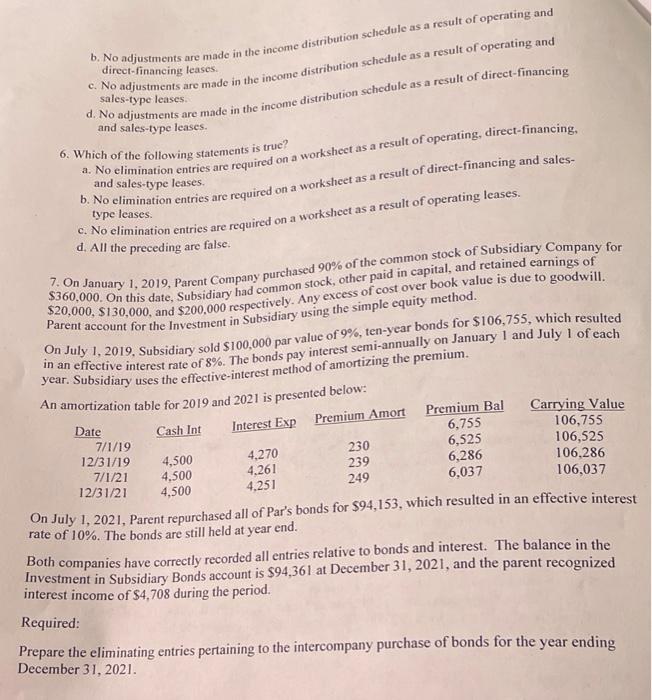

cach Note: All multiple choice questions (1-6) are worth 10 points. Problems 7 and 8 are worth 20 points 1. The motivation of a parent company to purchase the outstanding bonds of a subsidiary could be to w manage all capital needs of the consolidated company for better control of all capital sources b. reduce the parent company's acquisition price for the subsidiary. c. increase the parent company's ownership percentage in the subsidiary. d.create interest revenue to offset interest expense in future income statements 2. A subsidiary has outstanding $100,000 of 8% bonds that were issued at face value. The parent effective interest amortization rather than straight-line amortization of the discount aflect the purchased all the bonds for $96,000 with 5 years remaining to maturity. How will the parent's use of the a. The consolidated financial statements report the same information whether the parent uses straight-line or cflective interest amortization on its investment in sub's bonds. d. Will result in less interest expense in the first year after the intercompany purchase. c. Will result in more interest expense in the first year after the intercompany purchase. 3. In the year when one member of a consolidated group purchases from outside parties the bonds of consolidated financial statements? b. Will result in a different gain on retirement a another affiliate, the purchasing member's income statement includes: a. a gain if purchased above book value. b. a gain if purchased below book value. c. a loss if purchased below book value. d. a deferred gain if purchased above book value. of company Sis a 100%-owned subsidiary of Company P. On January 1, 2019. Company S has $200,000 Dafts% face rate bonds outstanding, which were issued a face value. The bonds had 5 years to maturity on January 1, 2019. Premiums or discounts would be amortized on a straight-line basis. On that date, Company P purchased the bonds for $198,000. The amount on the consolidated balance sheet relative to : a. bonds payable $200,000. b. bonds payable $200,000, discount $2,000. 9. bonds payable $200,000, discount $1,600. d. The bonds do not appear on the consolidated balance sheet. 5. Which of the following statements is true? a. No adjustments are made in the income distribution schedule as a result of operating, direct- financing, and sales-type leases. b. No adjustments are made in the income distribution schedule as a result of operating and direct-financing leases. c. No adjustments are made in the income distribution schedule as a result of operating and sales-type leases d. No adjustments are made in the income distribution schedule as a result of direct-financing and sales-type leases 6. Which of the following statements is true? a. No elimination entries are required on a worksheet as a result of operating, direct-financing. and sales-type leases b. No elimination entries are required on a worksheet as a result of direct-financing and sales- type leases No elimination entries are required on a worksheet as a result of operating leases. d. All the preceding are false. 7. On January 1, 2019, Parent Company purchased 90% of the common stock of Subsidiary Company for $20,000, S130,000, and $200,000 respectively. Any excess of cost over book value is due to goodwill. Parent account for the Investment in Subsidiary using the simple equity method. On July 1, 2019, Subsidiary sold $100,000 par value of 9%, ten-year bonds for $106,755, which resulted Date 7/1/19 106,525 106,286 106,037 year. Subsidiary uses the effective-interest method of amortizing the premium. An amortization table for 2019 and 2021 is presented below: Cash Int Interest Exp Premium Amort Premium Bal Carrying Value 6,755 106,755 12/31/19 230 4,500 4,270 6,525 4,500 4.261 239 6,286 4,500 4.251 249 6,037 On July 1, 2021, Parent repurchased all of Par's bonds for $94,153, which resulted in an effective interest rate of 10%. The bonds are still held at year end. Both companies have correctly recorded all entries relative to bonds and interest. The balance in the Investment in Subsidiary Bonds account is $94,361 at December 31, 2021, and the parent recognized interest income of $4,708 during the period. 