaide mettwurst has the potential to destroy our business. All our years of work will be lost. By the time our chiidren, Wolfgang and Heidi, nish university there will be no more Schmidtke's Meat! Where will they work? Hans: Frieda, stop worrying. The Adelaide mettwurst will disappear from the market after a while. There is no way they can be making a prot at that price. Just think about it. They're located in the city where the rates and taxes are very high. They've got all that fancy new machinery to pay for. They're playing games, trying to get a share of our market. To survive in the longer term, they'll have to increase their price. Anyway, they don't have a recipe like ours that has been in the family for years. And they don't have our reputation for quality. Heidi: Dad, I'm not sure you're right. You should taste this Adelaide mettwurst. There's no problem with their recipe or their quality. The customers know this already and that's why our mettwurst sales are down. At the university, we've been learning about a new costing system called activity-based costing. I'd like to use it to work out what our problem is. Hons: We told you, I've told your mother: we don't have a problem, or we won't in the longer term. In the meantime, if you want to waste your vacation playing around with a new costing system that we don't needr go right ahead! Heidi developed an activity-based costing system and identied the following bill of activities for the production of mettwurst; Mettwurst: bill of activities Annual volume: 5000 sticks Batch size: 250 sticks Quantity of activity Cost per unit activity Activity driver used driver Annual cost Inspect meat 20 inspections $30 per inspection $ 600 Dispose of substandard meat 500 kilograms $1 per kilogram 500 Move to mincing room 60 barrow-loads $3 per barrow 480 Load mincer\" 40 loads $2? per load 1 080 Operate minoer 3 000 kilograms $0.50 per kilogram 1 500 Unload minoer\" 40 loads $21 per load 840 Move to mixing room 40 barrow-loads $9 per izlarriovvur 360 Load mixer\" 60 loads $20 per load 1 200 Operate mixer 60 loads $40 per load 2 400 Unload mixer'\" 60 loads $16 per load 960 Move to packing room 60 barrow-loads $5 per barrow 300 Pack meat into skins 5 000 skins $0.50 per skin 2 500 Move to smokehouse 100 trolley-loads $4 per trolley 400 Move to truck 100 trolley-loads $10 per trolley 1000 Annual cost of all direct labour and $14120 manufacturing overhead activities Activity cost per unit $ 2.824 Direct material cost per unit 2.160 Cost per unit $ 4.984 These activities have to be performed more than once per batch because ofthe limited capacity per machine C16.49 L016.2 Required: 1. Suggest some reasons why the Adelaide company may be able to sell its mettwurst at $5.50 over the longer term. 2. Calculate the cost per stick of mettwurst under the existing absorption costing system. 3. Hans is convinced that Heidi's activity-based cost for the mettwurst is wrong. Identify the likely causes of the difference between the absorption cost and the activity-based cost per unit and explain to Hans why the absorption cost is likely to be wrong. (Hint: If you have problems with this you should revisit Chapter 8.) 4. What target cost would Schmidtke's have to set for its mettwurst if it wished to match the Adelaide price and maintain its existing markup? 5. Review the activities included in the bill of activities and identify any candidates for elimination as non- value-added activities. For each activity, explain why you consider it to be non-value-added. Suggest possible root cause cost drivers for each of the non-valueadded activities. Does Schmidtke's need business process re-engineering or process improvement to eliminate its non- value-added activities? Explain. 8. Assume that, bythe next year of operations, the company has been able to reduce the cost ofthe following non-valueadded activities by 25 per cent: inspect meat dispose of substandard meat move to mincing room load mincer unload mincer move to mixing room load mixer unload mixer move to packing room move to smokehouse move to truck. What will be the activity-based cost per unit (including direct material)? 9. Assuming the activity-based cost calculated in requirement 8. will the company be able to add its 40 per cent markup and compete effectively with the Adelaide mettwurst? If not, what would you recommend? 749' Traditional approaches to control; activity-based management; performance measures: manufacturer Refer to the data for Schmidtke's Meat Pty Ltd in Case C1648. Schmidtke's Meat uses the following approach to planning and control. The company is divided into three departments: manufacturing, marketing and administration. Each month, Hans Schmidtke checks a report that compares actual costs for the departments with budgeted costs. The budgeted costs are based on the costs for the previous year, adjusted for any major changes planned for the coming year. He also looks at actual versus budgeted revenue for the marketing department. When his father was running the business, he was able to 'keep his nger on the pulse' without any formal performance reports. Even in those days, the business had a reputation for fine quality and reliable delivery performance. However, the company has grown since then, and the existing approach to planning and control simply evolved. In her rst year at university, Hans' daughter, Heidi, learned about standard costing. She extolled the virtues of the standard costing variances and the principles of management by exception, and advised Hans to update his planning and control system. If he did not, she wan-ledI he would never have effective control of his costs and Schmidtke's Meat would eventually fall to its competitors. Hans discussed Heidi's ideas with his long-time accountant, Otto Werner, but they decided it would involve a lot of effort setting standards for each of the company's products. The business seemed to be reasonably protable and costs appeared to be under control. In her second year at university, Heidi learned about activity-based costing and activity-based management. At about this time,the company experienced problems with sales of its mettwurst, described in the preceding case, and Heidi spent her summer vacation implementing an activity-based costing system. Initially, she used the system to cost products, but she also used the activity management dimension to identify and reduce the non-value-a dded activities associated with the production of mettwurst. But she was still not completely happy with the company's information for planning and control. She had identied non-value-added activities but she wanted to be sure that these were being eliminated as planned. Also, she wanted information to manage other critical aspects of performance for each activity. on an ongoing basis. Hans was not convinced. Only a year ago Heidi was insisting that he throw out the existing system and implement standard costing. Now she was brutal in her condemnation of standard costing and was insisting on masses of activity-based information. 2th he said to himsehf 'The impetuosiiy of youth knows no bounds, but nor does it understand that conservatism is the essence of good business'. Required: 1. Identify the major weaknesses of the existing approach to planning and control at Schmidtke's Meat Pty Ltd. 2. If Hans had implemented a standard costing system, would it have given him a sound basis for planning and control? Explain your answer. {You may nd it useful to revisit Chapters 10 and 1 1 to help answer this question} What aspects of performance do you think Heidi would like to monitor at Schmidtke's Meat? Explain. How could these requirements be met through activity-based management? Identify a root cause cost driver for the activity 'dispose of substandard meat' and use the process (supplier! customer} perspective to suggest a suitable performance measure for the preceding activity 'inspect meat'. 6. When Hans hears that Heidi wants to measure several aspects of performance for each activity, he is horried. 'We will spend all ourtime measuring ratherthan making mettwurst!' How could Heidi's approach be simplied? 7. {Only attempt this question if you have completed Chapter 1 4.) How does Heidi's proposal differ from the balanced scorecard approach to performance measurement described in Chapter 14? 91:15.\

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance