Question

Cabanarama Inc. designs and manufactures easy-to-set-up beach cabanas that families can set up for picnicking, protection from the sun, and so on. The cabanas come

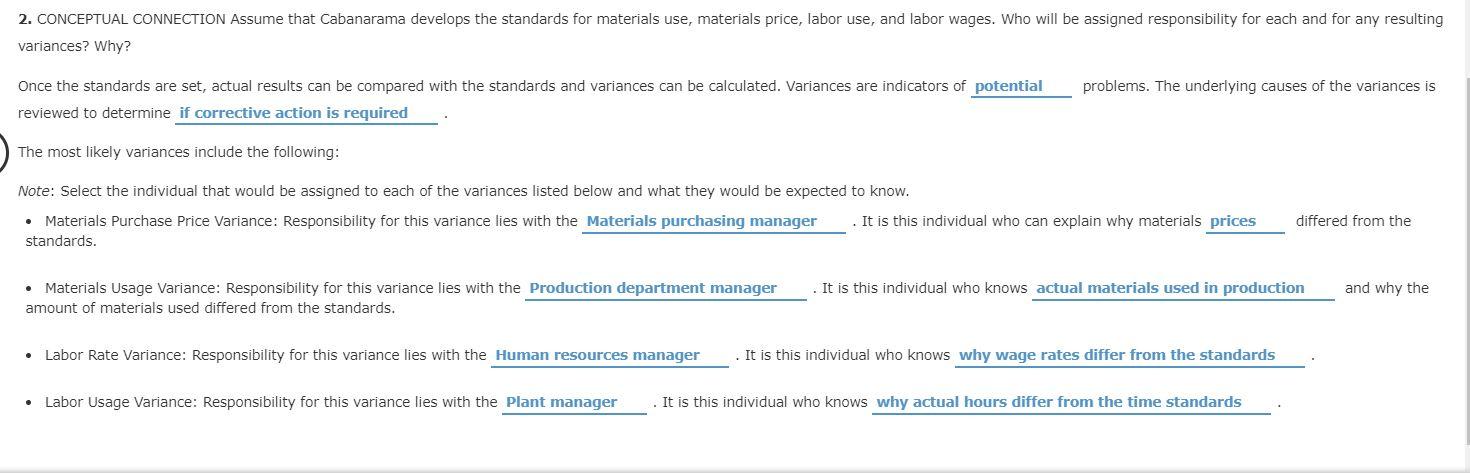

Cabanarama Inc. designs and manufactures easy-to-set-up beach cabanas that families can set up for picnicking, protection from the sun, and so on. The cabanas come in a kit that includes canvas, lacing, and aluminum support poles. Cabanarama has expanded rapidly from a 2-person operation to one involving over a hundred employees. Cabanaramas founder and owner, Frank Love, understands that a more formal approach to standard setting and control is needed to ensure that the consistent quality for which the company is known continues. Frank and Annette Wilson, his financial vice president, divided the company into departments and designated each department as a cost center. Sales, Quality Control, and Design report directly to Frank. Production, Shipping, Finance, and Accounting report to Annette. In the production department, one of the supervisors was assigned the materials purchasing function. The job included purchasing all raw materials, overseeing inventory handling (receiving, storage, etc.), and tracking materials purchases and use Frank felt that control would be better achieved if there were a way for his employees to continue to perform in such a way that quality was maintained and cost reduction was achieved. Annette suggested that Cabanarama institute a standard costing system. Variances for materials and labor could then be calculated and reported directly to her, and she could alert Frank to any problems or opportunities for improvement. Required: 1. a. CONCEPTUAL CONNECTION When Annette designs the standard costing system for Cabanarama, who should be involved in setting the standards for each cost component? a. The managers of accounting, production and purchasing. b. The top management of the company. c. The managers of accounting and human resources. d. The managers of accounting and outside consultants. b. What factors should be considered in establishing the standards for each cost component? a. Standards should be attainable and exact with no room for any wastage and breakdown. b. Standards should be attainable and should include an allowance for any wastage and breakdown. c. Standards should be exact and above attainable levels so that the staff can be pushed to perform better. 2. CONCEPTUAL CONNECTION Assume that Cabanarama develops the standards for materials use, materials price, labor use, and labor wages. Who will be assigned responsibility for each and for any resulting variances? Why? Once the standards are set, actual results can be compared with the standards and variances can be calculated. Variances are indicators of potential problems. The underlying causes of the variances is reviewed to determine if corrective action is required . The most likely variances include the following: Note: Select the individual that would be assigned to each of the variances listed below and what they would be expected to know. Materials Purchase Price Variance: Responsibility for this variance lies with the Materials purchasing manager . It is this individual who can explain why materials prices differed from the standards. Materials Usage Variance: Responsibility for this variance lies with the Production department manager . It is this individual who knows actual materials used in production and why the amount of materials used differed from the standards. Labor Rate Variance: Responsibility for this variance lies with the Human resources manager . It is this individual who knows why wage rates differ from the standards . Labor Usage Variance: Responsibility for this variance lies with the Plant manager . It is this individual who knows why actual hours differ from the time standards .