7/1/21 12/31/21 Required: Prepare the eliminating entries pertaining to the intercompany purchase of bonds for the year ending December 31, 2021. cach Note: All multiple choice questions (1-6) are worth 10 points. Problems 7 and 8 are worth 20 points 1. The motivation of a parent company to purchase the outstanding bonds of a subsidiary could be to w manage all capital needs of the consolidated company for better control of all capital sources b. reduce the parent company's acquisition price for the subsidiary. c. increase the parent company's ownership percentage in the subsidiary. d.create interest revenue to offset interest expense in future income statements 2. A subsidiary has outstanding $100,000 of 8% bonds that were issued at face value. The parent effective interest amortization rather than straight-line amortization of the discount aflect the purchased all the bonds for $96,000 with 5 years remaining to maturity. How will the parent's use of the a. The consolidated financial statements report the same information whether the parent uses straight-line or cflective interest amortization on its investment in sub's bonds. d. Will result in less interest expense in the first year after the intercompany purchase. c. Will result in more interest expense in the first year after the intercompany purchase. 3. In the year when one member of a consolidated group purchases from outside parties the bonds of consolidated financial statements? b. Will result in a different gain on retirement a another affiliate, the purchasing member's income statement includes: a. a gain if purchased above book value. b. a gain if purchased below book value. c. a loss if purchased below book value. d. a deferred gain if purchased above book value. of company Sis a 100%-owned subsidiary of Company P. On January 1, 2019. Company S has $200,000 Dafts% face rate bonds outstanding, which were issued a face value. The bonds had 5 years to maturity on January 1, 2019. Premiums or discounts would be amortized on a straight-line basis. On that date, Company P purchased the bonds for $198,000. The amount on the consolidated balance sheet relative to : a. bonds payable $200,000. b. bonds payable $200,000, discount $2,000. 9. bonds payable $200,000, discount $1,600. d. The bonds do not appear on the consolidated balance sheet. 5. Which of the following statements is true? a. No adjustments are made in the income distribution schedule as a result of operating, direct- financing, and sales-type leases. b. No adjustments are made in the income distribution schedule as a result of operating and direct-financing leases. c. No adjustments are made in the income distribution schedule as a result of operating and sales-type leases d. No adjustments are made in the income distribution schedule as a result of direct-financing and sales-type leases 6. Which of the following statements is true? a. No elimination entries are required on a worksheet as a result of operating, direct-financing. and sales-type leases b. No elimination entries are required on a worksheet as a result of direct-financing and sales- type leases No elimination entries are required on a worksheet as a result of operating leases. d. All the preceding are false. 7. On January 1, 2019, Parent Company purchased 90% of the common stock of Subsidiary Company for $20,000, S130,000, and $200,000 respectively. Any excess of cost over book value is due to goodwill. Parent account for the Investment in Subsidiary using the simple equity method. On July 1, 2019, Subsidiary sold $100,000 par value of 9%, ten-year bonds for $106,755, which resulted Date 7/1/19 106,525 106,286 106,037 year. Subsidiary uses the effective-interest method of amortizing the premium. An amortization table for 2019 and 2021 is presented below: Cash Int Interest Exp Premium Amort Premium Bal Carrying Value 6,755 106,755 12/31/19 230 4,500 4,270 6,525 4,500 4.261 239 6,286 4,500 4.251 249 6,037 On July 1, 2021, Parent repurchased all of Par's bonds for $94,153, which resulted in an effective interest rate of 10%. The bonds are still held at year end. Both companies have correctly recorded all entries relative to bonds and interest. The balance in the Investment in Subsidiary Bonds account is $94,361 at December 31, 2021, and the parent recognized interest income of $4,708 during the period. 7/1/21 12/31/21 Required: Prepare the eliminating entries pertaining to the intercompany purchase of bonds for the year ending December 31, 2021