Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Calculate durations and modified durations for the 3% bonds in Table 3.2. You can follow the procedure set out in Table 3.4 for the 9%

Calculate durations and modified durations for the 3% bonds in Table 3.2. You can follow the procedure set out in Table 3.4 for the 9% coupon bonds. Confirm that modified duration closely predicts the impact of a 1% chanec in interest rates on the bond prices.

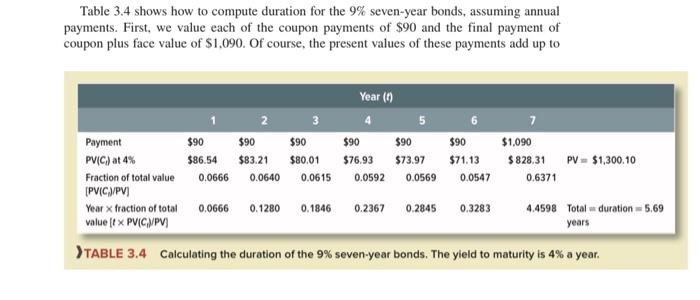

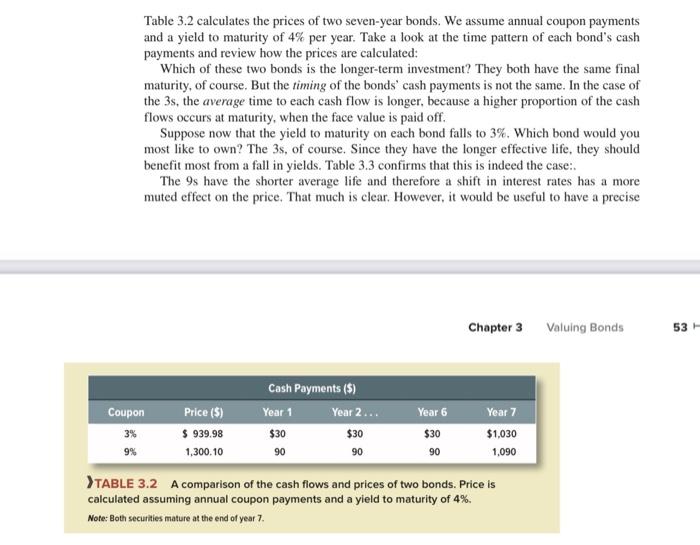

Table 3.2 calculates the prices of two seven-year bonds. We assume annual coupon payments and a yield to maturity of 4% per year. Take a look at the time pattern of each bond's cash payments and review how the prices are calculated: Which of these two bonds is the longer-term investment? They both have the same final maturity, of course. But the timing of the bonds' cash payments is not the same. In the case of the 3s, the average time to each cash flow is longer, because a higher proportion of the cash flows occurs at maturity, when the face value is paid off. Suppose now that the yield to maturity on each bond falls to 3%. Which bond would you most like to own? The 3 s, of course. Since they have the longer effective life, they should benefit most from a fall in yields. Table 3.3 confirms that this is indeed the case: The 9s have the shorter average life and therefore a shift in interest rates has a more muted effect on the price. That much is clear. However, it would be useful to have a precise DTABLE 3.2 A comparison of the cash flows and prices of two bonds. Price is calculated assuming annual coupon payments and a yield to maturity of 4%. Note: Both securties mature at the end of year 7 . Table 3.4 shows how to compute duration for the 9% seven-year bonds, assuming annual payments. First, we value each of the coupon payments of $90 and the final payment of coupon plus face value of $1,090. Of course, the present values of these payments add up to DTABLE 3.4 Caiculating the duration of the 9% seven-year bonds. The yield to maturity is 4% a year please do it in excel to see the formulas

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Front Office Operations And Night Audit Workbook

Authors: Patrick J. Moreo, Gail Sammons, Jim Dougan, James Dougan

1st Edition

0133987698, 978-0133987690