Question

Calculate the average return, standard deviation of Blandy, Gourmange, Portfolio, and Market as well as the correlation of the Blandy & Market and Gourmange &

Calculate the average return, standard deviation of Blandy, Gourmange, Portfolio, and Market as well as the correlation of the Blandy & Market and Gourmange & Market, respectively using the data below:

2. Calculate the beta from the standard deviation of the Blandy and Market, the correlation of Blandy and Market, and then calculate the required return for the Blandy.

3. Calculate the beta from the standard deviation of the Gourmange and Market, the correlation of the Gourmange and Market, and then calculate the required return for the Gourmange.

4. Calculate the beta of the portfolio, and then the required rate of return of the portfolio and the standard deviation of the portfolio.

Data1: rRF=4%, rM=9%,Weight of the Blandy=.75 &Weight of the Gourmange= 0.25%, and beta of the portfolio= 0.7785

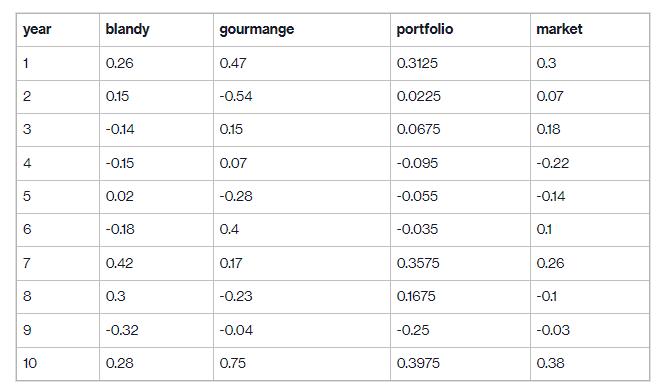

Data2:

year 1 2 3 st 4 01 5 6 7 8 9 10 blandy 0.26 0.15 -0.14 -0.15 0.02 -0.18 0.42 0.3 -0.32 0.28 gourmange 0.47 -0.54 0.15 0.07 -0.28 0.4 0.17 -0.23 -0.04 0.75 portfolio 0.3125 0.0225 0.0675 -0.095 -0.055 -0.035 0.3575 0.1675 -0.25 0.3975 market 0.3 0.07 0.18 -0.22 -0.14 0.1 0.26 -0.1 -0.03 0.38

Step by Step Solution

3.42 Rating (155 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the average return standard deviation and correlation we first need to calculate the returns for each asset using the provided data Then ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Finance A Focused Approach

Authors: Michael C. Ehrhardt, Eugene F. Brigham

6th edition

1305637100, 978-1305637108