Cabanarama Inc. designs and manufactures easy-to-set-up beach cabanas that families can set up for picnicking, protection from the sun, and so on. The cabanas come in a kit that includes canvas, lacing, and aluminum support poles. Cabanarama has expanded rapidly from a 2-person operation to one involving over a hundred employees. Cabanaramas founder and owner, Frank Love, understands that a more formal approach to standard setting and control is needed to ensure that the consistent quality for which the company is known continues. Frank and Annette Wilson, his financial vice president, divided the company into departments and designated each department as a cost center. Sales, Quality Control, and Design report directly to Frank. Production, Shipping, Finance, and Accounting report to Annette. In the production department, one of the supervisors was assigned the materials purchasing function. The job included purchasing all raw materials, overseeing inventory handling (receiving, storage, etc.), and tracking materials purchases and use Frank felt that control would be better achieved if there were a way for his employees to continue to perform in such a way that quality was maintained and cost reduction was achieved. Annette suggested that Cabanarama institute a standard costing system. Variances for materials and labor could then be calculated and reported directly to her, and she could alert Frank to any problems or opportunities for improvement. Required: 1. a. CONCEPTUAL CONNECTION When Annette designs the standard costing system for Cabanarama, who should be involved in setting the standards for each cost component? a. The managers of accounting, production and purchasing. b. The top management of the company. c. The managers of accounting and human resources. d. The managers of accounting and outside consultants. b. What factors should be considered in establishing the standards for each cost component? a. Standards should be attainable and exact with no room for any wastage and breakdown. b. Standards should be attainable and should include an allowance for any wastage and breakdown. c. Standards should be exact and above attainable levels so that the staff can be pushed to perform better. 2. CONCEPTUAL CONNECTION Assume that Cabanarama develops the standards for materials use, materials price, labor use, and labor wages. Who will be assigned responsibility for each and for any resulting variances? Why? Once the standards are set, actual results can be compared with the standards and variances can be calculated. Variances are indicators of potential problems. The underlying causes of the variances is reviewed to determine if corrective action is required . The most likely variances include the following: Note: Select the individual that would be assigned to each of the variances listed below and what they would be expected to know. Materials Purchase Price Variance: Responsibility for this variance lies with the Materials purchasing manager . It is this individual who can explain why materials prices differed from the standards. Materials Usage Variance: Responsibility for this variance lies with the Production department manager . It is this individual who knows actual materials used in production and why the amount of materials used differed from the standards. Labor Rate Variance: Responsibility for this variance lies with the Human resources manager . It is this individual who knows why wage rates differ from the standards . Labor Usage Variance: Responsibility for this variance lies with the Plant manager . It is this individual who knows why actual hours differ from the time standards .

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

From Zero To Digital Hero Discovering Opportunities Navigating Challenges And Launching A Successful Online Business For Absolute Beginners

Authors: Nolan Stafford

1st Edition

180342592X, 978-1803425924