Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Calculate COGS and prepare these journal entries Fit for Life (FFL) operates a fitness center and snack lounge. The following is a partial list of

Calculate COGS and prepare these journal entries

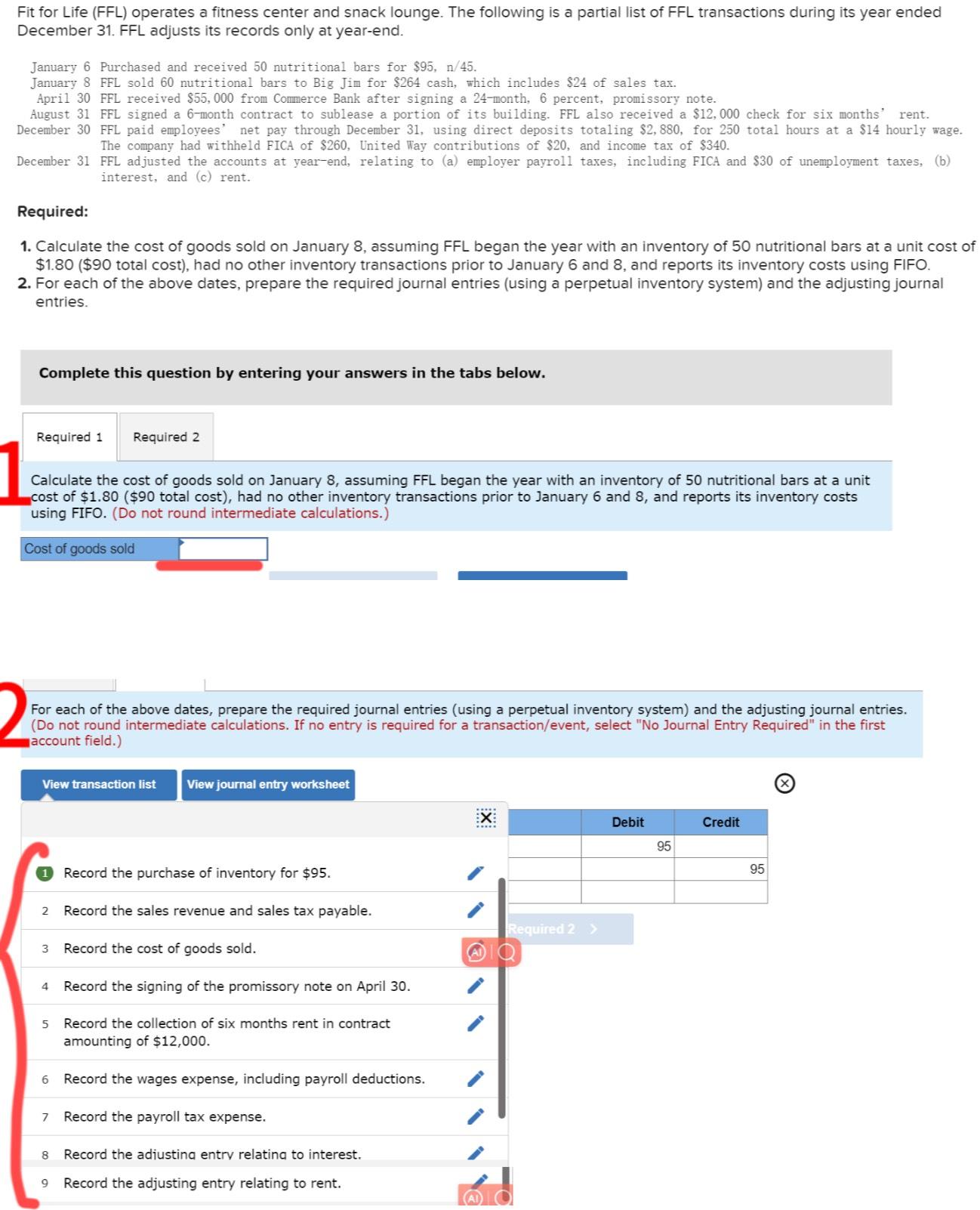

Fit for Life (FFL) operates a fitness center and snack lounge. The following is a partial list of FFL transactions during its year ended December 31. FFL adjusts its records only at year-end. January 6 January S April 30 August 31 December 30 December 31 Required: Purchased and received 50 nutritional bars for $95, n/45. FFL sold 60 nutritional bars to Big Jim for S264 cash, which includes S24 of sales tax. FFL received S55, 000 from Cozmerce Bank after signing a 24month, 6 percent, promissory note. FFL signed a 6month contract to sublease a portion of its building. FFL also received a S12,000 check for six months' rent. FFL paid employees' net pay through December 31, using direct deposits totaling $2, 880, for 250 total hours at a S14 hourly wage. The company had withheld FICA of $260, United Way contributions of $20, and income tax of $340. FFL adjusted the accounts at yeazend, relating to (a) employer payroll taxes, including FICA and S30 of unemployment taxes, (b) interest, and (c) rent. 1. Calculate the cost of goods sold on January 8, assuming FFL began the year with an inventory of 50 nutritional bars at a unit cost of $1.80 ($90 total cost), had no other inventory transactions prior to January 6 and 8, and reports its inventory costs using FIFO. 2. For each of the above dates, prepare the required journal entries (using a perpetual inventory system) and the adjusting journal entries. Complete this question by entering your answers in the tabs below. Required 1 Required 2 Calculate the cost of goods sold on January 8, assuming FFL began the year with an inventory of SO nutritional bars at a unit ost of $1.80 ($90 total cost), had no other inventory transactions prior to January 6 and 8, and reports its inventory costs using FIFO. (Do not round intermediate calculations.) Of For each of the above dates, prepare the required journal entries (using a perpetual inventory system) and the adjusting journal entries. (Do not round intermediate calculations. If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field.) View list View journal entry worksheet Debit 95 2 3 4 5 6 7 8 9 Record the purchase of inventory for $95. Record the sales revenue and sales tax payable. Record the cost of goods sold. Record the signing of the promissory note on April 30. Record the collection of six months rent in contract amounting of $12,000. Record the wages expense, including payroll deductions. Record the payroll tax expense. Record the adiustina entrv relatina to interest. Record the adjusting entry relating to rent. 95

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Just In Time Accounting How To Decrease Costs And Increase Efficiency

Authors: Steven M. Bragg

3rd Edition

0470403721, 978-0470403723